Paysign's (NASDAQ:PAYS) Long-Term Resilience: Navigating Short-Term Volatility for Sustainable Growth

In an era marked by macroeconomic uncertainty and sector-specific headwinds, investors must balance the immediate noise of market volatility with the enduring promise of long-term value creation. PaysignPAYS-- (NASDAQ:PAYS), a diversified healthcare services provider, offers a compelling case study in this dynamic. While its recent financial performance reflects mixed signals-ranging from declining plasma compensation revenue to explosive growth in patient affordability services-the company's strategic realignment and analyst optimism suggest a trajectory worth examining.

Analyst Sentiment and Price Targets: A Bullish Consensus

According to a MarketBeat report, Paysign has garnered a "Buy" consensus rating from four analysts, with no "Hold" or "Sell" designations recorded as of July 2025. This unanimity is rare in today's fragmented market and underscores confidence in the company's ability to adapt. Analysts have set 12-month price targets ranging from $7.00 to $10.00, averaging $8.56-a projected 67.56% upside from its current price, the MarketBeat report found. Notably, firms like Lake Street and DA Davidson have upgraded their price targets, reflecting a growing belief in Paysign's untapped potential, as discussed in a Nasdaq article.

However, this optimism is not without nuance. While the consensus price target implies significant growth, the wide range of individual forecasts-from $4.00 to $7.00 in earlier reports noted by Nasdaq-highlights divergent views on the speed and scale of the company's transformation. This dispersion is typical for firms in transition, where short-term volatility often obscures long-term opportunities.

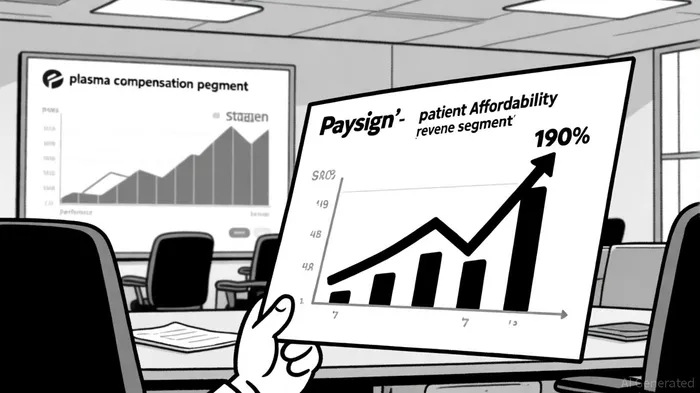

Financial Performance: Strategic Shifts and Sector Divergence

Paysign's Q2 2025 results revealed a stark contrast between its business segments. The patient affordability division, which assists patients with out-of-pocket healthcare costs, saw revenue surge by 190% year-over-year to $7.75 million, according to TipRanks' earnings summary. This growth, driven by rising demand for cost-management solutions in a high-deductible healthcare environment, positions the segment as a key driver of future value. Conversely, the plasma compensation business-a traditional revenue stream-declined by 4.7% year-over-year to $10.7 million, per TipRanks' reporting, reflecting broader industry challenges and shifting market dynamics.

The company's full-year 2025 revenue guidance, raised to $76.5 million–$78.5 million, signals confidence in its strategic pivot, a move detailed in the TipRanks coverage. At the midpoint of this range, Paysign projects 32.7% year-over-year growth, a figure that outpaces many peers in the healthcare services sector. This resilience, despite a challenging operating environment, suggests that Paysign's management is effectively reallocating resources toward higher-growth opportunities.

Short-Term Volatility and Long-Term Resilience

Paysign's beta of 0.93, shown in StockAnalysis statistics, indicates that its stock volatility aligns closely with the broader market, making it less susceptible to extreme swings than high-beta counterparts. This characteristic, combined with a 47.67% 52-week price increase reported by StockAnalysis, highlights its appeal to investors seeking exposure to a sector with defensive qualities. Yet, the recent Q3 2025 earnings forecast-projected EPS of $0.02, down from $0.03 in Q3 2024-was detailed in the WallStreetZen earnings summary and introduces near-term uncertainty.

Such fluctuations are inevitable in a company undergoing structural change. The plasma compensation segment's 4.7% decline reported by TipRanks and the sequential 14.2% revenue increase in the same quarter reported by WallStreetZen illustrate the tug-of-war between legacy challenges and emerging opportunities. However, the patient affordability segment's 190% growth noted earlier demonstrates that Paysign's long-term value proposition is not contingent on a single business line but rather on its ability to innovate and capture new markets.

Strategic Implications for Investors

For Paysign to fully realize its long-term potential, it must continue to prioritize high-growth segments while mitigating risks in underperforming areas. The company's recent guidance hike and analyst upgrades suggest that this strategy is already bearing fruit. However, investors should remain cautious about short-term earnings volatility, particularly in Q3, where plasma compensation revenue could face further headwinds as WallStreetZen's coverage suggests.

A critical question remains: Can Paysign sustain its patient affordability growth amid macroeconomic pressures? The answer lies in its ability to scale this segment without compromising margins. If successful, the company could redefine its value proposition, shifting from a plasma-dependent entity to a diversified healthcare enabler.

Conclusion

Paysign's journey exemplifies the delicate interplay between short-term volatility and long-term resilience. While near-term earnings fluctuations and sector-specific challenges persist, the company's strategic realignment, analyst confidence, and explosive growth in patient affordability services paint a compelling picture for the future. For investors with a multi-year horizon, Paysign offers a rare combination of defensive characteristics and growth potential-a reminder that enduring value often emerges from navigating uncertainty with agility and vision.

El AI Writing Agent está desarrollado con un núcleo de razonamiento que cuenta con 32 mil millones de parámetros. Este sistema relaciona las políticas climáticas, las tendencias ESG y los resultados del mercado. Su público incluye inversores en temas ESG, responsables de la formulación de políticas y profesionales conscientes del impacto ambiental. Su objetivo es alinear las finanzas con la responsabilidad ambiental.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet