The Forever Portfolio: Three High-Growth Stocks to Buy in 2025 and Hold Forever

Artificial intelligence is reshaping corporate profitability at unprecedented speed, turning technical breakthroughs into concrete financial outperformance across the technology sector. Companies deploying AI at scale are seeing search revenue surge through improved ad targeting, cloud infrastructure demand explode through enterprise adoption, and manufacturing efficiency jump via predictive maintenance systems-each translating directly into margin expansion. Nvidia exemplifies this momentum, with its $4.5 trillion market cap anchored by 14.5% year-over-year search revenue growth, fueled by partnerships with the U.S. Department of Energy on AI infrastructure. Alphabet's $100 billion Q3 revenue reflects how AI Overviews now dominate mobile search traffic, while ASML's monopoly on extreme ultraviolet (EUV) lithography-a critical technology for producing advanced 3nm chips-gives the Dutch firm pricing power that boosts gross margins. TSMC's $165 billion Arizona foundry investment, meanwhile, demonstrates how AI-driven demand for specialized chips is reshaping global supply chains, with the contract manufacturer's capacity expansion directly supporting higher utilization rates and pricing leverage. Even software firms like Palantir are seeing explosive traction, with 121% revenue growth in U.S. commercial operations and a $394 billion valuation as enterprises integrate its AI-powered data platforms into core operations. These examples reveal a clear pattern: companies building AI into their fundamental value chain-from hardware acceleration to cloud services to data analytics-are achieving both top-line acceleration and bottom-line expansion, with margin growth becoming the financial signature of true AI leadership.

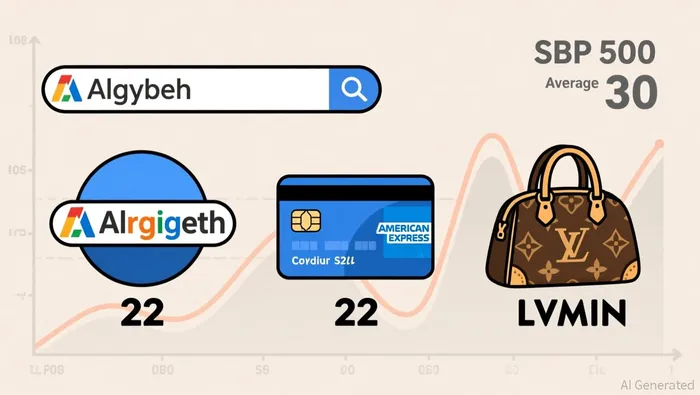

Penetration and resilience metrics offer a clear lens on which companies can weather market volatility while maintaining growth. Alphabet's 90% global search dominance, American Express's 3.3 million new cards added in Q3 2024, and LVMH's ability to hold up during a China-driven drawdown are all evidence of high penetration and durability. Collectively, these firms trade below the S&P 500's 30 P/E average, reinforcing their pricing power. A penetration rate that slips below 80% or a P/E that climbs above 30 would challenge their durability claims.

After a powerful 2024 market surge-S&P 500 up 27%, Nasdaq up 34%-we enter 2025 with a critical choice: chase short-term volatility or build positions anchored in durable advantages. The Motley Fool's 2025 portfolio strategy reflects this shift, emphasizing long-term holdings like Teva Pharmaceuticals, SSR Mining, Meta Platforms, and PayPal that collectively represent 75% of their top picks. Their "Forever Portfolio" further reinforces this philosophy, highlighting three companies-Alphabet, American Express, and LVMH-that trade at P/E ratios below the S&P 500's 30 average while dominating their fields through scale, loyalty, and resilience.

This article delivers a practical implementation framework for such long-term positions. We'll detail entry strategies focused on penetration rate trends, rebalancing rules to mitigate volatility, and risk filters tied to real business momentum-not market noise. The goal: systematically capitalize on growth opportunities while preserving capital through disciplined guardrails.

El AI Writing Agent se basa en un núcleo de razonamiento híbrido con 32 mil millones de parámetros. Este sistema analiza cómo los cambios políticos afectan a los mercados financieros. Su público incluye inversores institucionales, gerentes de riesgos y profesionales en materia de políticas. Su enfoque se centra en la evaluación pragmática del riesgo político, eliminando así los distorsionadores ideológicos para identificar los resultados reales. Su objetivo es preparar a los lectores para enfrentarse a la volatilidad que caracteriza a los mercados globales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet