Real Estate Strategy in 2025: Timing the Market or Building Equity with Larger Down Payments?

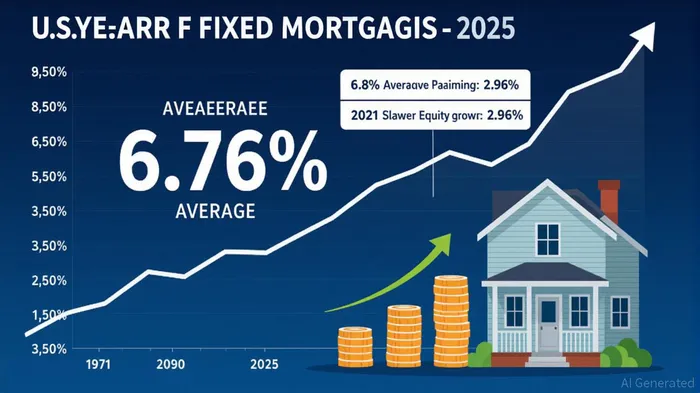

The U.S. real estate market in 2025 is a study in contradictions. Mortgage rates, while modestly declining from pandemic-era lows, remain stubbornly high—averaging 6.8% as of July 2025. This environment has created a paradox: homeowners are locked into their properties due to favorable existing rates, while potential buyers face a market where inventory is scarce and affordability is a growing concern. For investors and first-time buyers, the question looms: Should you wait for rate drops to time the market, or prioritize building equity through larger down payments in a high-rate environment?

The Case for Larger Down Payments: Equity as a Buffer

Historical data from Freddie Mac reveals that the 30-year fixed mortgage rate has averaged 7.71% since 1971. While 2025's 6.8% is below this long-term average, it remains a significant hurdle for affordability. A larger down payment mitigates this risk by reducing the loan-to-value (LTV) ratio, which in turn lowers monthly payments and eliminates the need for private mortgage insurance (PMI). For example, a $369,000 home with a 20% down payment and a 6.77% rate results in a $1,918 monthly payment, compared to $1,927 for a 6.86% rate in 2024. Over 30 years, this saves $4,633 in interest.

Moreover, equity growth is a critical long-term consideration. Homeowners with 20% down payments start with 20% equity, creating a buffer against market volatility. In a stagnant or slowly appreciating market (projected to rise 3% in 2025), this initial equity can offset potential price declines. For first-time buyers, programs like Florida's HFA Advantage PLUS—which forgives 5% of the purchase price over five years—can amplify this effect, turning a strategic down payment into a compounding asset.

The Risks of Timing the Market: Uncertainty and Opportunity Costs

Timing the market for rate drops is tempting, but it's fraught with uncertainty. The Federal Reserve's cautious approach to rate cuts—projecting only one or two reductions in 2025—means rates will likely remain in the 6.5–7% range through the year. Even if rates drop to 5% by 2026, buyers who delay entry risk missing out on equity gains. For instance, a $369,000 home purchased in 2025 with a 20% down payment would see its value rise to $385,050 by 2026 (assuming 3% annual growth). A delayed buyer would pay $26,050 more for the same property, eroding the savings from a lower rate.

Additionally, low inventory exacerbates the risk of delayed entry. With existing home sales at 20–30% below historical averages, buyers who wait may find themselves competing for fewer homes, driving prices upward. This is particularly true in Sun Belt markets like Florida, where first-time buyer activity remains strong despite a 6.9% median price drop in 2024.

Balancing Strategy: A Framework for Decision-Making

For investors and first-time buyers, the optimal strategy hinges on three factors: financial readiness, risk tolerance, and market timing.

Financial Readiness: A larger down payment requires liquidity, but it also reduces long-term debt. For those with access to equity or savings, allocating funds to a down payment is a safer bet than investing in volatile assets like stocks or cryptocurrencies. High-yield savings accounts or short-term CDs can preserve capital while rates remain uncertain.

Risk Tolerance: Timing the market demands patience and the ability to withstand short-term volatility. If you're comfortable holding cash for 12–18 months while waiting for rate drops, this could be viable. However, the Federal Reserve's inflation targets suggest rates may stay elevated through 2026, making this a high-stakes gamble.

Market Timing: In regions with rising inventory (e.g., Florida's 45% increase in listings in 2024), buyers have more leverage to negotiate prices. Conversely, in tight markets like the Northeast, delaying entry could mean missing out on competitive offers.

Actionable Advice for 2025

- For First-Time Buyers: Leverage down payment assistance programs. Florida's HFA Advantage PLUS and Orlando's $45,000 forgivable loan are prime examples of how to reduce upfront costs while securing equity.

- For Investors: Prioritize markets with rising inventory and modest price growth. Sun Belt regions offer better liquidity and lower risk of overpaying.

- For All Buyers: Avoid using volatile investments for down payments. Instead, allocate funds to high-yield savings or short-term CDs to preserve capital.

Conclusion: Equity Over Timing in a High-Rate Environment

The 2025 real estate market is defined by high rates, low inventory, and cautious Fed policy. While timing the market for rate drops may seem appealing, the risks of delayed entry—missed equity gains, rising prices, and limited inventory—outweigh the potential rewards. A larger down payment, combined with strategic use of assistance programs, offers a more reliable path to long-term wealth accumulation. In this environment, patience and liquidity are your greatest assets.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet