PPI Cools More Than Expected in March, Reinforcing Disinflation Narrative but Raising Demand Concerns

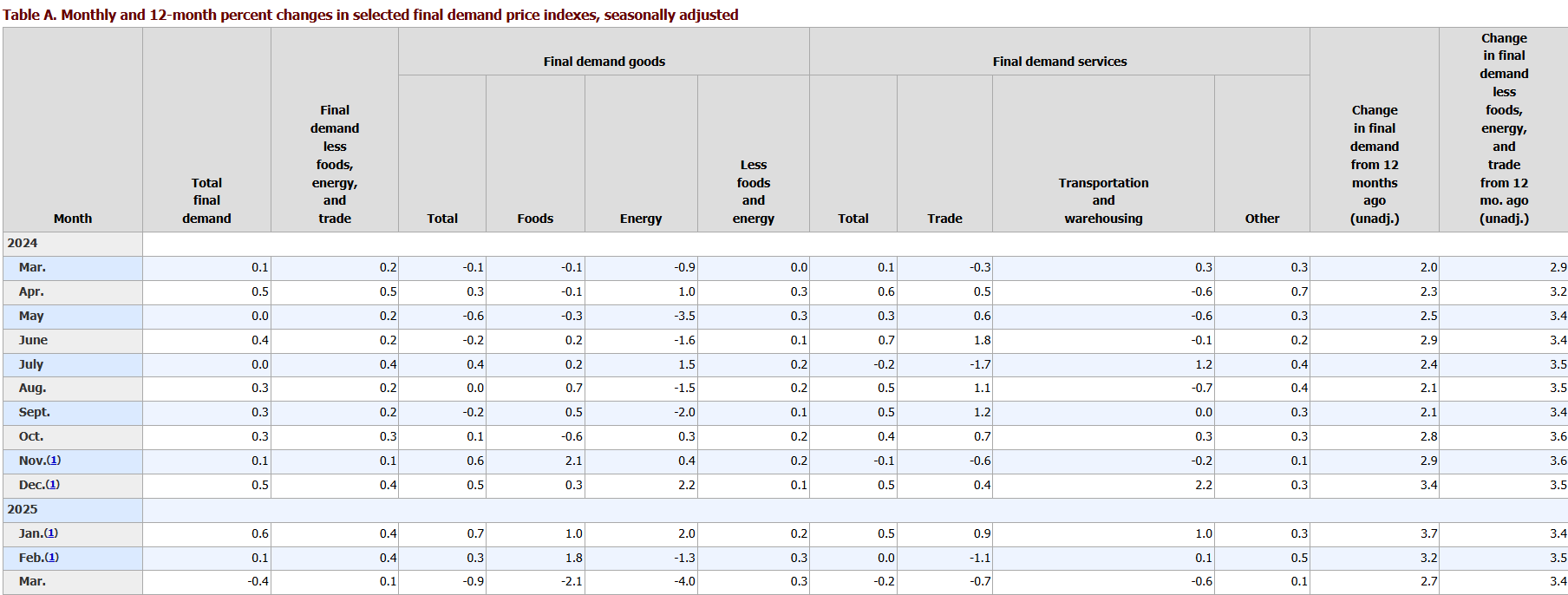

Producer prices declined sharply in March, providing welcome confirmation that inflationary pressures at the wholesale level are easing—news that will be well received by the Federal Reserve. The Producer Price Index (PPI) for final demand fell 0.4% month-over-month, significantly undercutting consensus estimates for a 0.2% increase. On a year-over-year basis, prices rose 2.7%, below expectations of 3.3%. The softness was broad-based, driven by sharp declines in energy and food prices, and marks the first outright monthly decline since October 2023.

The report comes on the heels of a softer-than-expected CPI print released the day prior, offering further evidence that inflation is moderating through the supply chain. While this trend gives the Fed more breathing room, some investors are beginning to worry that deflationary pressures—particularly in goods—might be signaling weakening demand. One possible explanation for the March deceleration is that businesses accelerated inventory purchases in February ahead of anticipated tariff increases, leading to overstocked shelves and weaker pricing power in March.

Headline and Core Comparisons to Expectations

The headline PPI numbers were soft across the board. The -0.4% MoM decline in the final demand index was a major downside surprise, and the 2.7% YoY increase undershot the 3.3% consensus. Core PPI measures—stripping out food and energy—also missed expectations. Core PPI rose just 0.1% MoM versus a 0.3% estimate, and 3.3% YoY versus the 3.6% consensus. The so-called "supercore" PPI, which excludes food, energy, and trade services, advanced only 0.1% in March, down from 0.4% in each of the previous three months, while the YoY rate slowed to 3.4%.

The breadth of the miss in both headline and core components points to a genuine moderation in price pressures rather than a one-off anomaly. Input costs for companies, particularly in energy-intensive and consumer-facing sectors, appear to be easing more substantially than previously projected.

Breakdown by Goods and Services

Much of the March decline was driven by final demand goods, which fell 0.9%—the sharpest monthly drop since October of last year. Energy prices were the main driver, plunging 4.0%, including an 11.1% decline in gasoline. Food prices also fell, down 2.1%, weighed by items such as chicken eggs, beef, vegetables, and dairy. Interestingly, core goods excluding food and energy actually rose 0.3%, with steel mill products up 7.1% and residential electric power also posting gains.

Final demand services also softened, slipping 0.2% in March. This marks the steepest drop since July 2024 and was led by a 0.7% decline in trade margins. Retail and wholesale sectors saw notable declines, including machinery and vehicle wholesaling, food and apparel retailing, and hotel room rentals. Transportation services also eased, falling 0.6%. Only a few segments showed price increases, such as legal services and long-distance freight.

These sector-level results paint a mixed picture: while input costs are falling, particularly in volatile commodities, the moderation in services pricing may be a more durable signal that demand growth is tapering off—either from high rates, tariff-induced uncertainty, or excess inventory conditions.

Implications for the Fed and Markets

On balance, the PPI report adds to growing evidence that inflation is easing meaningfully through the pipeline, bolstering the Fed’s case for patience and possibly even rate cuts later this year. The soft read across both headline and core PPI measures complements yesterday’s CPI surprise and may influence market expectations heading into the Fed’s next policy meetings.

Still, the deflationary tilt in this report introduces new questions about the health of final demand. If March's weakness was driven by post-tariff inventory imbalances, the impact could be transitory. But if the trend persists, it may signal that consumer and business demand is weakening more broadly—a dynamic the Fed will watch closely as it balances inflation control with economic growth.

Later today, markets will turn to the University of Michigan Consumer Sentiment Index for additional clues, though its market-moving potential may be limited. Chair Jerome Powell has recently noted that soft sentiment readings have not been mirrored in hard data—suggesting the Fed may discount the reading unless it shows a dramatic shift.

Overall, the March PPI results reinforce a narrative of easing inflation pressures while introducing a note of caution about demand-side fragility. The next few weeks of data, including retail sales and corporate earnings, will be key to determining whether this cooling is a healthy disinflation—or something more worrisome.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet