Real Estate Services Stocks Sell-Off: Who Is the Next AI Victim?

On Wednesday, February 11, the "AI Scare Trade" officially broadened its blast radius, decimating the commercial real estate services sector. Shares of industry giants CBRE Group Inc.CBRE--, Jones Lang LaSalle Inc.JLL-- (JLL), and Cushman & Wakefield Ltd. collapsed, registering losses between 12% and 14%. This marks the steepest single-day decline for these firms since the onset of the Covid-19 pandemic in 2020. However, unlike the pandemic-driven selloff, which was based on a temporary freeze in physical occupancy, yesterday’s crash represents a structural re-rating of the business model itself. Investors are no longer asking if Artificial Intelligence will displace human intermediaries; they are asking how fast.

The market consensus is shifting violently. For decades, these firms have relied on a "high-headcount" model—armies of brokers, researchers, and leasing agents charging significant fees to facilitate transactions. The arrival of autonomous AI agents threatens to democratize this data and automate the deal-making process, effectively compressing margins to near zero. While some analysts from Jefferies argue that the selloff is an "excessive knee-jerk reaction" given the companies' data moats, the price action suggests the market is pricing in a permanent disruption. The era of the high-fee middleman is ending. For investors, the signal is clear: avoid labor-intensive service stocks and rotate capital into the physical infrastructure required to power the AI revolution.

The Catalyst: Claude’s "Cowork" and the SaaS Implosion

To understand why real estate stocks collapsed yesterday, one must look at the digital carnage that preceded it earlier this week. The market is reeling from the release of Anthropic’s new "Claude cowork" feature. This development allows multiple autonomous AI agents to collaborate in a shared workspace, executing complex, multi-step workflows without human intervention.

Previously, AI was a tool for a human to use (a "copilot"). The "cowork" update changes the paradigm to "autopilot." This has triggered a massive selloff in the Software-as-a-Service (SaaS) sector. The logic is brutal: if an AI agent can execute the work of three junior analysts, companies will no longer need to purchase expensive, per-seat software licenses for human employees. The revenue models of major B2B software firms are essentially tied to human headcount. As headcount shrinks, so does the Total Addressable Market (TAM) for seat-based software.

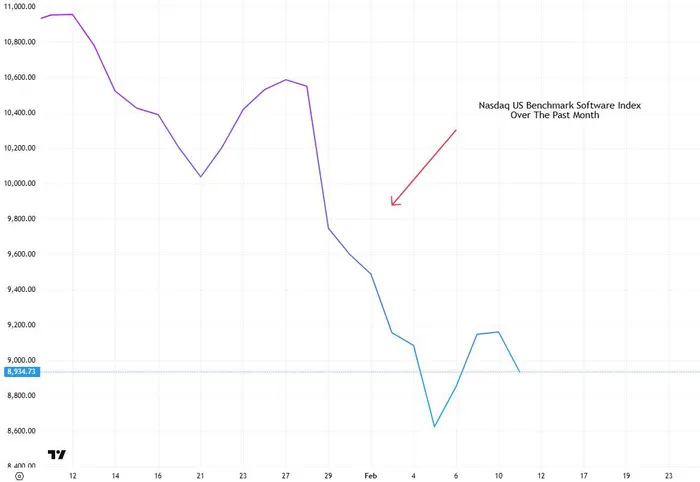

According to Ainvest Analysis, this fear has materialized in the charts. The Nasdaq US Benchmark Software Index (Figure 1) has been in freefall over the past month, breaking critical support levels as the capabilities of these new agents became public.

The contagion spread rapidly to the real estate services sector this Wednesday. Just as Claude is replacing the junior legal associate, investors realized that AI agents could easily replace the junior real estate broker. Much of the work in commercial real estate—market research, lease abstraction, comparative market analysis—is data processing.

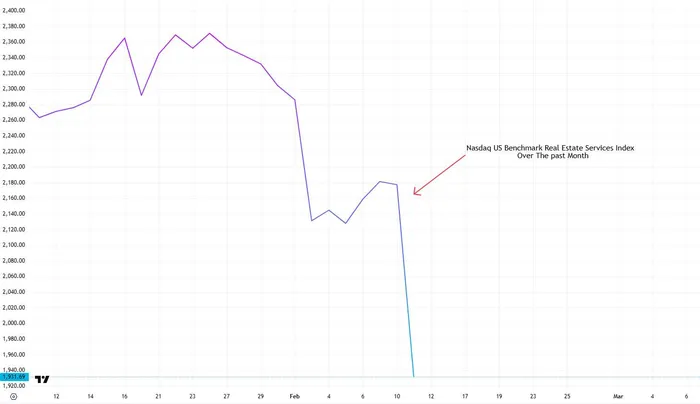

According to Ainvest Analysis, the Nasdaq US Benchmark Real Estate Services Index (Figure 2) mirrors the software crash, dropping vertically as the market digested the implications of the "cowork" feature.

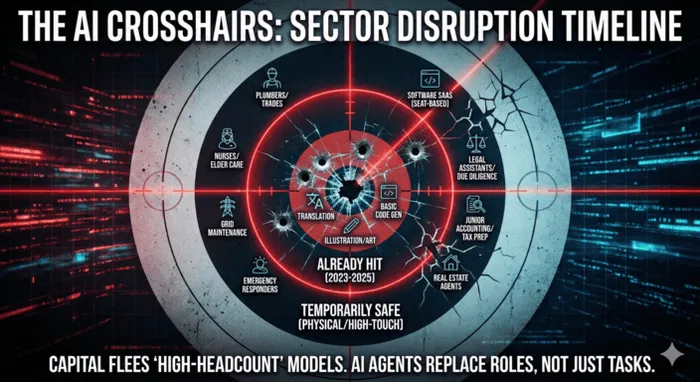

Adding fuel to the fire was the recent announcement by Altruist regarding their new AI tax planning integration. The tool demonstrated the ability to structure complex tax strategies for high-net-worth individuals in seconds—a service that usually costs thousands of dollars in billable hours from accounting firms. This specifically battered stocks in the tax preparation and financial compliance sectors, reinforcing the narrative: if your business model relies on billing for hours spent on intellectual processing, you are in the crosshairs.

Forecasting the Damage: Wealth Management, BPO, and Creative Sectors

If real estate and legal services are the current victims, who is next? The "AI Scare Trade" will likely hunt down any industry where value is derived from information asymmetry or manual digital labor.

Wealth Management is a prime target. The industry currently charges roughly 1% of assets under management (AUM) for portfolio construction and rebalancing. As AI agents become capable of executing sophisticated, tax-loss harvesting strategies and personalized asset allocation at a fraction of the cost, the justification for human advisory fees evaporates. We anticipate significant pressure on traditional asset managers who have not integrated AI-native workflows.

Business Process Outsourcing (BPO) and Customer Support are perhaps the most vulnerable. The "Claude cowork" model excels at customer handling and back-office resolution. The labor arbitrage model—hiring cheap human labor in developing nations—is obsolete when AI inference costs are falling exponentially.

Furthermore, the Creative and Advertising sectors are facing an existential threat from tools like "Seedance." While earlier image generators disrupted illustrators, Seedance has demonstrated the ability to generate high-fidelity, motion-consistent video content and full ad campaigns from text prompts. This threatens the billing model of ad agencies, which historically charge for the heavy lifting of production, filming, and editing. If a marketing director can generate a commercial using Seedance, the need for a junior creative team vanishes. The market will soon turn its gaze to ad-holding companies, re-evaluating their future cash flows in a world where content creation cost trends toward zero.

The Strategic Pivot: Long Energy, Copper, and Compute

Despite the gloom in the services sector, this is not a signal to exit the market entirely. Instead, it is a call for a strategic rotation. The development of AI is deflationary for services but inflationary for physical resources.

Investors should look toward AI Infrastructure. The more capable AI agents become, the more compute power they consume. This creates an inelastic demand for three key commodities:

- Electricity (Utilities & Uranium): AI data centers are power-hungry. The US power grid is already strained, and the demand from hyperscalers is projected to triple by 2030. Utilities companies, particularly those with nuclear assets or rapid renewable deployment capabilities, are the new defensive growth stocks.

- Copper: There is no AI without electricity, and there is no electricity transmission without copper. Upgrading the grid and building data centers requires massive amounts of copper, yet global supply is constrained.

- Semiconductor Manufacturing (Foundries): While software margins compress, the hardware manufacturers (the "pick and shovel" plays) retain pricing power. The physical construction of chip fabrication plants remains a bottleneck that AI code cannot solve overnight.

Conclusion

The 12% crash in CBRECBRE-- and JLLJLL-- is not an anomaly; it is the beginning of a market-wide "Efficiency Rotation." Wall Street is systematically repricing companies with high human capital costs and moving that liquidity into companies with high physical capital assets.

The "AI Scare Trade" is rational. The release of autonomous agentic workflows like Claude’s "cowork" and specialized tools like Altruist and Seedance proves that white-collar automation is accelerating. For the astute investor, the play is simple: Short the "middleman" who charges for time; Long the utility that powers the machine. The AI revolution will not just replace roles; it will reshape the very foundation of value in the US equity market.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet