Rising Debt, Defensive Sectors, and the Path to Portfolio Resilience

The U.S. national debt is careening toward a critical inflection point. According to Ray Dalio's recent projections, the fiscal trajectory outlined for 2025—where annual government spending hits $7 trillion, revenues lag at $5 trillion, and debt service costs soar to $18 trillion—paints a stark picture. This escalating debt burden, combined with the Federal Reserve's constrained ability to raise interest rates, creates fertile ground for inflationary pressures and market instability. In this environment, investors must reassess risk exposure and prioritize defensive strategies aligned with historical debt cycles and systemic vulnerabilities.

The Debt Dynamics and Their Implications

Dalio's analysis underscores a stark reality: the U.S. is on course to see its debt-to-GDP ratio rise to 130% by 2030, with national debt per household surpassing $425,000. The fiscal options to address this—drastic spending cuts, tax hikes, or currency devaluation—are all politically unpalatable. The historical preference for monetary easing (lowering rates, expanding the money supply) suggests a likely path of currency devaluation to erode the real value of debt.

This approach carries dual consequences:

1. Inflation: Erosion of purchasing power as money supply outpaces economic growth.

2. Interest Rate Suppression: Near-zero rates for an extended period, compressing returns for fixed-income investors.

The knock-on effects to equities are clear. Cyclical sectors tied to economic sensitivity—such as financials or real estate—face headwinds, while industries with pricing power and stable demand are poised to outperform.

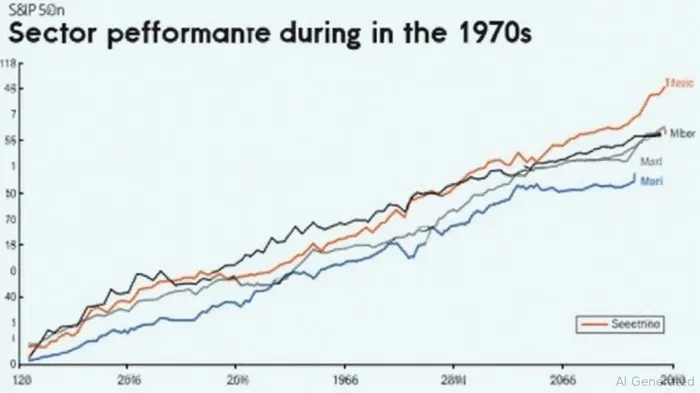

Historical Precedent: The 1970s Stagflation

The 1970s stagflation offers a cautionary mirror. During that period, the U.S. faced 13% inflation, stagnant growth, and negative real returns for equities. Yet defensive sectors thrived:

- Utilities benefited from regulated monopolies and inelastic demand for essentials like electricity.

- Healthcare saw steady demand for medical services, with costs absorbed by insurance or public programs.

- Consumer Staples maintained sales of food and household products despite inflation.

These sectors weathered the storm by relying on pricing power and essential demand. For example, Coca-Cola's stock price rose 200% in nominal terms during the decade, even as the broader market declined in real terms.

Defensive Sectors: The Modern Case for Resilience

Today's fiscal environment mirrors the . Let's examine why utilities, healthcare, and consumer staples remain critical defensive pillars:

Utilities: Steady as She Goes

- Regulated monopolies: Provide stable revenue streams with predictable cash flows.

- Inelastic demand: Energy and water are non-negotiable for households and businesses.

- Pricing power: Regulated rate adjustments allow utilities to pass through inflation.

Utilities have historically low beta (below 0.5) compared to the broader market, making them a hedge against volatility.

Healthcare: Necessity Amid Crisis

- Medical demand: Unaffected by economic cycles—people prioritize healthcare even in recessions.

- Cost pass-through: Insurers and governments absorb much of the inflation pressure.

- Innovation: Biotech and pharmaceuticals offer long-term growth despite macro headwinds.

Healthcare's defensive characteristics are further bolstered by aging populations and rising chronic disease rates.

Consumer Staples: The Bedrock of Demand

- Essentials-driven: Food, beverages, and hygiene products remain top priorities for consumers.

- Brand loyalty: Companies like Procter & Gamble or Nestlé maintain pricing power via trusted brands.

- Global supply chains: Scale and efficiency reduce vulnerability to input cost shocks.

These sectors have shown a strong positive correlation with rising inflation, outperforming cyclicals when prices spike.

Strategic Asset Allocation: A Dalio-Backed Playbook

Dalio's warnings demand proactive adjustments to portfolio construction:

Prioritize Low-Beta Stocks:

Focus on sectors with minimal sensitivity to economic swings. Utilities, healthcare, and consumer staples are prime candidates.Inflation-Hedging Assets:

- Gold: A 15% allocation can mitigate currency devaluation risks (as Dalio advises).

Inflation-Linked Bonds (TIPS): Directly tied to CPI, offering protection against rising prices.

Reduce Exposure to Rate-Sensitive Sectors:

Financials, real estate, and tech (dependent on cheap capital) face risks from prolonged low rates and margin compression.Monitor Debt-to-GDP Metrics:

Rising debt levels historically correlate with declining bond yields, reinforcing the case for shifting capital to real assets.

Conclusion: Navigating the Debt Storm

The path ahead is fraught with fiscal challenges, but history offers a roadmap for investors. By tilting portfolios toward defensive sectors with pricing power and stable demand—utilities, healthcare, and consumer staples—investors can mitigate the risks of currency devaluation and inflation. Pairing these allocations with gold and inflation-linked bonds creates a balanced shield against systemic debt-driven volatility.

Dalio's warnings are not merely theoretical; they reflect a cycle that has repeated throughout history. Those who heed them now will be better positioned to preserve capital and capitalize on opportunities in an increasingly uncertain economic landscape.

Stay informed and stay resilient.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet