Q1 Market Recap: Tariff Tensions Trigger Volatility, Tech Stocks Tumble, Europe Shines Bright

The first quarter of 2025 was defined largely by rising economic uncertainty and heightened volatility, driven significantly by escalating tariff tensions. GoldmanGXUS-- Sach's US Economic Policy Uncertainty Index surged to its highest levels since early 2020, reflecting investors growing anxiety over trade policy. Economists predict a substantial rise in the US effective tariff rate—from last year's modest 3% up by potentially 10 percentage points, with risks extending even higher. This shift has considerably disrupted investor confidence, leading to a spike in annualized volatility on the S&P 500 above 20%, a level unseen since the turbulent summer of last year.

Equity indices broadly declined through Q1, reflecting tariff-induced concerns. The Nasdaq Composite experienced its worst quarterly drop since 2022, falling 10.42%, severely pressured by growth and technology stocks. Meanwhile, the S&P 500 and Dow Jones Industrial Average dropped by 4.59% and 1.28%, respectively, indicating a broader but comparatively moderate pullback. Small-cap stocks were notably weaker, with the Russell 2000 declining 10.62%, underscoring increased investor risk aversion toward economically sensitive sectors. Concurrently, market volatility, as indicated by the S&P 500 VIX, climbed 12.84%, emphasizing the nervous sentiment among traders.

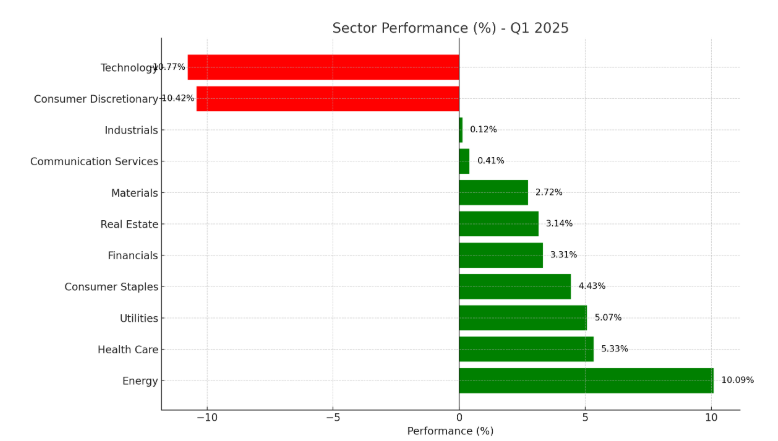

Sector performance within the S&P 500 exhibited a marked divergence, highlighting investors rotation into defensive positions. Energy notably outperformed, rising 10.09% amid higher oil prices and persistent geopolitical tensions. Defensive sectors including Health Care (+5.33%), Consumer Staples (+4.43%), and Utilities (+5.07%) also saw significant inflows, reflecting a clear preference for stability and reliability amid uncertainty. Financials managed modest gains of 3.31%, benefiting from stable interest rate dynamics, whereas Real Estate and Materials saw marginally positive returns. Conversely, Information Technology plunged by 10.77%, heavily affected by tariff fears and valuation concerns, while Consumer Discretionary faced even harsher conditions, down 10.77%, as consumer confidence and discretionary spending expectations declined sharply.

Within equities, Q1's strongest-performing high-volume stocks indicated selective bullishness. MicroalgoMLGO-- Inc (MLGO) astonishingly surged 515.96%, driven by speculative momentum despite recent volatility. H&E Equipment ServicesHEES-- (HEES) gained 94.89%, benefiting from robust industrial demand, while Corcept TherapeuticsCORT-- (CORT) jumped 90.81%, reflecting strength in targeted biotech investments. CVS Corp (CVS) rose notably by 51.15%, illustrating investor demand for defensive healthcare exposure. Internationally, Alibaba Group Holding ADR (BABA) advanced 57.92%, buoyed by renewed optimism in Chinese technology.

On the downside, significant volume accompanied steep declines among speculative and technology-heavy names. Fluence Energy Inc (FLNC) led losses, plummeting 69.71%, indicative of severe investor caution toward renewables amidst broader macroeconomic concerns. SoundHound AI (SOUN) declined 58.90%, reflecting diminished confidence in AI stocks. Wolfspeed Inc (WOLF), critical within semiconductor manufacturing, dropped 56.38%, signaling persistent worries about chip demand and supply chain impacts from tariffs. Biotechnology names such as Iovance Biotherapeutics (IOVA), down 55.34%, faced amplified volatility amid uncertain regulatory environments and tariff-related cost concerns.

Notably, the quarter also highlighted an intriguing rotation from US equities toward Europe, spurred significantly by geopolitical and trade policy shifts. European equities remarkably outperformed the S&P 500 by approximately 18.4%, the widest margin in over three decades. Valuation attractiveness played a role, with the MSCI Europe Index trading at a significantly lower forward P/E compared to US counterparts. However, underlying structural shifts—such as Germany's aggressive fiscal stimulus response to evolving geopolitical dynamics—provided additional momentum, bolstering sectors like defense and infrastructure.

European indices like Germany’s Rheinmetall AG and Thyssenkrupp AG soared 113% and 130%, respectively, fueled by expectations of extended military and infrastructure spending. The Global X MSCI Greece ETF (GREK) and Spain's ETF (EWP) rose sharply, climbing 25% and 23.7%, respectively, benefiting from both regional economic recovery and increased investor inflows fleeing US volatility.

Looking ahead, markets enter Q2 2025 amid significant uncertainties shaped by tariff developments. While historical patterns suggest potential for a technical bounce in April, particularly following sharply negative March performances, the medium-term trajectory remains clouded by trade policy uncertainties and inflationary pressures. Investors must navigate carefully, balancing defensive positioning against opportunistic investments, especially as ongoing geopolitical negotiations continue to influence market sentiment and broader economic trajectories.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet