The Rising Threat to Traditional Banking: How the GENIUS Act is Reshaping the Stablecoin Landscape

The U.S. GENIUS Act of 2025 has ignited a seismic shift in the stablecoin and digital asset landscape, redefining the competitive dynamics between decentralized finance (DeFi) and centralized finance (CeFi). By establishing a federal regulatory framework that mandates 1:1 reserve backing for stablecoins and excludes them from securities classification, the Act has created a stark divergence in risk profiles and institutional investment strategies between these two ecosystems [1]. For investors, this legislative pivot demands a recalibration of risk assessment and positioning in a market where regulatory clarity is both a catalyst and a constraint.

DeFi’s Regulatory Resilience and Institutional Embrace

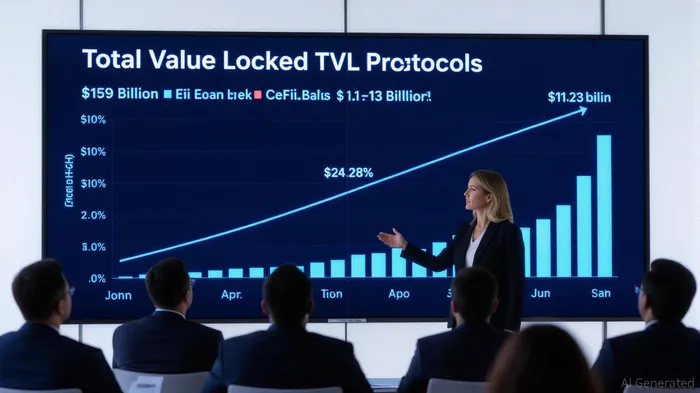

The GENIUS Act’s exclusion of DeFi protocols from securities oversight has been a boon for decentralized platforms, reducing compliance burdens and attracting institutional capital. Total Value Locked (TVL) across major DeFi protocols has surged to $159 billion, a stark contrast to CeFi’s shrinking loan books, which have plummeted to $11–13 billion from a 2022 peak of $34.8 billion [2]. This shift reflects DeFi’s operational resilience: smart contracts enforce transparency, and protocols like AaveAAVE-- and Lido offer yields that outpace traditional banking products. For instance, USDC—a permitted stablecoin under the Act—now dominates 24.28% of the market, with $2.6 billion locked in lending protocols [3].

The Act’s requirement for stablecoin issuers to maintain reserves of U.S. Treasuries and FDIC-insured deposits has further bolstered institutional confidence in DeFi. Platforms leveraging compliant stablecoins, such as Ethereum-based Exchange-Traded Products (ETPs), have seen $5.4 billion in inflows since July 2025 [4]. This trend is amplified by the Act’s bankruptcy protections for stablecoin holders, which mitigate insolvency risks and align with institutional risk appetites [5].

CeFi’s Struggle with Compliance and Trust

Conversely, CeFi platforms face a dual challenge: regulatory scrutiny and eroding trust. The GENIUS Act’s licensing requirements and reserve mandates have imposed compliance costs that disproportionately affect mid-sized and community banks, many of which lack the infrastructure to tokenize assets or integrate blockchain systems [6]. High-profile security breaches, such as Bybit’s $1.46 billion theft, have further tarnished CeFi’s reputation, driving investors toward DeFi’s trustless models [2].

While the Act aims to curb systemic risks by restricting stablecoin issuance to licensed entities, it has inadvertently stifled innovation in CeFi. JPMorgan’s pivot to tokenized deposit products and crypto-backed loans underscores the sector’s struggle to adapt [7]. For institutional investors, CeFi’s shrinking market share and regulatory uncertainty present a high-risk, low-reward proposition.

Strategic Risk Assessment: DeFi vs. CeFi

The GENIUS Act has reshaped risk paradigms. DeFi’s embedded compliance—via smart contracts and transparent audits—reduces counterparty risk, though it remains vulnerable to smart contract exploits (92 incidents in H1 2025, totaling $470 million in losses) [3]. CeFi, meanwhile, faces existential threats from regulatory arbitrage and operational fragility. The Act’s emphasis on AML/CFT compliance also raises costs for CeFi, which must now navigate overlapping federal and state mandates [8].

For investors, the key lies in balancing these risks. DeFi’s institutional-grade protocols—such as ChainlinkLINK-- and Ethereum—offer yield opportunities but require rigorous due diligence on security and governance. CeFi’s niche, however, remains in cross-border payments and custodial services, where its infrastructure advantages persist [9].

Investment Positioning in the New Era

The post-GENIUS Act landscape favors DeFi-first strategies. Institutional capital is flowing into protocols with compliance-first designs, such as Gnosis’ Safe multi-signature wallets and zero-knowledge proof (ZKP) privacy solutions [4]. These innovations align with the Act’s emphasis on transparency while addressing privacy concerns.

Conversely, CeFi’s survival hinges on partnerships with regulated stablecoin issuers and the adoption of tokenized assets. Banks that modernize their infrastructure—like JPMorgan’s tokenized deposit experiments—may carve out a role in hybrid models [7]. However, the broader trend points to DeFi’s ascendancy, driven by Gen Z’s crypto adoption and the de-banking pressures reshaping traditional finance [2].

Conclusion

The GENIUS Act has not merely regulated stablecoins—it has redefined the battlefield between DeFi and CeFi. For traditional banking, the threat is twofold: regulatory displacement and institutional capital flight. Investors must now navigate a landscape where DeFi’s compliance-driven innovation and CeFi’s compliance-heavy constraints dictate risk-adjusted returns. As the Act’s global influence grows—spurring EU MiCA alignment and CBDC development—the winners will be those who adapt to a decentralized, transparent future [10].

Source:

[1] The GENIUS Act of 2025 Stablecoin Legislation Adopted in ... [https://www.lw.com/en/insights/the-genius-act-of-2025-stablecoin-legislation-adopted-in-the-us]

[2] Institutions Bet Big on DeFi as CeFi Collapses Under $34.8B Loss [https://www.ainvest.com/news/bitcoin-news-today-institutions-bet-big-defi-cefi-collapses-34-8b-loss-2508/]

[3] The DOJ's 2025 Liability Clarification and the Rise of Institutional-Grade DeFi Infrastructure [https://www.ainvest.com/news/doj-2025-liability-clarification-rise-institutional-grade-defi-infrastructure-2508/]

[4] GENIUS Act: Catalyst or Catastrophe? Haven1's Take on the New Stablecoin Rulebook [https://haven1.org/blog/genius-act-catalyst-or-catastrophe-haven1s-take-on-the-new-stablecoin-rulebook]

[5] The Rise of USDCUSDC-- in the Post-GENIUS Act Era: Strategic Positioning in the Stablecoin Gold Rush [https://www.ainvest.com/news/rise-usdc-post-genius-act-era-strategic-positioning-investors-stablecoin-gold-rush-2508/]

[6] The GENIUS Act and Stablecoins: What Banks Need to Know [https://www.crnrstone.com/gonzobanker/the-genius-act-and-stablecoins-what-banks-need-to-know]

[7] Corporate Crypto After the GENIUS Act [https://www.rand.org/pubs/commentary/2025/08/corporate-crypto-after-the-genius-act.html]

[8] GENIUS Act: New Rules for Stablecoin Issuers [https://www.cbh.com/insights/articles/genius-act-new-rules-for-stablecoin-issuers/]

[9] Institutional Flows & Yield Strategies Drive Crypto Maturation [https://www.galaxy.com/insights/perspectives/institutional-flows-and-yield-strategies-drive-crypto-market-maturation]

[10] Stablecoin Regulation 2025: Global Liquidity & Trading Strategies [https://phemex.com/blogs/stablecoin-regulation-2025-global-liquidity-trading-strategies]

Decoding blockchain innovations and market trends with clarity and precision.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet