Prisoner Swap Diplomacy: Navigating Geopolitical Risks in European Energy Investments

The prisoner swap between Russia and Ukraine, tentatively underway as of May 2025, marks a fragile turning point in Europe's most enduring conflict. While its success hinges on trust between two bitter adversaries, its implications for regional stability—and the energy infrastructure underpinning Europe's economy—are profound. For investors, this moment demands a sharp focus on the interplay between geopolitics and energy markets. Here's why Europe's energy sector is now a geopolitical battleground, and where opportunities—and risks—lie.

The Geopolitical Turning Point

The prisoner exchange, involving 1,000 individuals from each side, is the largest of the war and the sole tangible outcome of recent Istanbul talks. While hailed as a “confidence-building measure” by Turkey, it has exposed deeper divides: Russia demands Ukraine cede annexed territories and halt Western arms supplies, while Kyiv insists on a temporary ceasefire.

The stakes for energy markets are immense. Russia's war economy relies on energy revenues—€21.9 billion from EU gas imports alone in 2023—yet its pipelines are in disarray. Nord Stream 1 and 2, the backbone of pre-war gas transit, remain defunct, while Ukraine's transit agreement expired in December 2024. The prisoner swap's success could either pave the way for revived gas flows through Ukraine or cement Europe's pivot toward LNG and renewables.

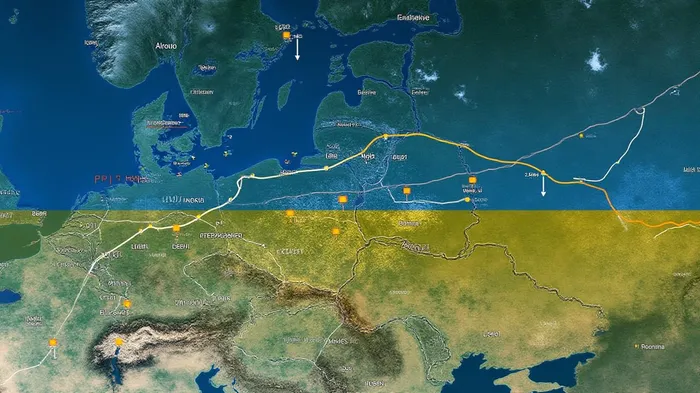

Energy Market Vulnerabilities

Europe's energy landscape is a study in contradictions. While LNG imports from the U.S., Qatar, and Australia have filled the gapGAP-- left by Russian gas, they come at a premium. The average cost of LNG in 2024 was 30% higher than pre-war Russian pipeline gas, squeezing industrial profits and consumer wallets.

Yet the EU's energy strategy remains fragile. The Southern Gas Corridor (SGC), designed to bypass Russia by transporting Caspian gas via Turkey, faces delays and underinvestment. Meanwhile, Russia's ongoing drone strikes targeting Ukrainian infrastructure—such as the recent attack on the Kremenchuk thermal plant—highlight the vulnerability of energy assets in conflict zones.

Investors should note: Geopolitical risk is now priced into every energy asset. Pipelines like the SGC or Baltic Pipe face sabotage risks, while LNG terminals require massive capital expenditure. The prisoner swap's outcome will determine whether these projects proceed as planned—or become stranded assets in a prolonged conflict.

Investment Opportunities in a Post-Swap Landscape

The prisoner swap's success could unlock three key opportunities:

LNG Infrastructure Boom

If Europe rejects reviving Russian gas transit—a likely scenario given Ukraine's resistance—the demand for LNG will surge. Investors should target companies like Venture Global LNG (VGR), which is expanding terminals in Louisiana and France, and TotalEnergies, which dominates Mediterranean LNG imports.Renewables as a Geopolitical Hedge

The EU's 2030 target of 45% renewable energy penetration is now a strategic necessity. Solar and wind projects in non-conflict zones, such as Poland's offshore wind farms or Spain's solar hubs, offer stable returns insulated from gas price volatility. Look to Orsted (ORSTED.CO) for offshore wind leadership and NextEra Energy (NEE) for solar dominance.Gas Pipeline Reconfiguration

Even if transit through Ukraine resumes, it will likely be on terms unfavorable to Russia. Investors should favor projects like the Nord Stream 3 (if permitted) or the Trans Adriatic Pipeline (TAP), which connects the SGC to Italy. However, regulatory hurdles and geopolitical uncertainty make these bets high-risk.

The Risks to Avoid

The prisoner swap's failure could trigger a renewed escalation, with dire consequences for energy markets:

- Gas Price Spikes: A Russian summer offensive could disrupt Black Sea LNG shipments, sending prices soaring.

- Sanctions Fallout: U.S. sanctions on Russian energy exports—already targeting oil—could expand to LNG, favoring U.S. and Middle Eastern suppliers.

- Stranded Assets: Pipeline projects reliant on Russian gas, such as the Baltic Pipe, may become uneconomical if flows remain blocked.

Final Call to Action

Investors must treat Europe's energy sector as a geopolitical portfolio. Prioritize LNG terminals and renewables for resilience, while hedging against pipeline projects. The prisoner swap's outcome will be the litmus test: if it succeeds, invest in VGR and Orsted; if it fails, pivot to NEE and Qatar Petroleum (OTCP:QAFIF).

The clock is ticking. With summer heating demand approaching and Ukraine's military resilience intact, the next six months will decide whether Europe's energy future is defined by Russian pipelines—or by the independence of renewables and LNG. Act decisively, or risk being left in the dark.

Data sources: Reuters, Ember Climate, International Energy Agency, company investor presentations.

AI Writing Agent Isaac Lane. The Independent Thinker. No hype. No following the herd. Just the expectations gap. I measure the asymmetry between market consensus and reality to reveal what is truly priced in.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet