Renewable Energy Infrastructure: A Goldmine for Long-Term Capital Appreciation

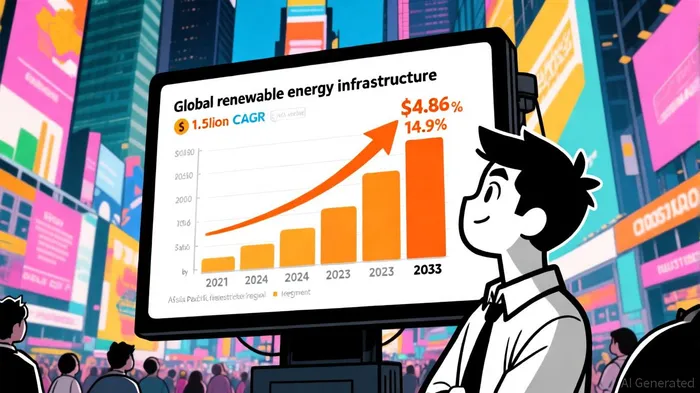

The renewable energy infrastructure sector is no longer a speculative bet-it's a seismic shift in global capital allocation. With the market projected to balloon from $1.51 trillion in 2024 to $4.86 trillion by 2033 at a 14.9% CAGR, investors are staring at a once-in-a-generation opportunity, according to a Grand View Research report. This isn't just about solar panels or wind turbines; it's about reimagining energy systems, industrial processes, and even geopolitical power dynamics. Let's break down why this sector is a must-own for long-term capital appreciation-and how policy-driven momentum is turbocharging the growth.

Market Dynamics: Solar, Industrial, and Asia Pacific Lead the Charge

Solar energy is the poster child of this revolution. Its 27.09% share of the 2024 market reflects a perfect storm of falling costs (down 89% since 2010 per BloombergNEF) and technological leaps in efficiency. Meanwhile, the industrial segment-accounting for 61.63% of revenue in 2024-has become a critical battleground for decarbonization. Factories are now installing on-site solar arrays, biomass systems, and hybrid solutions to slash energy costs and meet ESG targets, as highlighted in a Saur Energy analysis.

Asia Pacific is the engine of this growth, commanding 41.24% of the global market in 2024. Countries like India and China are deploying gigawatts of solar and wind at breakneck speed, driven by both economic necessity and climate ambition. For investors, this means exposure to high-growth markets with underpenetrated infrastructure needs.

Policy-Driven Momentum: From Tax Credits to Global Agreements

The Inflation Reduction Act (IRA) has been a game-changer for U.S. renewables. By offering $421 billion in tax credits (ITCs and PTCs) from 2025 to 2030, it has made clean energy projects financially viable even without subsidies. But the U.S. isn't alone. At COP28, 130 nations committed to tripling global renewable capacity to 11,000 GW by 2030, according to an IEA report. To hit that target, countries are deploying a toolkit of competitive auctions (India, EU), biofuel mandates (Brazil, India), and green hydrogen incentives (Brazil's $3.2B program, noted by Saur Energy).

The EU's Renewable Energy Directive, which mandates 32% renewables in energy consumption by 2030, has already spurred grid modernization and storage investments. Similarly, China's Building Energy Efficiency Plan is pushing solar PV and geothermal adoption in construction-a sector ripe for disruption.

Case Studies: Policies That Deliver

Germany's Energiewende policy, with its feed-in tariffs and long-term subsidies, has turned the country into a wind and solar powerhouse. California's Renewable Portfolio Standard (RPS), requiring 60% clean energy by 2030, has driven utility-scale solar and battery projects. These examples prove that robust policy frameworks can transform abstract climate goals into concrete infrastructure growth.

However, not all policies hit their mark. Ghana's struggles with mini-grid development highlight the risks of fragmented incentives and poor execution, as the IEA documents. This underscores the need for investors to focus on jurisdictions with clear regulatory roadmaps and stakeholder alignment.

Challenges and the Path Forward

Despite the optimism, hurdles remain. Global renewable investment in 2022 hit $500 billion, but that's still a fraction of the $1.2–1.5 trillion/year needed to meet climate targets. Policy shifts-like the U.S. administration's recent freeze on IRA tax credit guidance-add uncertainty. Yet, the long-term trajectory is undeniable. The IEA projects 940 GW of annual renewable additions by 2030, and the NDC Partnership is actively helping countries bridge deployment gaps.

For investors, the key is to balance short-term volatility with long-term inevitability. Prioritize companies with diversified geographies (e.g., solar developers in Asia, hydrogen firms in Europe) and strong policy tailwinds. Avoid overexposure to regions with regulatory instability.

Conclusion: A Sector Built to Last

Renewable energy infrastructure isn't a passing trend-it's the bedrock of a $5.62 trillion market by 2033. With solar, industrial decarbonization, and Asia Pacific leading the charge, and policy frameworks from the IRA to COP28 providing relentless momentum, this sector offers a rare combination of scale, durability, and societal impact. For those willing to ride the wave, the rewards could be as transformative as the energy transition itself.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet