Peraso's Q3 2025 Earnings Call: Contradictions Emerge on Military Revenue, Inventory Management, and OEM Market Penetration

Date of Call: November 10, 2025

Financials Results

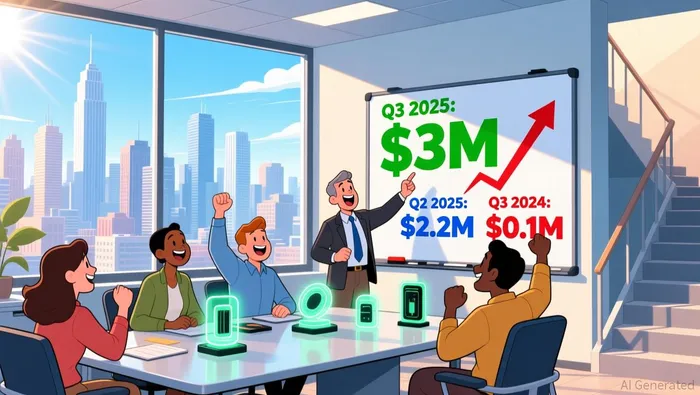

- Revenue: $3.2M in Q3 2025, up >45% sequentially from $2.2M in Q2 2025, down from $3.8M in Q3 2024; mmWave revenue $3.0M vs $2.2M prior quarter and $0.1M year-ago

- EPS: Loss impact of $0.15 per share in Q3 2025 from change in fair value of warrant liabilities; prior-quarter non-GAAP net loss was $0.28 loss per share and year-ago was $0.34 loss per share

- Gross Margin: 56.2% GAAP in Q3 2025, up from 48.3% sequentially and vs 47% in Q3 2024 (non-GAAP also 56.2% vs 48.3% prior quarter and 61.7% year-ago)

Guidance:

- Q4 2025 revenue expected to be $2.8M to $3.1M based on current backlog.

- Expect continued year-over-year growth from mmWave products in Q4 and into 2026.

- Short-term gross margin target around ~50% (high-40s to mid-50s); Q4 expected mid-50s aided by high-margin memory shipments.

- Preproduction customers typically convert to production in ~1 quarter; fixed wireless engagements ~9–12 months; new markets/military ~12–15 months.

- Tactical-defense customer production anticipated in H2 2026 (roughly a 5–6 quarter lag).

Business Commentary:

* Strong Revenue Growth in mmWave Products: - Peraso reported record mmWave product

* Strong Revenue Growth in mmWave Products: - Peraso reported record mmWave product revenues of $3 million in Q3 2025, up from $2.2 million in the prior quarter and $0.1 million in the same quarter a year ago. - The growth was driven by increased market awareness of 60 gigahertz technology, broad adoption by fixed wireless access providers, and expanding opportunities in new markets like tactical communications.- Improved Gross Margin and Operating Efficiency:

- Consolidated GAAP gross margin increased to

56.2%in Q3 from48.3%in the prior quarter and47%in the year ago quarter. The increase was primarily due to a favorable revenue mix of mmWave products and reduced stock-based compensation expense.

Increased Funnel Opportunities and Production Orders:

- Peraso's engagement pipeline shows a greater than

30funnel opportunity, with nearly doubling the number of customer SKUs in production over the last 2 years. This growth is attributed to successful customer engagements, new strategic partnerships, and the versatility of Peraso's mmWave technology in various applications.

Tactical Communications Market Expansion:

- Peraso is expanding its reach into the tactical communications market, with notable collaborations and initial field trials with defense contractors.

This growth is driven by the unique attributes of 60 gigahertz wireless technology, which provides high data rates, low latency, and power efficiency, ideal for military applications.

Strategic Review and Capitalization:

- Peraso has approximately

$1.9 millionin cash as of September 30, 2025, with recent proceeds from warrant and at-market offerings. - The company is conducting a strategic review, considering various financing transactions and strategic alternatives to improve its financial position.

Sentiment Analysis:

Overall Tone: Positive

- Management: "notably strong third quarter" with "total revenue increased more than 45% sequentially" and "gross margin increased... achieving our targeted gross margin level in the mid-50% range." CEO: "we had a great third quarter" and highlighted record mmWave revenue and reduced cash burn, supporting a positive tone.

Q&A:

- Question from David Williams (N/A): Can you give more color on the new OEM you announced and what that opportunity looks like?

Response: OEM is confidential but represents a performance win where Peraso displaced competitors, serving as validation and likely driving more OEM conversions.

- Question from David Williams (N/A): Does that new OEM/order specifically signal anything about demand in fixed wireless access?

Response: Management: It's broadly positive—another validation of mmWave technology, particularly effective for MDUs, supporting fixed wireless demand.

- Question from David Williams (N/A): Any sense of customer design cycles now that inventory correction is ending—are customers coming to market more quickly?

Response: Management: It varies—fixed wireless ~9–12 months to mass production; new markets/military ~12–15 months.

- Question from David Williams (N/A): AR and inventory rose sequentially—any color and how should we think about working capital going forward?

Response: Jim: AR was timing-related (70%+ collected); inventory builds are deliberate to meet anticipated Q1/Q2 demand and will be tightly managed to backlog.

- Question from David Williams (N/A): How should we think about gross margin moving forward given mix and prior write-down recoveries?

Response: Jim: Targeting around 50% (high-40s to mid-50s); Q3 was elevated by mix and reserve sales; Q4 should be mid-50s with memory benefit.

- Question from Kevin Liu (K. Liu & Company): For customers in preproduction, how long before they contribute meaningfully to growth?

Response: Management: Preproduction typically indicates about one quarter (≈3 months) to meaningful production.

- Question from Kevin Liu (K. Liu & Company): For the lead tactical defense customer, how long will trials last before meaningful long-term revenue?

Response: Management: Trials are ongoing (including around Christmas); expect real production in H2 2026—about a 5–6 quarter lag from engagement.

- Question from Kevin Liu (K. Liu & Company): Can you describe the NRE pipeline and how much customization is needed for adjacent-market opportunities?

Response: Management: Two buckets—existing chips needing modest NRE (fast) and custom silicon requiring longer development; silicon spins pursued only for sizable opportunities.

- Question from Kevin Liu (K. Liu & Company): How much memory revenue remains in Q4 and will that raise gross margin sequentially?

Response: Jim: Approximately $375k of memory shipments remain in Q4; it's high-margin and should lift Q4 gross margin to mid-50s.

Contradiction Point 1

Military and Defense Engagement and Revenue Contribution

It directly impacts expectations regarding new revenue streams, market penetration, and the timeline for revenue contributions from the military sector, which are crucial for strategic planning and investor expectations.

What are inventory trends and have you resolved overstock issues? - David Neil Williams(The Benchmark Company, LLC, Research Division)

20251111-2025 Q3: Fixed wireless typically takes 9-12 months, military is 12-15 months, and new markets like edge AI can also take about 12-15 months. Trial results are expected in the second half of 2026, with production following. - Ronald Glibbery(CEO)

Are there opportunities to boost near-term revenue via defense contracts or government contracts? - David Neil Williams(The Benchmark Company, LLC, Research Division)

2025Q2: We have 10-plus engagements in the military, and we've secured our first NREs. We expect significant contributions over the next 1.5 to 2 years. - Ronald Glibbery(CEO)

Contradiction Point 2

Inventory and Cash Flow Management

It involves changes in inventory management and cash flow expectations, which are critical for operational efficiency and financial stability.

Can you speak to the increase in AR and inventory on the balance sheet? - David Williams(fund)

20251111-2025 Q3: AR increase is due to timing of sales, and 70% has been collected. Inventory has been depleted and built back up for anticipated demand in Q1 and Q2. Tightly managing working capital, building based on orders. - James Sullivan(CFO)

How is inventory trending, and have you resolved most of the inventory overhang? - David Neil Williams(The Benchmark Company, LLC, Research Division)

2025Q2: We are seeing a significant reduction in inventory levels, primarily due to orders from major customers. Most inventory is spoken for, and we have started replenishing certain products. We expect continued improvement in inventory management, supporting better cash flow. - James W. Sullivan(CFO)

Contradiction Point 3

OEM Customer Engagement and Market Opportunities

It highlights differences in the perceived timeline and impact of a significant OEM customer engaging with Peraso, which could affect revenue expectations and strategic direction.

Can you provide details about the new OEM you announced? What is the potential of this opportunity? - David Williams (fund)

20251111-2025 Q3: It's the #2 OEM in the space and sensitive to confidentiality. It's a validation of our performance as they historically used other competitors. Inventory correction is ending, and OEMs are now choosing Peraso over competitors due to better performance. - Ronald Glibbery(CEO)

Can you discuss the visibility from previously announced deals and any exciting developments expected to contribute further to that visibility throughout the year? - Kevin Liu (K. Liu & Company)

2025Q1: We have backlog with much better visibility than in the past. Key customers in South Africa and defense applications are expected to contribute to Q2 growth. The Ubiquiti purchase order will continue until the end of the year. - James Sullivan(CFO)

Contradiction Point 4

OEM Validation and Market Penetration

It reflects differing perspectives on the significance and impact of OEM partnerships and market penetration, which could influence investor confidence in Peraso's growth strategy.

Does the OEM opportunity relate to fixed wireless access? - David Williams (fund)

20251111-2025 Q3: It's positive, as Starry is an advocate of mmWave technology and uses it for multiple dwelling units, which is turning out to be a nice application for the technology. - Ronald Glibbery(CEO)

Does the new order from an established equipment supplier to fixed wireless service providers indicate a positive or negative signal? - David Williams(The Benchmark Company, LLC, Research Division)

2025Q3: It's a positive validation of mmWave technology. It showcases Peraso's ability to penetrate the market and attract new customers, including those who may not have previously considered their technology. - Ronald Glibbery(CEO)

Contradiction Point 5

Fixed Wireless Access Applications and Market Potential

It involves differing views on the adoption and potential impact of fixed wireless access applications, which is crucial for strategic planning and revenue projections.

Does the OEM opportunity specifically address anything related to fixed wireless access from the company's perspective? - David Williams (fund)

20251111-2025 Q3: It's positive, as Starry is an advocate of mmWave technology and uses it for multiple dwelling units, which is turning out to be a nice application for the technology. - Ronald Glibbery(CEO)

Are you seeing new growth opportunities from BEAD and RDOF funding related to fixed wireless access technology, and are customers shifting interest from fiber or other technologies to FWA? - David Williams (The Benchmark Company, LLC)

2025Q1: We expect BEAD to have a positive impact in the second half of the year. Although direct benefits are not yet visible, we anticipate increased interest in fixed wireless access as an alternative to fiber. - Ronald Glibbery(CEO)

Discover what executives don't want to reveal in conference calls

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet