The Resurgence of Bond Market Volatility and Its Implications for Fixed-Income Portfolios

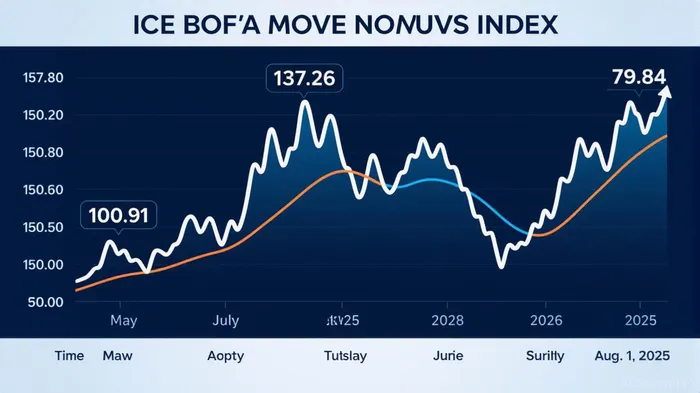

The bond market, long a haven for risk-averse investors, has become a stormy sea in 2025. The ICE BofA MOVE Index—a critical barometer of fixed-income volatility—has surged to its highest level in over 13 years, signaling a profound shift in risk perception. This volatility is not merely a technical anomaly but a reflection of deepening macroeconomic uncertainty, policy ambiguity, and asset reallocation trends. For fixed-income investors, the implications are clear: traditional strategies must adapt to a landscape where complacency is fleeting and diversification is no longer a given.

The Drivers of Volatility: Inflation, Policy, and Economic Uncertainty

The MOVE Index's recent surge is rooted in three pillars: inflation expectations, central bank policy ambiguity, and trade-war-induced economic uncertainty.

Inflation's Persistent Shadow: The one-year CPI swap rate has climbed above 3%, driven by stubborn labor-driven service inflation. Retiring baby boomers and restrictive immigration policies have created a labor shortage, keeping wage growth—and thus inflation—elevated. While the PCE price index has moderated to 2.6% year-over-year, this remains above the Federal Reserve's 2% target. Investors are pricing in higher inflation for years to come, as reflected in the MOVE Index's elevated readings.

Central Bank Policy in Perilous Waters: The Federal Reserve's dual mandate—price stability and maximum employment—has collided with a paradox: a tight labor market coexisting with inflation stubbornly above 2.5%. The Fed's caution about rate cuts, despite market expectations for one or two reductions in the second half of 2025, has fueled uncertainty. The term premium on long-term bonds has spiked, with the 10-year Treasury yield climbing as investors demand higher compensation for holding duration in a policy vacuum.

Trade Wars and Supply Chain Chaos: The administration's on-again, off-again approach to tariffs has created a fog of uncertainty. A federal court's recent blockage of key tariffs has only deepened the confusion, with businesses delaying capital spending and global supply chains destabilized. The U.S. Business Leaders Survey Future Capital Spending index now sits at its lowest level since the pandemic, a stark indicator of corporate pessimism.

Reallocation Opportunities in a Volatile World

As bond markets grapple with these headwinds, investors are recalibrating their portfolios. The MOVE Index's spikes are not just a warning but a call to action—particularly for those overexposed to long-duration bonds.

Short-Duration and Inflation-Linked Bonds: With the term premium elevated, long-term bonds have become riskier. Short-duration bonds and Treasury Inflation-Protected Securities (TIPS) offer a safer harbor. The iShares TIPS BondTIP-- ETF (TIP) has outperformed conventional Treasuries in 2025, reflecting this shift. Investors should consider tilting toward these instruments to mitigate inflation and duration risk.

Alternatives as a Diversifier: Traditional diversification is failing. The U.S. dollar's 7% decline since the trade war began has eroded its safe-haven status. Alternatives like gold, infrastructure, and private credit are gaining traction. Gold's 10-year correlation with equities has fallen to 0.15, its lowest since the 2008 crisis, making it a compelling hedge. Meanwhile, infrastructure and power-related real estate—especially in data centers and renewable energy—are attracting capital due to their inflation-resistant cash flows.

Equity Sector Rotation: Defensive equities, particularly utilities and consumer staples, have shown resilience. However, valuations in these sectors are stretched. A better opportunity lies in healthcare providers, which trade at a discount to their long-term averages. For growth investors, the AI theme remains durable, with falling compute costs and surging enterprise spending creating a runway for innovation-driven sectors.

Emerging Markets and the AI Energy Bottleneck: While trade policy uncertainty has weighed on emerging markets, Latin America is emerging as a beneficiary of supply chain reallocation. Investors should remain selective but open to long-term opportunities in regions with structural growth drivers. Meanwhile, the AI-driven energy bottleneck—a 5x–7x surge in power demand—is creating structural opportunities in traditional and renewable energy, nuclear, and battery storage.

Conclusion: A Portfolio for the New Normal

The ICE BofA MOVE Index's resurgence is more than a technical indicator—it's a signal that the bond market is pricing in a world of persistent uncertainty. For fixed-income investors, the playbook must evolve: short-duration and inflation-linked bonds, alternatives, and a more nuanced approach to equity sector rotation are now table stakes. The key is to balance resilience with growth, leveraging volatility rather than fearing it. In this new normal, adaptability is the ultimate asset.

As the market navigates the crosscurrents of inflation, policy, and global trade, one thing is certain: complacency is the most dangerous risk of all.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet