Can Quanta Turn Data Center Demand Trends Into Margin Upside?

Quanta Services, Inc. PWR highlighted that data centers now account for nearly 10% of the business as of 2025, making it its fastest-growing backlog segment. But the bigger question for investors is whether this demand surge can translate into meaningful margin expansion.

The company is seeing strong infrastructural demand as the U.S. energy landscape undergoes a fundamental transformation. Expectations for rising power needs, driven by data centers, Artificial Intelligence and broader technology adoption, continue to expand the scope of work across all forms of energy generation. Quanta is increasingly moving toward long-term, programmatic contracts rather than one-off project bidding. These multi-year arrangements with hyperscalers and utilities provide revenue visibility and risk-adjusted returns, a formula that prioritizes earnings quality over short-term margin spikes.

Furthermore, PWR’s $500-$700 million vertical supply-chain investment, particularly in high-voltage transformers, could reduce procurement bottlenecks and improve execution certainty. This derisking strategy may not immediately boost reported margins but could enhance return on invested capital and protect profitability as data center loads scale.

Labor tightness, especially in data center markets, remains a constraint. Yet Quanta’s decades-long investment in craft labor and prefabrication capabilities gives it a competitive edge. Management also emphasized that architectural shifts, including higher-voltage DC systems, are unlikely to shrink its total addressable market. Thus, while explosive margin expansion may not be imminent, Quanta appears well-positioned to convert sustained data center demand into durable, compounded earnings growth.

Quanta vs. Market Peers

Quanta is positioning itself as a full-spectrum infrastructure partner in the data center boom, competing with EMCOR Group, Inc. EME and AECOM ACM across engineering, construction and power solutions.

EMCOR remains strong in mechanical and electrical contracting within data center campuses, particularly on complex MEP installations, while AECOM focuses more on design, program management and advisory roles globally.

Market factors such as AI-driven load growth, labor tightness and supply-chain constraints favor firms with craft depth and procurement control. In that context, Quanta’s scale, backlog visibility and grid-centric positioning may provide a structural advantage as data center power demand accelerates, compared with EMCOR and AECOM.

PWR Stock’s Price Performance & Valuation Trend

Shares of this specialty contracting services provider have trended upward 51.9% in the past six months, outperforming the Zacks Engineering - R and D Services industry, the broader Construction sector and the S&P 500 index.

Image Source: Zacks Investment Research

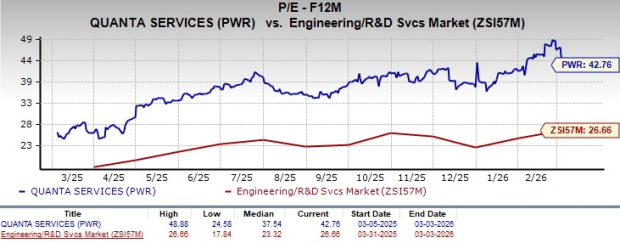

PWR stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 42.76, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of PWR

PWR’s earnings estimates for 2026 and 2027 have trended upward in the past 30 days, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 19.7% and 16.7%, respectively.

Image Source: Zacks Investment Research

Quanta stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

AECOM (ACM): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet