Refiners Are Running Hot: Why CRAK Leads While XOP & PXE Lag

Major U.S. refiners have been one of 2025’s stealth winners. As Sherwood noted, names like ValeroVLO--, Marathon PetroleumMPC--, and Phillips 66PSX-- are beating most of the S&P 500 this year—reflecting a powerful (if choppy) rebound in refining margins. Sherwood News

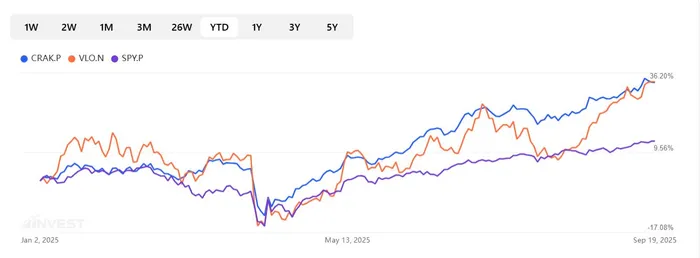

Scoreboard: CRAKCRAK-- vs. XOPXOP-- & PXE (YTD)

CRAK (VanEck Oil Refiners ETF): +33.5% YTD. Pure-play exposure to global refiners. Expense ratio 0.62%.

XOP (SPDR S&P Oil & Gas E&P): +1.65% YTD. Equal-weighted upstream E&Ps; expense ratio 0.35%.

PXE (Invesco Dynamic Energy E&P): +1.25% YTD. Quant-selected U.S. E&Ps; expense ratio 0.63%.

Bottom line: refiners (CRAK) have sharply outperformed upstream producers (XOP, PXE) in 2025.

Why Refiners Are Winning

1) Margins got a summer boost. Global refining margins climbed into early summer on tighter product supply—helped by plant outages and delays at big new facilities—pushing gasoline/diesel cracks higher and lifting refiner earnings expectations.

2) Diesel strength mattered. Elevated diesel margins—especially in Europe and during mid-summer—provided a tailwind to complex refineries geared to middle distillates.

3) Crude volatility helped. When crude prices soften or chop while product prices hold up, the “crack spread” widens—good for refiners. Recent U.S. data showed a large crude draw and gasoline decline even as distillates built, underscoring the noisy backdrop refineries are navigating.

ETF Angles You Can Act On

CRAK — Refiners, straight up. CRAK tracks the MVIS Global Oil Refiners Index, holding a concentrated slate of refiners like Marathon Petroleum, Phillips 66, Valero, and global peers. If you’re expressing a view on product margins rather than crude price, this is the cleanest vehicle.

XOP — Equal-weight U.S. E&Ps. XOP is highly sensitive to WTI beta and exploration/production cash flows. It can lag in periods when crude underperforms refined products—or when investor attention shifts from growth barrels to margin capture.

PXE — Factor-tilted E&Ps. PXE tracks Invesco’s Dynamic Energy Exploration & Production Intellidex, which tilts toward companies with stronger fundamentals. It’s still an upstream bet, so the same caveats as XOP apply if product cracks, not oil prices, are doing the heavy lifting.

Risks & What Could Flip the Trade

Refining is notoriously cyclical. New capacity ramp-ups (e.g., mega-refineries in Mexico and Nigeria) and seasonal demand fade can compress margins quickly. Analysts already flagged the summer margin bump as short-lived, with risks that rising runs and softer macro demand narrow cracks into year-end. If cracks roll over while crude steadies or rises, E&Ps (XOP, PXE) can retake leadership.

What to Watch (Practical Signals)

3-2-1 crack spread trends (gasoline + diesel vs. WTI): a quick pulse on refiner economics. (Supports CRAK when widening.)

EIA weekly data: gasoline/distillate inventories and refinery utilization (currently ~93% in the latest print). Tight product stocks + high utilization = supportive for refiner cash flows.

Headlines on outages/new capacity: unplanned downtime and delayed start-ups help margins; smooth ramps pressure them.

Takeaway

The refiner trade has been the winning energy expression in 2025—CRAK captures it cleanly—while broad E&P baskets (XOP, PXE) have been largely flat. If you believe margins can stay elevated (or at least above mid-cycle) into Q4, the overweight remains justified. If you think cracks compress and crude steadies, rotating some exposure back to XOP/PXE makes sense. For now, the tape—and the margins—favor CRAK.

Quickly compare CRAK, XOP, PXE side by side with our ETF Compare Tool

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet