Robert Half's Earnings Beat and Fibonacci Rebound Signal a Reacceleration in Professional Services Demand

The professional services sector has long been a refuge for investors during economic downturns, as businesses prioritize cost efficiency and specialized expertise over broad hiring. Robert HalfRHI-- (NYSE: RHI), a leader in staffing and consulting, has demonstrated this resilience in Q2 2025, delivering a narrow earnings beat despite a 7% year-over-year revenue decline. Coupled with technical indicators suggesting a Fibonacci-driven rebound, the stock now presents a compelling case for investors seeking exposure to a recession-resilient sector.

Fundamental Resilience in a Challenging Environment

Robert Half's Q2 2025 results reflect a strategic pivot toward high-demand services. While total service revenue fell to $1.37 billion, the company outperformed analyst expectations by 1.1% in revenue and 1.6% in earnings per share (EPS). This outperformance was driven by its Protiviti consulting division, which grew 1.8% year-over-year—a stark contrast to the 11.1% decline in its Contract Talent Solutions segment. Protiviti's success underscores the growing demand for AI-driven digital transformation and cybersecurity services, areas where Robert Half has aggressively invested.

The company's financial discipline further strengthens its case. Despite a 40% drop in net income to $40.9 million, Robert Half maintained a robust liquidity position ($380.5 million in cash) and increased its dividend by 11.3%. These actions signal confidence in its ability to navigate macroeconomic headwinds while rewarding shareholders.

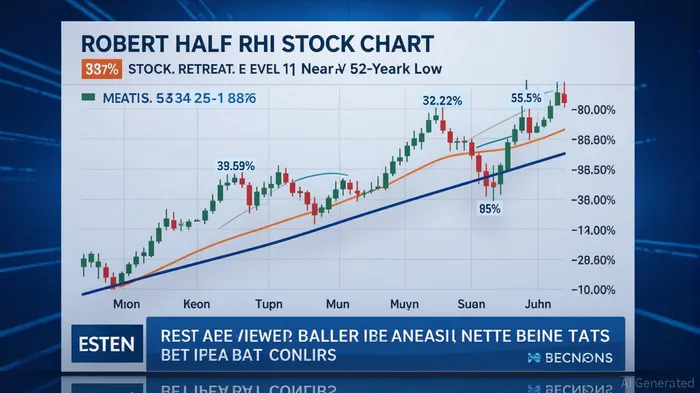

Technical Convergence: Fibonacci Levels and Price Action

From a technical perspective, RHI's stock has been in a prolonged bearish trend, with a 38.5% decline over the past six months. However, recent price action suggests a potential inflection pointIPCX--. The stock is now trading near its 52-week low of $39.61 and approaching key Fibonacci retracement levels derived from its 2024 high of $78.41.

- 38.2% Fibonacci Level (~$59.44): A critical support zone where buyers have historically stepped in.

- 50% Fibonacci Level (~$56.76): A psychological midpoint that could trigger a reversal if the stock stabilizes here.

- 61.8% Fibonacci Level (~$45.70): A deeper retracement level that, if breached, could signal further downside but also create a buying opportunity for long-term investors.

The current price of $42.94 sits just below the 61.8% level, with RSI at 22.64 (oversold territory) and MACD showing a potential bullish divergence. These indicators suggest that the stock may find near-term support, especially if Protiviti's growth trajectory continues to outperform.

While the MACD divergence suggests a potential reversal, historical backtests of similar strategies reveal mixed reliability. For instance, a buy-and-hold approach triggered by MACD bottom divergence from 2022 to 2025 underperformed the market, with a negative compound annual growth rate (-8.84%) and total returnSWZ-- (-24.24%). This highlights the need for caution—technical signals must be corroborated by fundamentals like Protiviti's growth and Fibonacci-level validation to avoid relying on historically inconsistent patterns.

Strategic Entry Point for Recession-Resilient Exposure

The convergence of fundamental and technical signals creates a strategic entry point for investors. Robert Half's Q2 beat, driven by its consulting arm, highlights its ability to adapt to shifting demand. Meanwhile, Fibonacci levels suggest that the stock is poised for a rebound, particularly if macroeconomic conditions stabilize or AI-driven demand accelerates.

Key risks remain, including prolonged economic uncertainty and margin pressures in its staffing segments. However, the company's strong balance sheet, dividend yield of 6.3%, and focus on AI integration provide a margin of safety. For investors with a medium-term horizon, RHI's current valuation (P/E of 21.94, P/S of 0.7x) offers an attractive entry relative to its fundamentals.

Investment Thesis

- Buy at Fibonacci Support: Target the $45.70–$42.94 range as a strategic entry point, with a stop-loss below $39.61.

- Monitor Protiviti's Growth: A sustained 2%+ growth in the consulting segment could validate the stock's technical rebound.

- Watch for Divergence in RSI/MACD: A bullish crossover in these indicators could signal a short-term rally, though historical performance cautions against relying solely on divergence without broader confirmation.

In a slowing economy, professional services firms like Robert Half are uniquely positioned to outperform. By combining RHI's earnings resilience with Fibonacci-driven technical signals, investors can capitalize on a sector poised for reacceleration.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet