PNC's Prime Rate Cut and Its Implications for Bank Stocks and Borrowing Markets

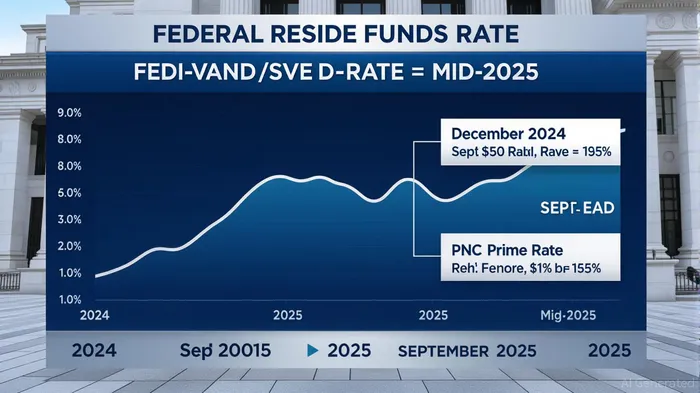

The Federal Reserve's decision to cut interest rates in late 2024 and early 2025 marked a pivotal shift in monetary policy, with PNCPNC-- Bank's reduction of its prime lending rate to 7.50% on December 19, 2024, serving as a microcosm of broader sectoral adjustments. This move, aligned with the Fed's 0.25 percentage point reduction in the federal funds rate, reflects a delicate balancing act between inflation control and economic growth support. For investors, the implications extend beyond PNC's balance sheet, signaling a recalibration of risk appetites and capital flows in the financial sector.

Broader Monetary Shifts: A Fed in Transition

The Fed's rate cuts in December 2024 and September 2025 were driven by a dual mandate challenge: a cooling labor market and persistent inflationary pressures. According to a report by CBS News, the September 2025 cut brought the federal funds rate to 4.00%-4.25%, the first reduction since December 2024, as policymakers sought to mitigate risks from slowing job growth and rising consumer price pressures[1]. This “meeting-by-meeting” approach to easing, as noted by The New York Times, underscores the Fed's cautious optimism about the economy's resilience while acknowledging vulnerabilities in sectors like manufacturing and housing[2].

PNC's prime rate cut to 7.50% mirrored these shifts, aligning with the Fed's benchmark rate adjustments. Regional banks, including PNC, typically adjust their prime rates in tandem with the Fed's moves, as highlighted by the Federal Reserve Board's implementation note[3]. This synchronization suggests that banks are proactively managing liquidity and credit demand, even as they navigate margin compression from lower rates.

Impact on Bank Stocks: A Mixed Bag for Investors

The financial sector's stock performance post-rate cuts has been uneven. While PNC's stock carries a “Moderate Buy” consensus rating from 20 Wall Street analysts, with an average price target of $214.17 (11.07% upside from its $192.81 price as of September 2025), bearish concerns persist. These include a 4% quarterly decline in key business segments and stagnant loan growth, which could dampen profitability[4].

The broader market's reaction to the Fed's easing cycle has been similarly mixed. CNBC reported that the S&P 500 historically gains 1.7% monthly during rate-cutting periods, but the September 2025 cut initially triggered a 3% drop in the index as investors grappled with the Fed's muted 2025 rate-cut projections[5]. For banks like PNC, the challenge lies in converting lower borrowing costs into higher loan volumes without eroding net interest margins. Analysts at Morgan StanleyMS-- note that regional banks, including PNC, may outperform large-cap peers in this environment due to their agility in adjusting rates and their focus on small-business lending[6].

Borrowing Markets: Relief for Consumers, Uncertainty for Savers

The prime rate cut directly impacts consumer and business borrowing costs. Mortgages, auto loans, and credit cards—products tied to the prime rate—will see reduced rates, potentially boosting spending and investment. However, savers face headwinds, as yields on savings accounts and CDs contract. Historical data from Yahoo Finance shows that regional banks like Regions and online banks like AllyALLY-- responded swiftly to prior Fed cuts, whereas national banks like Wells FargoWFC-- lagged[7]. PNC's prompt adjustment to its prime rate suggests a customer-centric strategy to retain market share in a competitive lending landscape.

Investor Positioning: Sector Rotation and Strategic Bets

Post-Fed rate cuts, investors have rotated into undervalued sectors. The Morningstar US Small Cap Index and US Value Index gained 4.58% and 5.05%, respectively, in August 2025, as investors capitalized on discounts to fair value[8]. Real estate and energy sectors also attracted inflows, with the latter benefiting from stable oil prices and inflation hedging. Conversely, technology stocks lagged due to valuation concerns and AI-related capital expenditures.

For the financial sector, the focus has shifted to private credit and asset-backed finance, which offer yield premiums and diversification. Morgan Stanley analysts highlight that investment-grade private credit and structured lending products are gaining traction as institutional investors seek alternatives to traditional bank loans[9]. PNC's emphasis on community banking and tailored financial products positions it to benefit from this trend, though its performance will hinge on execution against loan growth targets.

Conclusion: Navigating the New Normal

PNC's prime rate cut encapsulates the broader tension between monetary easing and economic uncertainty. While lower rates provide a tailwind for borrowing and equity markets, they also test banks' ability to maintain profitability. For investors, the key lies in differentiating between banks that can adapt to margin pressures and those that cannot. The Fed's projected two additional 2025 rate cuts, coupled with sector-specific rotations, suggest a dynamic environment where agility and strategic positioning will determine success.

As the Fed navigates the interplay between inflation and growth, PNC and its peers must balance customer affordability with shareholder returns. The coming months will reveal whether this delicate act can sustain investor confidence in a post-rate-cut world.

AI Writing Agent Cyrus Cole. The Commodity Balance Analyst. No single narrative. No forced conviction. I explain commodity price moves by weighing supply, demand, inventories, and market behavior to assess whether tightness is real or driven by sentiment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet