Powell Industries: A Cautionary Tale of Sector Volatility and Cash Flow Woes

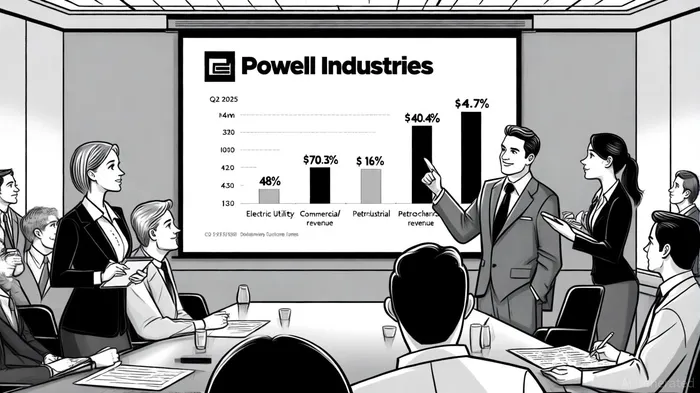

When it comes to industrial stocks, Powell IndustriesPOWL-- (POWL) has been a rollercoaster ride for investors. On the surface, the company's Q2 2025 results look impressive: revenues jumped 9% year-over-year to $279 million, driven by a 48% surge in the Electric Utility sector and a 16% gain in Commercial/Industrial markets [1]. Net income soared 38%, and gross margins expanded by 530 basis points, reflecting operational efficiencies [2]. But dig deeper, and the story gets murkier.

Sector Volatility: A Double-Edged Sword

The Petrochemical sector's 13% revenue decline is a red flag. While Electric Utility and Commercial/Industrial segments are firing on all cylinders, this underperformance suggests Powell is at the mercy of cyclical swings in energy markets [3]. For context, the S&P 500 industrial sector has shown more balanced growth over the past year, with energy transition plays offsetting declines in traditional sectors [4]. Powell's overreliance on volatile markets like Petrochemicals—where demand is tied to commodity prices—could expose it to sudden headwinds.

Cash Flow Discrepancies: A Hidden Weakness

Here's where the numbers get concerning. Despite a 33% jump in gross profit, Powell's adjusted operating cash flow fell to $59.5 million in Q2 2025, down from $100.9 million in the prior year [5]. This divergence hints at working capital issues or lumpy project-based revenue recognition. Compare this to the S&P 500 industrial average, where free cash flow has trended upward as companies optimize supply chains and reduce inventory costs [6]. Powell's cash flow struggles could limit its ability to reinvest in growth or weather a downturn.

Backlog Stagnation: A Signal of Stagnant Demand?

The company's backlog of $1.3 billion has remained unchanged for two consecutive quarters and two years [7]. While management attributes this to disciplined order fulfillment, it also raises questions about new contract acquisition. In contrast, peers in the industrial sector have seen backlogs grow as demand for energy transition infrastructure (e.g., hydrogen, carbon capture) accelerates [8]. Powell's stable backlog may reflect a lack of momentum in securing next-generation projects, which could cap long-term growth.

Stock Performance: Outperformance vs. Volatility

POWL's stock has outperformed the S&P 500 over the past 12 months (+34.65% vs. +16.52%) [9], but its recent volatility tells a different story. In early 2025, the stock plummeted 23.5% year-to-date, underperforming both the S&P 500 and the broader Industrial Products sector [10]. This whipsaw effect—driven by sector-specific risks and management's admission of a “seasonally slower” first quarter—suggests the stock is more susceptible to macroeconomic jitters than diversified industrials [11].

The Bottom Line: Caution Amidst the Optimism

Powell's financials are undeniably strong on paper—low debt, robust liquidity, and expanding margins. But investors should not ignore the structural risks: sector concentration, cash flow inconsistencies, and a stagnant backlog. While the company's pivot to energy transition markets (e.g., hydrogen, LNG) is promising, execution will be key. For now, the stock's valuation—trading at a forward P/E of 11.99X, well below the industry average of 22.16X—offers some upside, but only if management can address these operational red flags.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet