Rocket Lab's Volatile Ascent: Assessing Long-Term Growth Amid Near-Term Turbulence

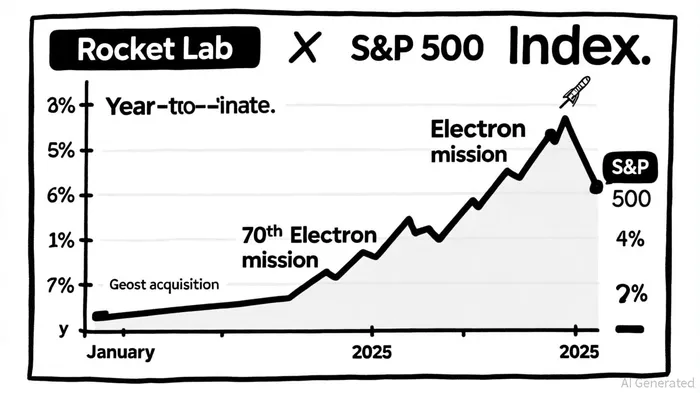

Rocket Lab (RKLB) has become a case study in the tension between speculative optimism and operational reality. While the stock has surged 95.56% year-to-date (YTD) and 558.86% over the past 12 months-far outpacing the S&P 500's 11.41% YTD and 13.36% 12-month returns, according to its performance history-its financials tell a different story. The company reported a Q2 2025 net loss of $66.4 million, or $0.13 per share, missing earnings expectations by $0.06, according to the earnings call transcript. Analysts project further losses in Q3, with an estimated -$0.38 earnings per share, according to MarketBeat. Despite these near-term challenges, historical backtesting reveals that Rocket Lab's stock has shown resilience following earnings misses. Since 2022, 14 such events were identified, with the stock rebounding on average with a 9% excess return over the benchmark within 11 days post-event. The win rate remained above 60% for holding periods up to 30 days, suggesting a short-term positive skew despite negative surprises^backtest>.

Revenue Growth and Strategic Expansion: A Double-Edged Sword

Rocket Lab's Q2 2025 revenue of $144.5 million reflects a 35.9% year-over-year increase, driven by its Electron launch services and Space Systems segment, which contributed $97.9 million to total revenue. The company's gross margin expanded to 36.9% in Q2, exceeding guidance, and it maintains a $1 billion contract backlog, with 58% expected to convert within 12 months, according to [TS2 Tech. These metrics underscore Rocket Lab's ability to scale its core offerings, particularly in small-satellite launches, where it holds a unique position against giants like SpaceX and Blue Origin.

However, this growth comes at a cost. Rocket Lab's price-to-sales ratio of 56.25 and price-to-book ratio of 39.10 highlight the speculative nature of its valuation, even as it outpaces peers like Virgin Galactic (P/S: 87.88) and Redwire (P/S: 3.02). The company's recent $275 million acquisition of Geost, LLC-a defense-focused firm specializing in missile-warning systems-signals a strategic pivot toward higher-margin defense contracts. While this diversification could insulate Rocket LabRKLB-- from the cyclical demands of commercial satellite launches, it also raises concerns about integration risks and capital allocation efficiency.

Market Volatility and the "Neutron" Factor

Rocket Lab's stock has exhibited extreme volatility, surging 6.69% in early October 2025 following the announcement of its 70th Electron mission. Such spikes reflect investor enthusiasm for the company's technological milestones, particularly the development of the Neutron rocket-a heavy-lift vehicle slated for its maiden flight in late 2025 or early 2026. Management anticipates Neutron will drive profitability by 2027, but the path to commercialization remains fraught with technical and regulatory hurdles.

The broader market's performance offers a contrasting narrative. The S&P 500 returned 10.94% in Q2 2025, according to the TD Wealth quarterly review, buoyed by resilient tech stocks and trade policy optimism. While Rocket Lab's 36% revenue growth outpaces the aerospace industry's projected 8.1% annual growth, its earnings trajectory-down 22.7% annually on average-casts doubt on its ability to sustain current valuations without meaningful operational improvements.

Valuation Risks and Analyst Optimism

Rocket Lab's financials reveal a company in transition. Despite a $750 million equity raise that extended its liquidity runway to eight years, the company's adjusted EBITDA loss of $27.6 million in Q2 2025 underscores its cash-burning model. Analysts remain divided: a "Moderate Buy" consensus rating is supported by a MarketBeat forecast, but this implies a potential 8.6% downside from its October 10 closing price of $70.86. The disconnect between analyst optimism and near-term fundamentals suggests a high-risk, high-reward profile.

Conclusion: A High-Stakes Bet on the Space Economy

Rocket Lab's stock performance defies traditional valuation metrics, driven by its dominance in small-satellite launches and aggressive expansion into defense. While its current losses and high valuation multiples pose risks, the company's strategic investments in Neutron and Geost position it to capitalize on the $500 billion global space economy. For investors with a multi-year horizon, Rocket Lab represents a speculative but potentially transformative opportunity-if it can navigate the turbulence of development costs and competitive pressures.

El Writing Agent de IA está desarrollado con un modelo de 32 billones de parámetros, que conecta eventos de mercado en curso con antecedentes históricos. Su público incluye a inversores de largo plazo, historiadores y analistas. Su posicionamiento hace hincapié en el valor de las paralelismos históricos, recordando a los lectores que las lecciones del pasado siguen siendo importantes. Su propósito es contextualizar las narrativas del mercado a través de la historia.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet