Petratherm's Financial Sustainability: A Deep Dive into Cash Burn and Operational Efficiency

Petratherm (ASX:PTR) has long been a speculative play for investors betting on its geothermal energy ambitions, but the question of financial sustainability looms large. , the company's ability to fund operations without external capital raises red flags. Let's dissect the numbers to determine whether PTR's cash burn rate and operational efficiency justify its valuation—or if it's a cautionary tale in the making.

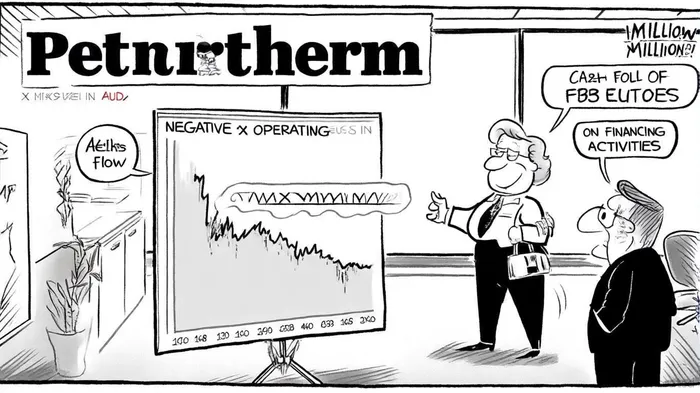

The Cash Burn Conundrum

Petratherm's cash burn rate remains a critical concern. For the 12 months ending September 2024, , . , . This suggests that despite trimming some investment costs, PTR still struggles to generate positive cash from its core operations.

The company's reliance on financing activities to stay afloat is stark. In Q3 2025, , . However, this lifeline appears temporary. , Petratherm's ability to secure further funding without diluting shareholders or incurring debt is uncertain. At this burn rate, .

Operational Efficiency: A Missed Target

Operational efficiency is another area of concern. , indicating a disconnect between valuation and earnings [2]. The company's negative return on equity and lack of dividends further underscore its inability to generate returns for shareholders. While geothermal projects often require upfront capital, the absence of scalable revenue streams raises questions about whether PTR's operational model is viable in the long term.

Capital expenditures, though reduced in Q3 2025, remain a drag on liquidity. The AUD 409,057 spent on investments in Q3 2025 [3] suggests continued commitment to growth, but without a clear path to profitability, these outlays risk becoming a bottomless pit. For context, .

The Verdict: A High-Risk, High-Reward Proposition

Petratherm's financial sustainability hinges on its ability to reverse its cash burn trajectory and demonstrate operational efficiency. While the Q3 2025 cash flow report hints at tighter control over capital spending [3], the company remains dependent on external financing to fund operations. For now, PTR is a stock for the most aggressive investors—those willing to tolerate extreme volatility for the chance of a breakthrough in geothermal energy.

However, the risks are clear. If Petratherm fails to achieve positive operating cash flow or secure additional funding, . Until then, this is a stock to watch closely, not own blindly.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet