Rising Retirement Costs and Social Security Uncertainties: Why Your State Choice Could Make or Break Your Nest Egg

The cost of retirement in the U.S. isn't one-size-fits-all—it's a postcode lottery. From Hawaii's sky-high expenses to West Virginia's budget-friendly charm, retirees face stark geographic disparities that demand urgent attention. Compounding this is the looming threat of Social Security cuts, projected to reduce benefits by 21% by 2033. In this volatile landscape, a one-dimensional retirement strategy is a recipe for disaster. Let's dissect the data and explore how investors can navigate these risks with precision.

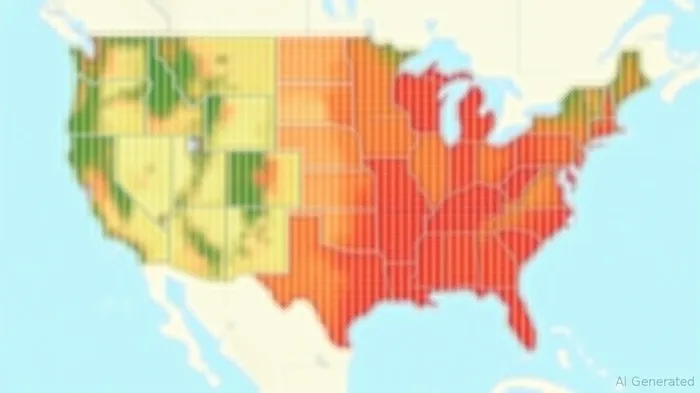

The State-by-State Retirement Cost Divide: Where You Live Could Double Your Expenses

According to the latest 2025 data, Hawaii's annual retirement cost tops $129,296—nearly double the $58,190 needed in West Virginia. This gap isn't just about housing (Hawaii's rents are 230% of the national average) or taxes (New York's high-tax burden inflates costs), but also healthcare. While Hawaii boasts top-tier healthcare, Mississippi's seniors face the worst care quality, despite its affordability.

The mathMATH-- is clear: retirees in high-cost states like California ($100,687/year) or Massachusetts ($100,201/year) must save $3 million or more to avoid running out of money. Meanwhile, those in affordable states like Kansas ($60,620/year) can get by with closer to $700,000. But even this assumes no inflation shocks—a dangerous assumption given the Federal Reserve's median 55-60-year-old has just $185,000 saved.

Social Security's Clock is Ticking: Plan for Reduced Lifelines

The Social Security Administration warns that trust funds may only cover 81% of benefits starting in 2033. Relying on this safety net is a gamble, especially for retirees in high-cost states where monthly benefits average just $22,437 annually—far below Hawaii's $107,657 pre-Social Security retirement cost.

Investors must treat Social Security as a supplement, not a foundation. Diversifying income streams—such as rental properties, dividend-paying stocks, or annuities—is critical. For example, states like Alaska (no income tax) and Wyoming (low property taxes) offer tax-friendly environments to grow such assets.

Investment Strategies to Combat Cost Disparities

- Geographic Cost Analysis: Choose Your Battlefield

- Low-Cost States (West Virginia, Oklahoma): Prioritize location-specific real estate investments. REITs like PSA (Senior Housing Properties Trust) or OHI (Omega Healthcare Investors) can generate rental income in states where housing is affordable but in demand.

High-Cost States (Hawaii, California): Focus on inflation-protected assets. Treasury Inflation-Protected Securities (TIPS) or commodities like gold (GLD) can hedge against rising living expenses.

Healthcare as an Investment Theme

States with poor healthcare quality (e.g., Mississippi) may see rising demand for private medical services. Companies like CVS Health (CVS) or telemedicine platforms like Teladoc (TDOC) could thrive as retirees seek alternatives to underfunded public systems.

Tax Efficiency Across Borders

Use states like Florida (no income tax) or Texas (no state income tax) to domicile IRAs or trusts. Tax-efficient ETFs like VTAX (a tax-free municipal bond fund) can also minimize drag on retirement savings.

Diversify Beyond the Obvious

- Alternative Income Streams: Consider peer-to-peer lending platforms (e.g., Upstart (UPST)) or fractional real estate investments (e.g., Fundrise) to generate passive income in low-cost states.

- Annuities: Use deferred income annuities to lock in payouts aligned with your state's cost of living. For example, a $100,000 annuity in Mississippi could provide more post-tax income than the same amount in New York.

The Bottom Line: Location and Liquidity Are Your Shields

The data is unequivocal: retirees in high-cost states face a savings gap exceeding $1.5 million compared to their peers in low-cost regions. With Social Security's future in doubt, investors must adopt a geographically aware, income-diversified portfolio.

- Act Now: Use low-cost states as cash generators while high-cost areas demand inflation hedges.

- Avoid Overreliance on Real Estate: While owning a home reduces housing costs, consider renting in volatile markets (e.g., coastal California) to preserve liquidity.

- Monitor Federal Policy: Social Security reform could come sooner than 2033. Stay plugged into legislative updates via platforms like Morningstar's Policy Hub.

In the end, retirement isn't about chasing the cheapest state—it's about aligning your portfolio's income streams with the cost realities of where you choose to live. The clock is ticking; start mapping your strategy today.

Dave Michaels' Investment Takeaway:

“Retirement planning in 2025 isn't a solo bet on a single state—it's a multi-asset, location-aware strategy. Pair low-cost state residency with tax-smart investments, and you'll turn uncertainty into opportunity.”

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet