Powell Slams Brakes on December Cut: Fed Ends QT but Cools Market Euphoria With ‘Driving in Fog’ Warning

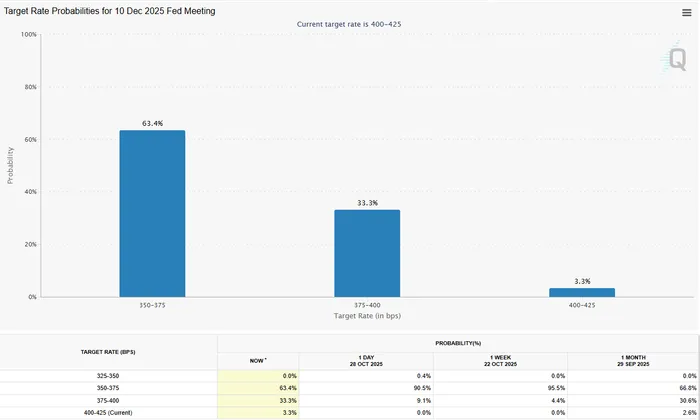

Markets got exactly what they penciled in from the Fed—another 25 bp cut and a formal end to QT on December 1—but Chair Powell cooled the punch bowl with a clear message on December: “A further reduction in the policy rate at the December meeting is not a forgone conclusion. Far from it.” Futures heard him. The CME Fed Funds contract-implied odds for a December cut slid to roughly 63% from about 90% pre-presser, taking some air out of the “auto-pilot easing” narrative even as today’s move nudged policy closer to neutral.

Powell framed the decision as risk management amid two-sided risks that have shifted further toward the labor side. “With downside risks to employment increased in recent month, the balance of risk has shifted,” he said, explaining today’s 25 bp step as another move “toward a more neutral policy stance.” But he drew a bright line under December: “Policy is not on a preset course.” If the data turn foggy due to delayed government releases, the Committee may err on the side of patience: “What do you do if you are driving in the fog? You slow down.”

On the economy, Powell described an outlook defined by sturdier growth but only gradual labor cooling. Participants are “noticing stronger economic activity,” while the labor market “may be continuing to gradually cool.” He emphasized that claims aren’t rising and job openings aren’t falling sharply, implying the labor side is softening without cracking. That nuance matters for December: if growth proves resilient and labor remains merely “gradually” cooler, the case for back-to-back cuts is weaker—especially with inflation progress mixed beneath the hood.

On inflation, Powell broke it into the familiar three buckets. Goods prices are running hotter—“that is really due to tariffs,” a reversal from the pre-2021 pattern of mild goods deflation. Housing services inflation “has been coming down… and we expect [it] to continue.” The sticky piece is core services ex-housing, which “has kind of been moving sideways over the last few months.” Netting those forces, he reiterated that the risks to inflation are still to the upside even as the employment side has grown more fragile—hence the Committee’s reluctance to signal another cut six weeks from now.

The balance sheet pivot was telegraphed—and delivered. The Fed will “conclude the reduction of our aggregate security holdings as of December 1.” Powell said the threshold for stopping runoff—reserves “somewhat above” ample—has been met, citing money-market signals: “repo rates have moved up relative to administered rates… [and] the effective federal funds rate has begun to move up relative to the interest on reserve balances.” After three and a half years of QT, Fed holdings are down $2.2 trillion; as a share of nominal GDP, the balance sheet has fallen “from 35% to about 21%.”

What comes next is a holding pattern—then a slow turn. Freezing the balance sheet doesn’t freeze reserves; as non-reserve liabilities (like currency in circulation) grow, reserves will “continue to move gradually lower.” At some point, the Fed will need to resume adding reserves to keep pace with the banking system, but “not for a long time.” Composition will also evolve: the Fed will let agency MBS roll and reinvest into T-bills to push the portfolio “closer to that of the outstanding stock of Treasury securities,” i.e., shorter duration. The timing will be glacial—“very, very gradually”—but the direction is clear: fewer MBS, shorter WAM, more Treasuries.

Duration and reserves featured prominently because the market has been sniffing at scarcity. Powell acknowledged “gradual tightening in money market conditions” in recent weeks, reinforcing the rationale to stop runoff now rather than wring out the “last few dollars.” The message: the Fed prefers an ample-reserves regime and will preserve it, even if that means ending QT a bit earlier than balance-sheet hawks might like.

Policy strategy from here is deliberately unscripted. Powell stressed the Committee saw “strongly differing views” about December. With the policy rate now in the 3–4% zone—“where most estimates of… the neutral rate live”—some participants want to “take a step back and see whether there really are downside risks to the labor market,” especially with activity data running hot. That helps explain why today’s cut didn’t come bundled with a wink toward another one.

On AI-powered capex and the data-center boom, Powell was careful not to over-ascribe causality to rates. He noted that AI build-outs are “based on longer-run assessments” and aren’t “really about 20 basis points here or there,” pushing back on the idea that modest near-term easing would supercharge bubble dynamics in that corner of investment. More broadly, he reiterated the Fed’s remit: “We use our tools to support the labor market, and to create price stability.”

Credit and consumer health questions drew watchful but unalarming responses. The Fed sees rising stress in subprime autos and pockets of delinquencies, but Powell doesn’t view it as systemic: “It doesn’t seem to be something that has very broad application across financial institutions… we are going to be monitoring this quite carefully.” On wealth effects, he reminded that the marginal propensity to consume diminishes at higher wealth levels—markets matter for spending, but not one-for-one.

Net-net, the decision itself was as-expected; the tone was a shade more hawkish because Powell explicitly removed any presumption of a December follow-up. That tweak knocked cut odds down to the low-60s, aligning pricing with an Fed that’s now closer to neutral and data-dependent into year-end. With QT ending and a shorter-duration portfolio ahead, balance-sheet policy shifts to “steady as she goes.” Unless incoming data materially deteriorate—or inflation’s “sideways” services bucket cracks lower—Powell just told you to fade the idea of a pre-committed December cut. In his words: it’s “not a forgone conclusion. Far from it.”

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet