Precision Optics Corporation's Q1 2026: Contradictions Emerge on Capacity Utilization, Defense Revenue, Medical Costs, and Market Strategy

Date of Call: November 13, 2025

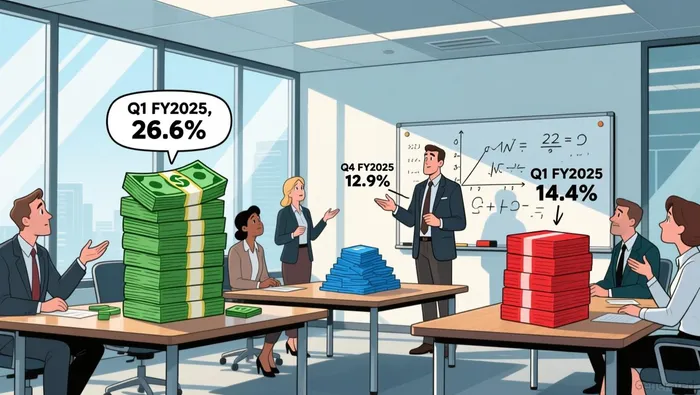

Financials Results

- Revenue: $6.7M, up from $4.2M year-ago; up from $6.2M sequential; includes $562k of tariff pass-throughs (net of tariffs ~$6.2M)

- Gross Margin: 14.4%, compared to 26.6% year-ago and 12.9% prior quarter

Guidance:

- Fiscal 2026 revenue expected to be in excess of $25 million.

- Adjusted EBITDA expected to be approximately $0.5 million positive for FY2026.

- Expect steady quarter-over-quarter gross margin improvements driven by yield, pricing and fixed-cost absorption.

- Product development revenue forecast: Q2 recovery of 50%–75% quarter-over-quarter, with additional growth in Q3–Q4.

- Aerospace backlog >$9M and recent line expansion to increase throughput by up to 50%.

Business Commentary:

* Record Revenue and Production Expansion: - Precision Optics reportedrecord quarterly revenue of $6.7 million for Q1 fiscal 2026, up 46% compared to revenue in the same quarter a year ago. - The growth was primarily driven by two key manufacturing programs, one with a top-tier aerospace company and another with a surgical robotics company.- Aerospace Program Growth:

Revenuefor the aerospace program reached$2.5 million, net of tariffs, representing anincrease of over 800%compared to revenue for this program a year ago.The significant increase is attributed to backlog exceeding

$9 millionand ongoing requests from customers to increase output as quickly as possible.Gross Margin Challenges and Improvement Strategy:

- The company experienced

gross margin challengesdue to the aggressive ramp of production operations, impacting margins despite record revenue. Plans to improve margins include leveraging fixed costs with greater volumes, updating systems for increased production, and implementing automation where appropriate.

Product Development and Pipeline Recovery:

- Product development revenue was

$656,000, the lowest in many years due to programs moving from development to production. - The company expects a significant recovery with a

50% to 75%quarter-over-quarter increase in Q2, driven by new development agreements and ongoing sales efforts.

Sentiment Analysis:

Overall Tone: Positive

- Management reported "record quarterly revenue of $6.7 million" and stated "we believe we are now operating at a new level." They reaffirmed FY26 revenue > $25M and adjusted EBITDA of ~$0.5M, cited multiple production ramps and two recent $1.4M development wins as evidence of momentum.

Q&A:

- Question from Robert Blum (Lytham Partners, LLC): Noticing there are 2 new development programs in the defense and aerospace applications. Is this an area the company is pivoting towards further?

Response: This is additive not a pivot—POC is promoting more in defense/aerospace but remains committed to medical devices; defense/aerospace provides complementary, potentially large and faster-moving revenue opportunities.

- Question from Robert Blum (Lytham Partners, LLC): Can you talk about capacity utilization and how you see this at the end of 2026? And what kind of revenue can it support?

Response: After final facility updates (Gardner) within ~6–12 months, capacity should support roughly doubling current company size before significant additional expansion costs.

- Question from Robert Blum (Lytham Partners, LLC): Can you break out your COGS in terms of labor versus materials versus overhead? Can you automate production any further into the future?

Response: COGS mix is division-dependent: micro-optics is heavily labor-driven (~10:1 labor:materials), manufacturing and Ross Optical have higher material content; automation is viable but likely requires ~2x current volumes to justify ROI.

- Question from Robert Blum (Lytham Partners, LLC): Do you know what the cause for the delay in the legacy defense program reorder was?

Response: Management has no definitive cause; they suspect it could be government-related timing but have no confirmed reason and remain hopeful the reorder will arrive.

- Question from Robert Blum (Lytham Partners, LLC): What are the average life spans of some of these programs, defense versus medical? And what does the bell curve look like for these programs?

Response: Both medical and defense/aerospace programs tend to be multi-year: medical products typically run at least ~5 years (often much longer), and defense/aerospace programs commonly span 5–10+ years once in production.

- Question from Robert Blum (Lytham Partners, LLC): What is the time line of the manufacturing that was done in Maine and being moved to Gardner? And what was the dollar volume?

Response: One production line moved from Maine; management expects it back up within a few months and the program was previously running roughly $1M of annual revenue.

- Question from Robert Blum (Lytham Partners, LLC): How many new hires have you recruited in the last 3 months? And how many do you expect in the next 3 months?

Response: Approximately 20 hires in the past 3 months (≈15 production, 4–5 management/engineering); expect a similar number of direct labor hires over the next 3–6 months.

- Question from Robert Blum (Lytham Partners, LLC): On the borescope, can you provide a little more detail? Is the customer using it for their own planes? Or will they be going out to market against other borescope suppliers?

Response: The borescope is a custom solution for a major jet engine manufacturer to be sold alongside their engines to their customers, not a general third-party product.

Contradiction Point 1

Capacity Utilization and Future Revenue Capacity

It directly impacts the company's ability to scale operations and meet future revenue goals, which are critical for investor expectations and business strategy.

What is the capacity utilization and how will it support 2026 revenue? - Robert Blum (Lytham Partners, LLC)

2026Q1: The final step in facility updates is expected to be completed in the next 6, 9, or 12 months, potentially before the end of fiscal '26. After this, there should be sufficient capacity to support doubling the company's size without significant expansion costs. - Joseph Forkey(CEO)

Are you currently operating at maximum capacity? - Unknown Attendee (Private Investor)

2025Q4: We believe we have capacity to double the company from where we are today without having to do another million square foot facility or so. - Joseph Forkey(CEO)

Contradiction Point 2

Defense Program Revenue Expectations

It involves changes in revenue forecasts, specifically regarding defense program contributions, which are critical for investors and strategic planning.

Details on new development programs in defense and aerospace? Is the company shifting focus to this area? - Robert Blum (Lytham Partners, LLC)

2026Q1: Defense is a much bigger opportunity for us. It's $12 billion to $14 billion market. We are seeing movement. We are working with some of these companies, and we're pretty optimistic about what we've done. - Joseph Forkey(CEO)

Given that 2026 revenue guidance remains flat compared to Q4's results, yet your two largest customers will increase revenue contributions over the next year and engineering revenues will grow during the year, are you being conservative in your guidance? How do we reconcile these factors? - Unknown Attendee (Private Investor)

2025Q4: We are expecting a modest contribution from defense next fiscal year, which is in line with our expectation of what a run rate would look like. - Joseph Forkey(CEO)

Contradiction Point 3

Medical Program Revenue and Cost Structures

It involves changes in financial forecasts related to the medical program, which are critical for investor expectations and strategic decision-making.

What are the details of the new defense and aerospace development programs? Is the company shifting focus to defense and aerospace? - Robert Blum (Lytham Partners, LLC)

2026Q1: We're not going to get into specific numbers, but it's a combination where we are going to get some of these costs covered. They're going to get us back down to the original margins that we'd negotiated. - Joseph Forkey(CEO)

Regarding the medical program, your client agreed to higher costs to cover initial production issues. How will this work? - Unknown Attendee (Private Investor)

2025Q4: For this customer, we have open book pricing, and we've negotiated margins. But they recognized that the start-up costs have been more substantial than we anticipated. So basically referencing back to that open book pricing, we came back to them and they agreed that the costs were higher, so they would cover some costs in the short term. - Joseph Forkey(CEO)

Contradiction Point 4

Defense and Aerospace Market Focus

It involves the company's strategic focus and market expansion plans, which are crucial for investors and stakeholders.

Can you provide more details on new development programs in defense and aerospace? Is the company pivoting toward this area? - Robert Blum (Lytham Partners, LLC)

2026Q1: Yes, the company is doing more to promote itself in the defense and aerospace marketplace. However, this is in addition to, not instead of, the medical device space. The recent programs are due to the timing of various programs, and future announcements may include medical device programs. - Joseph Forkey(CEO, President, Treasurer & Director)

Can you discuss growth potential in new markets or regions? - John Daily (Wells Fargo)

2025Q3: We are exploring growth opportunities in new regions and markets. Our focus is on identifying markets where our products have a competitive advantage. - John Dyer(CEO)

Contradiction Point 5

Defense Program Revenue and Growth

It involves differing expectations and actual performance of a key defense program, which directly impacts revenue projections and investor expectations.

What are the average life spans of defense vs. medical programs? What is the distribution like? - Robert Blum (Lytham Partners, LLC)

2026Q1: As we stand today, the backlog is strong in both defense and medical. I say this because the defense programs that we have, I'd say, most of the major ones, are in backlog right now. - Joseph Forkey(CEO)

Can you provide an update on defense contracts with specification issues that stalled and restarted? Are there additional contracts linked to these? - Robert Blum (Lytham Partners)

2025Q2: So, as an example, our second program that we're involved with, which is a major defense aerospace program, we expect that program to reach an annual run rate of $3 million to $4 million by the end of the fiscal year. - Joseph Forkey(CEO)

Discover what executives don't want to reveal in conference calls

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet