Rising Economic Pessimism and Its Impact on Market Volatility

The Volatility Paradox: Calm on the Surface, Turbulence Beneath

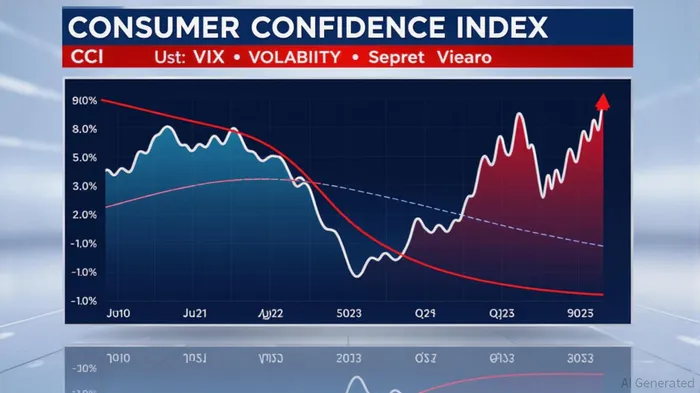

Market volatility, as measured by the VIX index, offers a counterintuitive narrative. After spiking above 50 in April 2025 amid tariff uncertainties, the VIX settled at 16 by the end of Q3 2025, signaling historically low volatility, according to a Lake Tahoe Wealth Management commentary. This apparent contradiction-economic pessimism coexisting with market calm-stems from policy interventions. A 90-day tariff pause and trade agreements with Japan and the European Union alleviated fears of a global trade standstill, as noted in the Lake Tahoe commentary. Yet, this stability is fragile. The Federal Reserve's cautious approach to rate cuts and the projected GDP slowdown to 1.9% in 2025, as noted in the Lake Tahoe commentary, suggest that underlying uncertainties remain.

Defensive Investing: A Strategic Retreat

In such an environment, defensive investing emerges as a prudent strategy. Defensive sectors-utilities, healthcare, and consumer staples-typically outperform during periods of economic uncertainty. However, Q3 2025 data reveals a mixed picture. Utilities delivered a robust 7.57% return, buoyed by a well-behaved bond market and lower discount rates, according to a UBT investment overview. In contrast, consumer staples and healthcare lagged, with the former posting a -2.36% total return due to higher input costs and weak demand, as noted in the UBT investment overview. This divergence highlights the importance of sector-specific analysis.

For instance, Enbridge's record Q3 adjusted EBITDA, driven by U.S. gas utilities, contrasts sharply with CNH Industrial's 5% revenue decline, underscoring the uneven impact of macroeconomic headwinds, as noted in the UBT investment overview. Defensive investors must prioritize companies with strong balance sheets and predictable cash flows, even within traditionally safe sectors.

Policy Uncertainties and the Road Ahead

The Federal Reserve's policy calculus adds another layer of complexity. While rate cuts are anticipated to support a weakening labor market, the central bank's reliance on alternative data sources-such as the Chicago Fed's real-time labor market indicators-signals a lack of confidence in traditional metrics, according to an AOL report. This uncertainty could reignite volatility if economic data diverges from expectations.

International markets, meanwhile, offer a glimmer of hope. European equities outperformed U.S. counterparts, driven by stronger earnings and geopolitical stability, as noted in the Lake Tahoe commentary. China's tech sector recovery further diversified global growth drivers. Defensive investors might consider allocating to international markets, particularly in sectors insulated from U.S. inflationary pressures.

Conclusion: Balancing Caution and Opportunity

Rising economic pessimism and low volatility present a paradox for investors. While the VIX suggests market complacency, the CCI and sector performance reveal a landscape of uneven risks. Defensive investing, when executed with granularity-favoring utilities over consumer staples and hedging against policy shocks-can mitigate downside risks. Yet, complacency is a dangerous trap. As the Fed's policy adjustments and global trade dynamics evolve, vigilance remains paramount.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet