Powell’s ‘Risk Management’ Cut

The Federal Reserve’s September decision and Chair Jerome Powell’s post-meeting press conference left investors with plenty to chew on—and little in the way of a clear takeaway. In true Rorschach fashion, hawks and doves alike could find support for their views, and the S&P 500 futures reflected that ambivalence. They opened Powell’s press conference near 6665, fell sharply mid-conference, only to close out the session right back at 6665, a round trip that underscored the market’s uncertainty.

At the center of that volatility was Powell’s description of the quarter-point cut as a “risk management” move. Markets initially slipped to session lows when he used that phrase, as traders were reminded of his 2019 “midcycle adjustment” framing. Back then, what was meant to reassure investors instead spooked them, triggering a sharp sell-off on concerns that the Fed might deliver only a token easing. The comparison was unavoidable, and Powell’s cautious tone reignited fears that this September cut could also prove a one-and-done adjustment rather than the start of a sustained easing cycle.

Still, Powell and the Committee were quick to emphasize that today’s move came in response to a tangible shift in the balance of risks. Inflation risks, while still present, are now seen as slightly less pressing than earlier this year. Goods prices are rising again, largely due to tariffs, but Powell stressed that the Fed views those pressures as temporary—essentially a one-time level shift rather than the onset of a new inflation cycle. Services disinflation continues, and longer-term inflation expectations remain consistent with the 2% target. The message: inflation is still elevated, but the risk of it breaking out again has diminished.

The real story, according to Powell, lies in the labor market. Job growth has slowed significantly, payroll gains are running well below breakeven levels, and the unemployment rate has crept up. Powell called the current dynamic “unusual”: both labor supply and demand have softened, but demand is fading faster. Immigration-driven labor supply growth has slowed, while employers have reduced hiring. That mix leaves the economy vulnerable—Powell warned that if layoffs accelerate in this environment, unemployment could rise quickly given the low hiring rate. For the first time in this cycle, the Fed’s statement explicitly acknowledged that downside risks to employment have risen.

That change in emphasis explains why Powell described the Fed’s stance as moving toward neutral. Policy has been “restrictive” throughout 2024, and until recently the Fed’s bias was firmly skewed toward fighting inflation. But as Powell said today, “our policy had been skewed toward inflation; now we are moving in the direction of more neutral.” He argued that a more balanced stance will better support the labor market without abandoning the inflation fight. Importantly, he also signaled there was no widespread support for a larger 50-basis-point cut—suggesting the Committee is still wary of moving too aggressively at this stage.

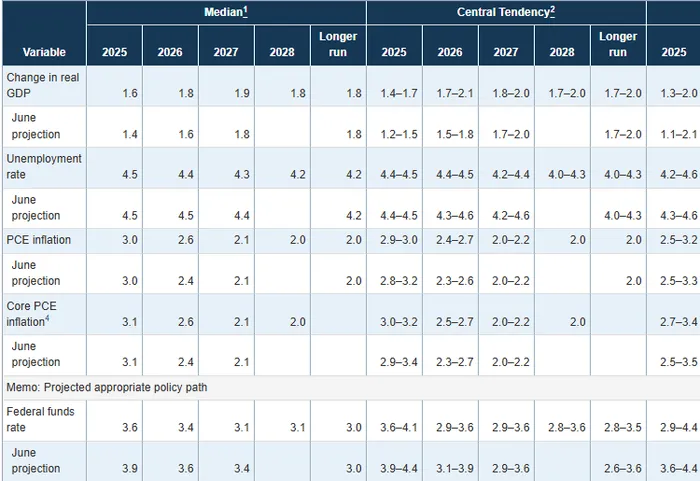

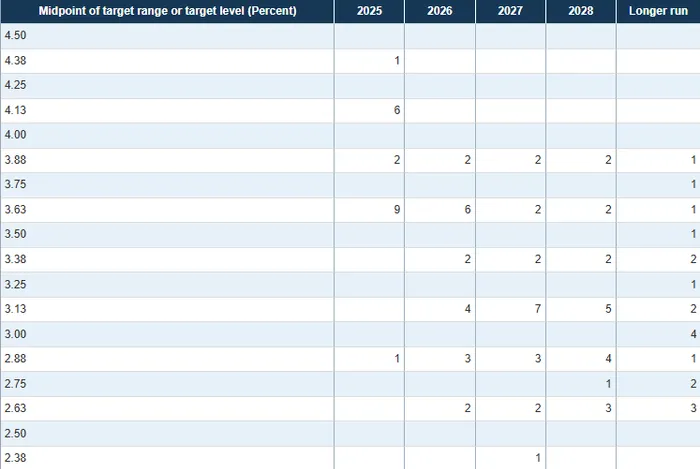

The Summary of Economic Projections released alongside the decision underscored that point. While the median forecast for the fed funds rate fell to 3.6% for 2025 from 3.9% in June, the 2026 and 2027 projections were only modestly lower, and inflation estimates for 2026 ticked higher. That mix suggested a gentler path of easing than markets had hoped, balanced by a recognition that inflation will take time to fully subside. Powell framed the SEP as a set of probabilities rather than a plan, reminding investors that policy is not on a preset course.

For the markets, the ambiguity was both frustrating and familiar. Powell’s insistence that today’s cut was about “risk management” led some to worry that the Fed may be setting the stage for a prolonged pause. At the same time, his emphasis on rising downside risks to employment was welcomed by those arguing the Fed has been too slow to pivot. With ten policymakers penciling in two or more cuts for the remainder of the year and ten penciling in fewer, the dispersion of views on the Committee mirrors the broader debate in markets.

Beyond the policy mechanics, Powell also kept the tone constructive on the broader economy. He noted that consumer spending remains resilient—albeit skewed to higher-income households—and that business investment has picked up. Credit conditions are holding up, and the Fed still views the economy as fundamentally solid. In that sense, today’s rate cut was not a response to imminent crisis, but rather a recalibration to prevent restrictive policy from choking off a still-healthy expansion. Powell’s comments suggested confidence that the U.S. economy has the strength to absorb the tariff shock and softer jobs data, provided rates are adjusted to reflect the new risk balance.

The irony of the day was that, for all the back-and-forth, markets ended exactly where they began. The S&P futures at 6665 were unchanged from 2 p.m. to the end of Powell’s press conference, though the intraday swings revealed just how sensitive investors are to the Fed’s tone. For bulls, the message was that the Fed is easing in the face of labor softness. For bears, the warning was that the Fed might not cut enough—or fast enough—to avert deeper weakness.

Ultimately, Powell’s press conference reinforced the idea that the Fed is trying to thread a needle between managing inflation risks and cushioning the labor market. Today’s cut may not mark the start of an aggressive easing cycle, but it does acknowledge the economy needs breathing room. Whether markets see it as a one-off “midcycle adjustment” or the first step in a broader pivot will depend on incoming data. As Powell made clear, the Fed is in “a meeting-by-meeting situation,” and the next move will be dictated by how the economy evolves.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet