Powell’s Jackson Hole Speech Could Make or Break Market Rally

WATCH: Bitcoin $200K? The math behind the next crypto supercycle.

The world’s central bankers, academics, and policymakers will converge later this week in the Grand Tetons for the annual Jackson Hole Economic Policy Symposium. Hosted by the Kansas City Fed, the conference runs from August 21–23 at the Jackson Lake Lodge, with Federal Reserve Chair Jerome Powell set to deliver the keynote address on Friday, August 22, at 10:00 a.m. ET. His speech, titled “Economic Outlook and Framework Review,” will focus on the conference theme of “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy.” The timing and subject matter carry outsized importance, as the Fed faces a weakening labor market, sticky inflation pressures, and heightened political pressure from the White House.

This year’s symposium is being watched with particular intensity because of Powell’s dual challenge: managing a cooling employment backdrop while inflation risks remain elevated. Markets are leaning toward a dovish interpretation, suggesting that the Fed is preparing to pivot toward rate cuts. Yet Powell may not be ready to fully endorse that narrative, especially with another round of jobs data, CPI, and PPI prints still to come before the September FOMC meeting. That tension makes Jackson Hole the ultimate stage-setter for the fall.

CME Fed Fund Futures (September cut expectations):

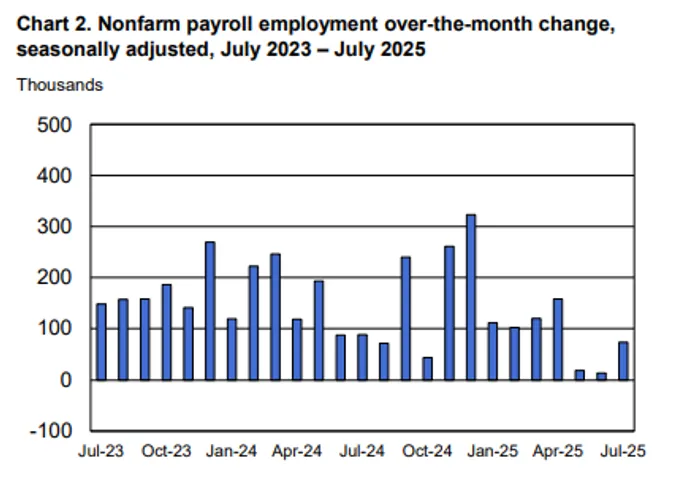

Employment will be front and center. Payroll growth slowed dramatically in July, with just 73,000 jobs added, while May and June figures were revised lower by more than 250,000. Wage growth has also decelerated from 6% in 2022 to below 4%. For Powell, who has emphasized the Fed’s dual mandate of stable prices and maximum employment, these developments demand attention. Investors view the labor market softening as the Fed’s green light to cut rates, but Powell may stress that the market is still “in balance.” Initial jobless claims remain historically low, suggesting companies are not yet shedding workers en masse. This “no hire, no fire” dynamic complicates the dovish case.

Inflation remains the other half of the equation. The July CPI report showed moderation, with headline prices up just 0.2% month-over-month and 2.7% year-over-year. Core CPI ticked higher, rising 0.3%, marking the largest increase since January. More concerning was the Producer Price Index, which surged 0.9% in July, the biggest monthly gain in over three years. The jump in services prices, up 1.1%, suggests pipeline pressures are building. Tariffs imposed on August 1 are feeding into these dynamics, raising costs for importers and threatening to spill over into consumer prices. Powell is likely to acknowledge that tariffs represent a major upside risk, even if current consumer inflation readings look contained.

Against that backdrop, markets are nearly unanimous in expecting action. According to the CME FedWatch tool, odds of a 25-basis-point cut at the September meeting sit above 80%. Fed funds futures imply about 55 basis points of easing by year-end, down modestly from last week’s expectations after the PPI surprise. Looking ahead to 2026, investors are penciling in at least three additional cuts, with some analysts suggesting as much as 150–175 basis points of easing across the year. Equities have rallied on this outlook, with the S&P 500 and Nasdaq near record highs and small caps outperforming on the assumption that lower borrowing costs will cushion tariff-related damage.

But Powell may hesitate to validate those assumptions. The Fed has been burned before by premature declarations. His 2021 “transitory” characterization of inflation remains a scar on credibility, and the chair may prefer to retain optionality. By stressing that the Fed wants to see “more information” before committing, Powell could temper market expectations without explicitly pushing back. This would leave September a “live” meeting, but not a guaranteed one, especially if incoming data surprise to the upside on inflation.

The political overlay adds another layer. President Trump has made no secret of his desire for cuts to reduce government borrowing costs and stimulate growth ahead of the election cycle. Reports suggest he has even threatened Powell’s tenure if the Fed does not comply. While Powell is unlikely to address political dynamics directly, the pressure hangs over the proceedings. History is littered with examples of political interference in monetary policy, from Nixon and Arthur Burns in the 1970s to Turkey’s central bank crises more recently. Powell, by all accounts, sees preserving the Fed’s independence as his defining legacy.

In previewing his remarks, it’s helpful to recall last year’s Jackson Hole appearance. Then, Powell used the stage to prepare markets for policy normalization, which was followed by a rate cut at the September FOMC meeting. This year’s situation is more ambiguous. Labor market weakness argues for easing, but tariff-driven inflation argues for caution. Powell is likely to walk that fine line, acknowledging risks on both sides. Expect references to “balance,” “uncertainty,” and the need for additional data.

The market impact could be substantial. A speech that tilts dovish—emphasizing employment risks and signaling comfort with a September cut—would likely push yields lower, the dollar weaker, and equities higher. A more cautious tone, focused on inflation and tariffs, could spark disappointment, especially given current valuations. With the Shiller P/E already near 40, markets are priced for perfection. Any deviation could trigger volatility, particularly in rate-sensitive small caps and tech. The VIX remains near cycle lows, suggesting traders are not hedged for surprise.

Looking beyond the near-term policy debate, Powell will also address the Fed’s ongoing framework review. Every five years, the central bank re-evaluates its approach, and this cycle may see a return to describing “deviations” from maximum employment, rather than “shortfalls.” This subtle shift would give the Fed equal license to raise rates when labor markets overheat and cut when they weaken. That recalibration could shape policy well beyond Powell’s tenure.

Ultimately, Jackson Hole 2025 is less about a single policy signal and more about how Powell frames the tradeoff between employment and inflation in an era of tariffs and political pressure. Markets want clarity, but Powell may prefer flexibility. Investors should be prepared for either outcome: a dovish signal that validates rate-cut bets, or a cautious tone that forces a reset of expectations. Either way, Friday’s speech will define the conversation heading into the September FOMC meeting and, potentially, Powell’s legacy as Fed chair.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet