Rising Dining-Out Costs and Retirement Readiness: Navigating Discretionary Spending in an Inflationary Era

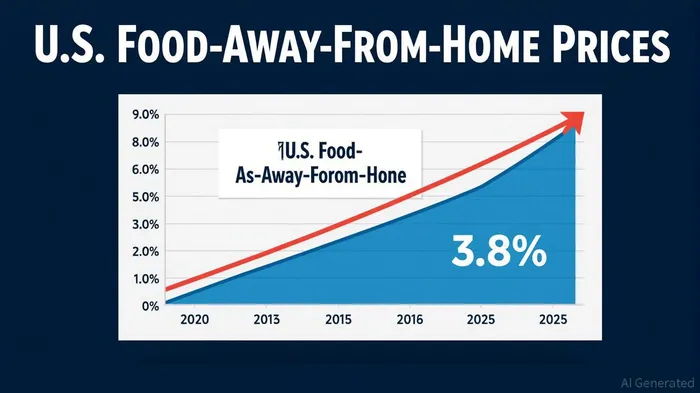

The rising cost of dining out has become a critical factor in retirement planning. According to the U.S. Bureau of Labor Statistics (BLS), food-away-from-home prices surged 3.8% in June 2025 compared to June 2024, with a projected annual increase of 4.0% for 2025. This trend, driven by inflationary pressures, labor cost hikes, and shifting consumer behavior, is reshaping how retirees manage discretionary spending. For retirees, the cumulative impact of dining-out expenses—averaging $2,250 annually—can erode retirement savings over decades, potentially costing millions by age 80.

The Discretionary Spending Dilemma

Discretionary spending on food services is not just a lifestyle choice but a financial lever with long-term consequences. The BLS data reveals that food-away-from-home spending grew 8.6% in the April–June 2022 quarter compared to the same period in 2021, outpacing broader inflation. This surge reflects post-pandemic consumer behavior, where dining out became a symbol of recovery and social reconnection. However, as prices rise, retirees face a trade-off: maintain dining habits at the expense of savings or adjust budgets to prioritize financial security.

The restaurant industry's bifurcation into fast-casual and fine-dining segments, as highlighted by the 2025 James Beard Foundation report, underscores this challenge. Fast-casual chains like Chipotle and Panera Bread have thrived by offering value-driven meals, while mid-tier and fine-dining establishments struggle to justify premium pricing in a cost-conscious environment. This shift has implications for retirees seeking to balance affordability with quality of life.

Asset Classes in the Crosshairs

The ripple effects of rising dining-out costs extend beyond consumer behavior, influencing equity performance and investment strategies. Fast-casual and fast-food chains, with their scalable models and price resilience, have outperformed mid-tier and fine-dining operators. For example, McDonald'sMCD-- and other global fast-food brands have leveraged limited-edition products and global exclusives to maintain customer engagement despite inflation. Conversely, mid-tier restaurants, which raised menu prices by an average of 27.2% to offset operational costs, face declining traffic as diners opt for cheaper alternatives.

Investors seeking to capitalize on this trend may focus on ETFs tracking the restaurant sector, such as the Restaurant Meals ETF (EAT), which allocates heavily to fast-casual and fast-food companies. Conversely, those aiming to mitigate dining-out costs might consider alternative assets like Treasury Inflation-Protected Securities (TIPS) or real estate investment trusts (REITs), which hedge against inflation and preserve purchasing power.

Retirement Strategies for a Volatile Era

To align retirement portfolios with the realities of rising dining-out costs, retirees should adopt strategies that balance growth, liquidity, and income generation:

- Bucketing and Dynamic Withdrawal Plans

- Short-term bucket: Allocate 1–3 years of essential expenses to cash or short-term bonds to avoid selling equities during downturns.

- Mid-term bucket: Use high-quality bonds and dividend-paying stocks to generate income while preserving capital.

Long-term bucket: Invest in equities or ETFs with exposure to inflation-resistant sectors (e.g., consumer staples, utilities).

Tax-Advantaged Accounts

Maximize contributions to Health Savings Accounts (HSAs) and 401(k)s to reduce taxable income and grow savings tax-free. HSAs, in particular, offer a dual benefit by covering healthcare costs—a growing concern for retirees.

Annuities for Income Stability

Fixed annuities provide guaranteed income streams, reducing the need to liquidate assets for discretionary expenses. For retirees prioritizing dining-out flexibility, variable annuities linked to equity indices offer growth potential with downside protection.

Leveraging Technology and Rewards

- Credit cards with dining-out rewards (e.g., 6% cash back) and restaurant loyalty programs can offset costs. Pairing these with budgeting apps like Mint or YNAB (You Need A Budget) ensures disciplined spending.

The Road Ahead

As dining-out costs remain elevated, retirees must recalibrate their financial strategies. The restaurant industry's evolution toward value-driven models and technological innovation will likely continue, favoring operators that prioritize affordability and efficiency. For investors, this means reallocating capital to resilient sectors while retirees should adopt proactive spending and investment habits to preserve savings.

In an era where $100-a-day dining out expenses can accumulate to $2 million over 40 years, the stakes for retirement readiness have never been higher. By aligning asset allocations with macroeconomic trends and leveraging tools to manage discretionary spending, retirees can safeguard their financial independence while still enjoying the occasional meal out.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet