The Retirement Savings Anxiety of Millennials and Gen Xers: Navigating Uncertainty with Passive Income Strategies

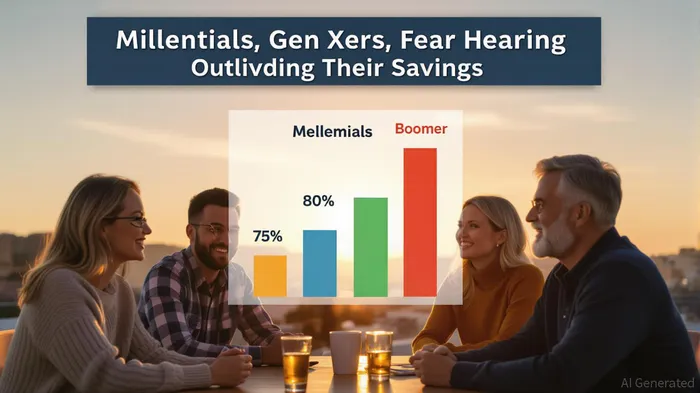

In 2025, the specter of retirement savings anxiety looms large over millennials and Gen Xers. Surveys reveal that 57% of millennials and 56% of Gen Xers believe they are at risk of outliving their savings, a stark contrast to the 40% of boomers who share this concern. This generational divide underscores a critical shift in financial priorities, as younger and middle-aged Americans grapple with inflation, market volatility, and the uncertain future of Social Security. For these cohorts, retirement is no longer a distant horizon but an urgent planning imperative.

The Financial Tightrope: Savings, Confidence, and Risk

The Northwestern Mutual Planning & Progress Study paints a sobering picture. Gen Xers, in particular, face a crisis of confidence: 54% of them believe they will not be financially prepared for retirement, despite saving an average of 17% of their income. Their median household savings of $150,000 pale in comparison to the $1.26 million "magic number" deemed necessary for a comfortable retirement in 2025. Meanwhile, millennials, though starting to save earlier (at age 29 on average), exhibit a troubling imbalance. Sixty percent admit they overemphasize investment growth while neglecting risk management tools like life or disability insurance. This "offense-only" approach leaves their portfolios vulnerable to unforeseen shocks.

The role of Social Security further complicates the landscape. Gen Xers rank it as their top retirement concern, with 54% including it in their top three worries. Yet only 26% plan to delay benefits until their full retirement age, a decision that could significantly boost their monthly payouts. For millennials, the uncertainty is compounded by their reliance on a system they fear may not exist in its current form by the time they retire.

Passive Income: A Lifeline for Long-Term Security

Amid these challenges, passive income strategies are emerging as a critical tool for both generations. Dividend stocks, real estate investment trusts (REITs), and alternative assets like fractional ownership in tangible assets (e.g., fine art, collectibles) offer a way to generate consistent cash flow without active labor. For millennials, platforms like Konvi and ESG-focused ETFs are democratizing access to these opportunities. Gen Xers, meanwhile, are gravitating toward dividend-paying stocks and REITs861104--, which align with their preference for stability and long-term capital preservation.

Consider the case of PrologisPLD-- (PLD), a real estate investment trust that has consistently increased its dividend payouts. Over the past five years, its yield has averaged 2.5%, providing investors with a reliable income stream. For Gen Xers seeking predictable returns, such assets can supplement traditional savings and offset the erosion of purchasing power caused by inflation. Similarly, millennials investing in high-growth dividend stocks like MicrosoftMSFT-- (MSFT) or AppleAAPL-- (AAPL) can benefit from compounding returns while diversifying their portfolios.

However, passive income is not a panacea. Both generations must balance growth-oriented strategies with risk mitigation. For instance, while 63% of millennials invest in sustainable or ethical vehicles, many overlook the importance of insurance products that protect against disability or longevity risk. A 45-year-old Gen Xer with a $500,000 portfolio might allocate 30% to dividend stocks, 20% to REITs, and 10% to annuities to ensure a steady income stream, while reserving 40% for growth-oriented equities.

Redefining Retirement: Work, Wealth, and Wisdom

The traditional notion of retirement is fading. Forty-five percent of millennials and 48% of Gen Xers plan to work during retirement, either for financial necessity or personal fulfillment. This shift opens new avenues for passive income. For example, a Gen Xer with a background in tech could monetize online courses on platforms like Teachable, generating royalties while staying engaged. Similarly, millennials leveraging peer-to-peer lending platforms can earn interest income from loans, albeit with higher risk.

Yet, the data also reveal a blind spot: 61% of both generations overestimate the safety of index funds, assuming they offer downside protection or access to the "best" investments. In reality, index funds mirror the market's upsUPS-- and downs, including its worst performers. This misconception could leave retirees exposed during downturns, particularly as Gen Xers approach retirement age with less time to recover.

A Path Forward: Balancing Growth and Protection

For millennials and Gen Xers, securing retirement requires a dual focus on growth and protection. Here's how to build a resilient strategy:

1. Diversify Income Streams: Combine dividend stocks, REITs, and alternative assets to reduce reliance on a single source of income.

2. Prioritize Risk Management: Allocate 10–15% of your portfolio to insurance products like long-term care or disability coverage.

3. Leverage Digital Tools: Use robo-advisors or ESG-focused platforms to streamline passive income generation while aligning with personal values.

4. Reassess Social Security Timing: Delaying benefits until age 70 can increase monthly payouts by up to 24%, a critical boost for those with lower savings.

Ultimately, retirement savings anxiety is not a dead end but a call to action. By embracing passive income strategies and addressing gaps in risk management, millennials and Gen Xers can transform uncertainty into opportunity. The key lies in balancing ambition with prudence—a lesson that will define their financial futures in an era of unprecedented economic complexity.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet