Post Holdings Q4 2025: Contradictions Emerge on M&A Strategy, Capital Allocation, Supply Chain Flexibility, and Cereal Segment Performance

Date of Call: None provided

Financials Results

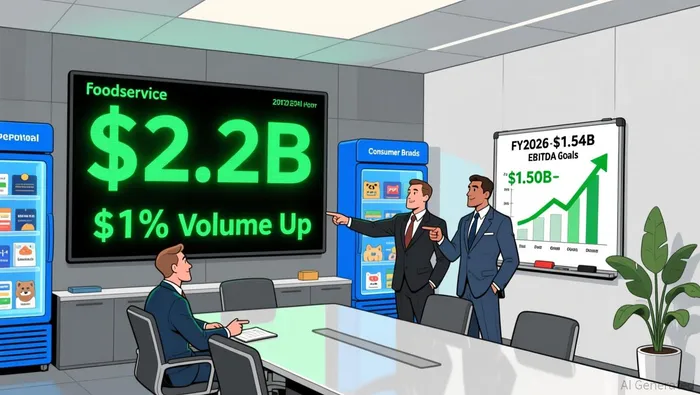

- Revenue: $2.2B consolidated net sales in Q4, up 12% YOY (driven by Eighth Avenue acquisition)

Guidance:

- FY2026 adjusted EBITDA expected $1.50B-$1.54B (approximately 1%-4% growth to a normalized FY2025)

- Q1 adjusted EBITDA expected to decrease meaningfully vs FY25 Q4 due to HPAI normalization and U.S./U.K. cereal seasonality; second half expected to be favorable to the first

- CapEx guidance $350M-$390M (notably below FY2025)

- Expect a meaningful increase in FY2026 free cash flow from lower CapEx and tax law benefits

- Two months of pasta contribution in FY2026; Eighth Avenue expected to contribute ~$45M-$50M run-rate with ~$15M synergies by year-end

Business Commentary:

* Diverse Growth and Capital Allocation: - Post Holdings reported strong fiscal 2025 results, with notable growth in the foodservice sector and cash flow generation, allowing for capital investments and acquisitions. - The growth was driven by the diversification of its business portfolio, navigating regulatory changes and tariffs, as well as the benefits of cost reductions and strategic acquisitions.

* Diverse Growth and Capital Allocation: - Post Holdings reported strong fiscal 2025 results, with notable growth in the foodservice sector and cash flow generation, allowing for capital investments and acquisitions. - The growth was driven by the diversification of its business portfolio, navigating regulatory changes and tariffs, as well as the benefits of cost reductions and strategic acquisitions.- Consumer Brands and Pet Challenges:

- Post's consumer brands saw a decline in net sales, with cereal volumes decreasing by

8%and pet volumes by13%. The decrease was attributed to category and competitive dynamics, combined with the impact of private label business losses and brand reset challenges.

Cold Chain Business Resilience:

- The company's cold chain businesses, including foodservice and refrigerated retail, showed resilience amidst challenges like avian flu (HPAI).

This was achieved through effective cost management and strategic manufacturing execution, which offset lower retail volumes.

Avian Flu Impact and Foodservice Momentum:

- The foodservice segment reported a

20%increase in net sales, driven by an11%volume increase and avian flu-driven pricing. The segment's growth was supported by increases in egg, potato, and shake volumes, with ongoing recovery from HPAI-related disruptions.

Financial Performance and Outlook:

- Post Holdings generated

$301 millionfrom operations in the quarter, with a free cash flow of approximately$150 million. - For fiscal 2026, the company anticipates adjusted EBITDA in the range of

$1.50 billion-$1.54 billion, reflecting a1%-4%growth rate compared to a normalized FY 2025.

Sentiment Analysis:

Overall Tone: Positive

- Management: "We had a good fiscal year 2025, and we ended with a strong quarter." "I like our positioning." CFO: "We generated $301 million from operations... Free cash flow for the full year was nearly $500 million." Guidance: "we expect a meaningful increase in FY 2026 free cash flow."

Q&A:

- Question from Andrew Lazar (Barclays): Maybe, Rob, to start off, we’ve certainly seen industry volume remain sort of challenged... I guess I’m curious how this dynamic sort of informs your capital allocation decisions. Is M&A still the right approach, given how cheap assets are? Is buying back stock at these levels more sensible...?

Response: We evaluate M&A versus buybacks on a risk‑adjusted return basis and will pursue focused, value‑adding M&A rather than size alone; we do not have a blanket preference for buybacks over deals.

- Question from Andrew Lazar (Barclays): On the asset optimization efforts in ready‑to‑eat cereal, if the category continues weak, what further cost actions could be considered?

Response: Additional cost reductions are available but of smaller magnitude now; focus will shift to line optimization rather than further large plant closures.

- Question from Tom Palmer (JPMorgan): Thinking through segments for fiscal 2026, which ones do you see as being more consistent with that normalized outlook after adjusting for M&A and avian flu?

Response: PCB legacy is expected to be roughly flat in FY26; the balance of the portfolio is expected to perform in line with our algorithmic assumptions.

- Question from Tom Palmer (JPMorgan): You previously referenced a ~$115M EBITDA normalized run rate for foodservice—should we expect something higher given recent volume strength?

Response: $115M remains our benchmark for the normalized run rate; we expect it to grow roughly in line with our algo (~5%), approaching ~$120M by year‑end, but want several quarters of normalcy to confirm.

- Question from Matt Smith (Stifel): You had a 20% EBITDA margin in refrigerated retail this quarter partly from AI pricing—can this business sustain high‑teens margins in a normal environment?

Response: High‑teens is reasonable as an annualized expectation, but seasonality will lower margins to around mid‑teens (≈16%) in slower periods.

- Question from Matt Smith (Stifel): Any read‑through on private label trading dynamics across categories—are consumers trading down into private label?

Response: Trade‑down and private label traction are primarily price‑gap dependent and increase with promotional activity.

- Question from Scott Marks (Jefferies): You mentioned targeted investments and innovation for 2026—what types of innovations and categories will you invest in?

Response: We’ll resume brand line extensions across retail categories—e.g., protein and granola in cereal, innovations in refrigerated sides, and a Nutrich relaunch in pet—targeting growth pockets within each category.

- Question from Scott Marks (Jefferies): What gives you confidence that foodservice operator demand for higher value‑add products will sustain?

Response: Longstanding operator migration to higher value‑added products driven by labor/efficiency benefits and some stickiness from conversions (e.g., to liquid eggs) support continued demand.

- Question from Marc Torrente (Wells Fargo Securities): Any changes to assumptions for GO4/Eighth Avenue—what contribution is baked into FY26 and how much did pasta contribute in Q4?

Response: No change: Eighth Avenue expected to contribute ~$45M-$50M in FY26 with confidence in achieving ~$15M of synergies by year‑end; Q4 included about $20M from Eighth Avenue (roughly half pasta), and FY26 assumes two months of pasta contribution.

- Question from Marc Torrente (Wells Fargo Securities): Any color on core grocery volume trends through the quarter and into Q1—are there incremental pressures like SNAP you’ve factored in?

Response: Guidance is conservative: expect Q1/Q2 to resemble recent quarters with marginal category improvement in H2 as we lap prior pressures; not forecasting full reversion to historical trends.

- Question from John Baumgardner (Mizuho Securities): Given headwinds on lower‑income consumers, should Post tilt more toward premium products via M&A or organic innovation?

Response: We view the portfolio as offering choice across price points; strategy is to innovate where consumer demand dictates, including opportunities targeting higher/mid‑income consumers when attractive.

- Question from John Baumgardner (Mizuho Securities): For refrigerated retail side dishes, how will you invest to drive convenience and distribution going forward?

Response: Capacity is now better aligned to serve both branded and selective private label; we’ll pursue attractive private label opportunities while continuing to invest in the brand and play multiple price points selectively.

- Question from Carla Casella (JPMorgan): How active is the M&A market for you today and any plans to refinance revolver draw from Eighth Avenue?

Response: We see some counterparty reluctance at current multiples and thus are selective—M&A is evaluated versus buybacks/debt paydown on risk‑return; we continue to monitor markets for optimal refinancing windows.

Contradiction Point 1

M&A Strategy and Capital Allocation

It involves a shift in the company's stance on M&A as a growth strategy, which could impact investor expectations and financial planning.

How would you describe the current M&A environment, and are there opportunities in your key segments? - Carla Casella(JPMorgan)

2025Q4: We are not solely focused on M&A but consider it as an allocation of capital. Current multiples make some counterparties hesitant. We are continually monitoring the environment and looking for the right opportunities. - Rob Vitale(CEO)

Does compressed valuations increase the likelihood of Post considering a more transformational deal? How do share repurchases impact larger acquisitions? - Andrew Lazar(Barclays)

2025Q1: Yes, we think there will be more activity. We're well positioned for opportunities with our leverage and cash flow profile. Share buybacks don't preclude larger deals. We're open to deals that offer synergies, as we've had in the past. - Jeff Zadoks(COO)

Contradiction Point 2

Supply Chain Flexibility and Stability

It highlights differing perspectives on the stability of the supply chain and production capabilities, which are crucial for operational efficiency and customer satisfaction.

What actions would you consider for cereal if the category remains weak? - Andrew Lazar(Barclays)

2025Q4: We are looking at line optimization opportunities after plant closures. The key is focusing on incremental improvements rather than large-scale actions. - Rob Vitale(CEO)

How has integration work impacted supply chain flexibility in the pet segment? - Andrew Lazar(Barclays)

2025Q1: There are opportunities for further optimization, but our focus is on stabilizing and growing brands like Nutrish. We're insourcing capacity and expect to stabilize products in the next year. - Jeff Zadoks(COO)

Contradiction Point 3

Private Label Performance in Cereal Category

It highlights a change in the company's understanding and explanation of the private label performance in the cereal category, which affects market analysis and strategic decisions.

What actions would you consider for cereal if the category remains weak? - Andrew Lazar(Barclays)

2025Q4: We are looking at line optimization opportunities after plant closures. The key is focusing on incremental improvements rather than large-scale actions. - Rob Vitale(CEO)

Why is private label underperforming branded cereal, and what is Post doing to address it? - Andrew Lazar(Barclays)

2025Q3: It's a mystery, but perhaps promotions affect price gaps. Private label skews to Walmart, which has seen food traffic pull back. - Rob Vitale(CEO)

Contradiction Point 4

Cereal Segment Performance and Strategy

It highlights differing perspectives on the performance and strategic direction of the cereal segment, which is a significant portion of Post Holdings' business.

What actions would you consider for cereal if the category remains weak? - Andrew Lazar(Barclays)

2025Q4: We are looking at line optimization opportunities after plant closures. The key is focusing on incremental improvements rather than large-scale actions. - Rob Vitale(CEO)

Can recent cereal asset optimization help maintain strong profitability despite volume declines in ready-to-eat and pet segments? - Andrew Lazar(Barclays)

2025Q2: The objective is to manage costs and profitability. We expect the category will start to temper to 1% to 2% decline. Asset optimization will help, but we can't predict the exact timing. We'll adapt to volume declines based on category performance. - Jeff Zadoks(CFO)

Contradiction Point 5

M&A Strategy and Cost of Capital

It reflects a shift in the company's strategic approach to capital allocation and M&A, which is crucial for investors and shareholders in understanding the company's growth and financial management strategies.

How do industry volume challenges impact capital allocation decisions? Is M&A still the right approach now? - Andrew Lazar(Barclays)

2025Q4: The cost of capital has changed dramatically. Rather than just focusing on growth through M&A, we are looking at opportunities to improve our portfolio through focus and efficiency. We compare M&A opportunities with share buybacks based on risk and return. Our strategy is to use capital effectively rather than focusing on size alone. - Rob Vitale(CEO)

Have there been any updates on the potential options for the 8th Avenue business and Post's role in it? - Kenneth Goldman(JPMorgan)

2025Q2: You know, we've been very, very thoughtful about whether, and how, we use M&A as part of our capital allocation strategy. The general view, obviously, is M&A growth. But that's not the only way to think about it. There are times, as we've shown, which is core organic growth. There are times we do M&A. We balance it. - Rob Vitale(CEO)

Discover what executives don't want to reveal in conference calls

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet