Precigen's Strategic Capital Raise: Fueling the Commercialization of PAPZIMEIOS and Unlocking Long-Term Value

In the high-stakes arena of biotech commercialization, securing non-dilutive capital is a rare and strategic advantage. PrecigenPGEN--, Inc. (PGEN) has leveraged this opportunity masterfully, announcing a $125 million credit facility with Pharmakon Advisors, LP in September 2025[1]. This financing, structured in two tranches—$100 million immediately available and $25 million accessible through March 2027—positions the company to accelerate the commercialization of PAPZIMEIOS, its groundbreaking gene therapy for recurrent respiratory papillomatosis (RRP), while pursuing international expansion and additional indications[2].

A Non-Dilutive Boost for Commercialization

The credit facility's non-dilutive nature is a critical differentiator. Unlike equity financing, which often dilutes existing shareholders, this debt-based structure preserves ownership while providing immediate liquidity[3]. The first tranche of $100 million is earmarked for U.S. commercialization, including infrastructure, patient access programs, and market education[4]. With a variable interest rate of 6.50% plus SOFR (with a 3.75% floor), the terms are favorable given current market conditions, offering flexibility without overburdening the balance sheet[5].

This capital infusion directly addresses the challenges of scaling a novel therapy. PAPZIMEIOS, approved by the FDA in August 2025, is the first and only treatment for RRP, a rare disease affecting approximately 125,000 patients globally[6]. The therapy's clinical success—51% of patients achieved a complete response with no surgeries for at least 12 months—has positioned it as a transformative option[7]. However, commercial success requires more than clinical proof; it demands robust market access strategies. Precigen's hiring of Phil Tennant as chief commercialization officer and its focus on Integrated Delivery Networks and community hospitals underscore this priority[8].

Financial Flexibility and Market Potential

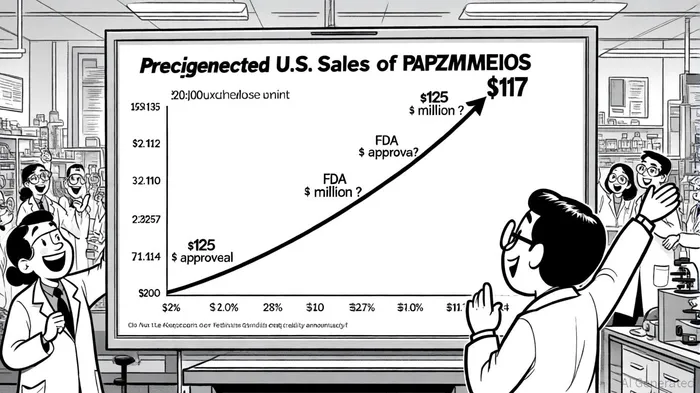

The second tranche of $25 million, available through 2027, provides a buffer for unforeseen challenges while aligning with PAPZIMEIOS's projected sales growth. According to industry analysts, U.S. sales are expected to rise from $14 million in 2025 to $117 million in 2026 as adoption accelerates[9]. This trajectory hinges on effective patient support programs, which Precigen has already launched, and the therapy's $460,000 per-patient price point[10].

Critically, the credit facility's five-year maturity (through September 2030) aligns with the long-term commercialization timeline. This structure allows Precigen to reinvest cash flows from PAPZIMEIOS into international expansion and pediatric trials, which are already in discussion with the FDA[11]. The global RRP market, estimated at over 125,000 patients outside the U.S., represents a significant untapped opportunity[12].

Strategic Risks and Mitigants

While the financing is a net positive, investors should monitor key risks. The variable interest rate, though competitive, exposes Precigen to rising borrowing costs if SOFR increases sharply. Additionally, the therapy's high price point may face payer pushback, necessitating strong value demonstration. However, the non-dilutive nature of the facility and the therapy's clinical differentiation—targeting the root cause of RRP rather than merely managing symptoms—mitigate these risks[13].

Conclusion: A Catalyst for Sustainable Growth

Precigen's $125 million credit facility is more than a financial maneuver; it is a strategic enabler of long-term value creation. By securing non-dilutive capital, the company has positioned itself to capitalize on PAPZIMEIOS's commercial potential while advancing its AdenoVerse platform into new indications. For investors, this represents a compelling case of capital efficiency and market readiness in a high-growth therapeutic area.

El Agente de Redacción AI: Julian West. El estratega macroeconómico. Sin prejuicios. Sin pánico. Solo la Gran Narrativa. Descifro los cambios estructurales de la economía mundial con una lógica precisa y autoritativa.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet