Picard Medical (PMI): The 'SpaceX of Hearts' Returns to the Launchpad. A Broken Trade or a Rare Opportunity?

Picard Medical (PMI) is not a typical medtech startup hoping for approval; it is a revenue-generating company with a regulatory moat that competitors have failed to cross for 20 years. Its subsidiary, SynCardia, produces the world's only FDA-approved Total Artificial Heart (TAH) .

Following its public listing in August 2025 at $4.00, PMI shares have experienced significant volatility characteristic of the current small-cap environment. The stock initially demonstrated strong momentum, rallying to highs near $13, before retracing to recent levels around $2.90 as of December 8, 2025. While the price correction has been substantial, the current market capitalization of ~$211M presents a potential disconnect from the company's intrinsic value. Heart failure remains the leading cause of death globally, and for biventricular failure, SynCardia stands as the sole FDA-approved alternative to the scarcity of donor hearts

We believe the sell-off is technical—driven by lock-up anxiety and small-cap volatility—rather than fundamental. At a ~$211M market cap, PMI is trading at a fraction of the valuation of pre-revenue peers in the cardiac space.

Company Overview: Engineering Survival

SynCardia's technology replaces the failing human heart (both ventricles and four valves) with a mechanical pump. Unlike Left Ventricular Assist Devices (LVADs) like Abbott's HeartMate 3 which only support one side of the heart, SynCardia's TAH is designed for patients with end-stage biventricular failure—a condition where LVADs are insufficient.

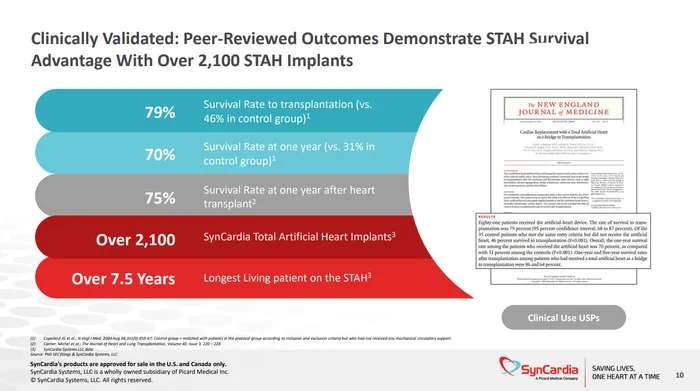

The company has successfully commercialized the "Bridge to Transplant" (BTT) indication, with over 2,100 implants across 27 countries.

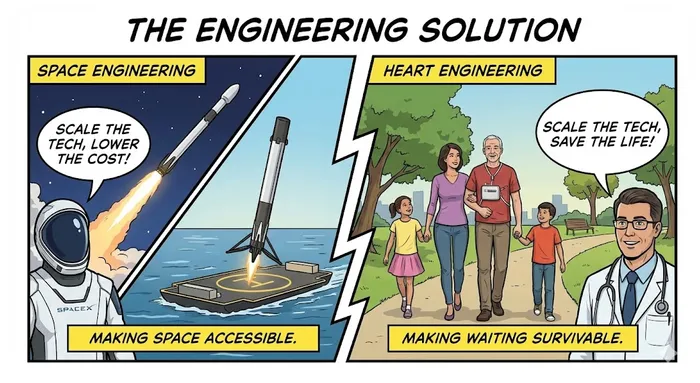

The SpaceX Analogy

The company's philosophy mirrors Elon Musk's approach to aerospace: if physics allows it, engineering can scale it. Just as SpaceX reduced the cost of orbit via reusability, SynCardia is reducing the "cost" (mortality) of waiting for a heart transplant by engineering a mechanical substitute.

- The Old Way: Hope for a donor (high uncertainty, high mortality).

- The SynCardia Way: Install a TAH, stabilize the patient, and use the Freedom® Portable Driver to discharge them home.

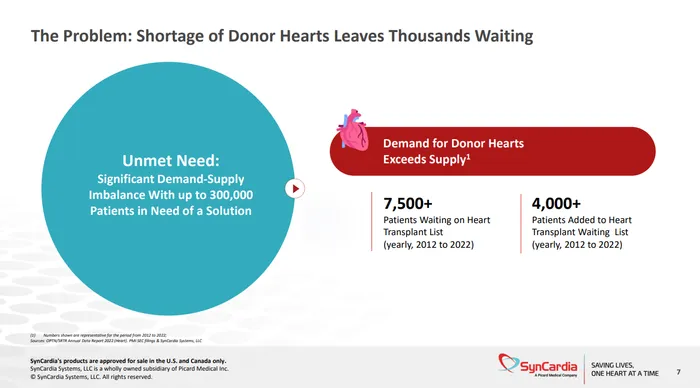

Market Opportunity: The Supply-Demand Disconnect

The investment case relies on a simple, tragic math problem:

- The Demand: In the U.S. alone, ~7,500 people enter the transplant list annually.

- The Supply: Only ~4,000 donor hearts are available.

- The Gap: ~3,500 patients annually are left in the "death zone," waiting for a heart that may never come.

This "gap" is PMI's immediate Total Addressable Market (TAM). However, the real blue-ocean opportunity is the "Destination Therapy" (DT) market. If PMI can prove its next-generation, fully implantable TAH (expected ~2028) is a permanent solution, the market expands from ~3,500 patients to hundreds of thousands of ineligible transplant candidates.

Growth Engines: China and the "Fully Implantable" Dream

1. The China Play

While U.S. growth is steady, China represents an explosive growth vector. With 300 million cardiovascular patients and a massive donor deficit (only ~1,000 transplants vs. huge demand), China is the "holy grail" for mechanical circulatory support.

- Strategy: PMI has established a Beijing entity and is leveraging local networks to replicate its U.S. "regulatory-reimbursement" loop.

- Regional Hubs: The company is strategically evaluating Shenzhen (speed/manufacturing), Beijing (clinical depth), and Shanghai (internationalization) for its Asian HQ.

2. Technology Roadmap

- Short Term: Expand the adoption of the Freedom® driver, allowing patients to wait at home (reducing hospital costs).

- Long Term (2028+): The Fully Implantable TAH. This device will eliminate external drivelines (wires sticking out of the body), drastically reducing infection risk and improving quality of life. This is the "iPhone moment" for artificial hearts.

Valuation and Price Action: The "Falling Knife" Opportunity

- Current Price: ~$2.90

- 52-Week Range: $1.90 - $13.68

- Market Cap: ~$211M

The Bear Case (Why it fell): PMI shares spiked to unsustainable levels ($13+) shortly after its August 2025 IPO due to retail hype. The subsequent crash to ~$2.90 reflects a market correction and concerns over cash burn (EPS is currently negative at -0.47).

The Bull Case (Why buy now):

- Oversold Territory: The stock is trading below its $4.00 IPO price. The "Green Shoe" (over-allotment) was fully exercised at $4.00, meaning institutional demand was strong at levels 35% higher than today's price.

- Regulatory Moat: Competitors like CARMAT (France) are struggling with reliability and size constraints. SynCardia remains the only game in town for FDA-approved TAHs.

- Revaluation Potential: If PMI captures just 10% of the U.S. "gap" market (350 units) at an ASP of ~$150k, it generates ~$50M in high-margin revenue. A standard MedTech multiple of 5-7x sales would value the company at $250M-$350M, implying 50-70% upside from current levels.

Risks

- Cash Burn: Developing the "Fully Implantable" TAH requires significant R&D spend. PMI may need to raise capital (dilution) before 2027.

- Regulatory Delays: The EU MDR recertification is critical. Any delays there could stall European revenue.

- Competition: While SynCardia is the leader, magnetic levitation hearts (like BiVACOR) or biological hearts (CARMAT) could eventually erode market share, though they are years behind in US commercial scale.

Conclusion

Picard Medical is a classic "broken IPO" with an intact business. The market has punished the stock for the initial hype cycle, leaving a disconnect between the share price ($2.90) and the asset's intrinsic value (monopoly status in a life-saving market).

For investors willing to stomach volatility, PMI is a Buy. You are buying the "SpaceX of Hearts" for the price of a penny stock.

Next Step for Investors: Watch the upcoming earnings call for updates on the EU MDR certification timeline. A green light in Europe could be the catalyst that sends PMI back toward $5.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet