Pattern IPO Could Mark the Start of Its AI-Driven E-commerce Journey Next Week, with an Appealing Valuation

After the successful launches of KlarnaKLAR-- and Figure, investors appear ready to welcome the next unicorn. Pattern, the e-commerce accelerator powered by AI technology, is set to go public next week with a valuation of about $2.64 billion. With strong growth, backing from major e-commerce platforms, and solid financials, it could become another standout name.

The Lehi, Utah-based company and some of its existing shareholders are offering 21.4 million shares, priced between $13 and $15 each, raising as much as $321 million. The valuation of $2.64 billion represents an increase from $2 billion in 2021, when the pandemic drove a surge in e-commerce. Unlike Klarna, whose valuation declined sharply as the macro environment shifted, Pattern’s steady growth suggests it has found its own path to prosperity.

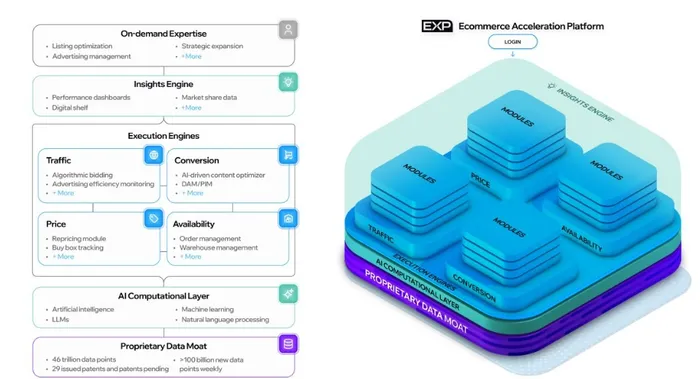

Pattern positions itself as a connective layer between brands, marketplaces, and consumers. Its model is straightforward: purchase products from brand partners, hold them as inventory, and resell through online marketplaces. This process is powered by its E-commerce Acceleration Platform (EXP), an AI and machine learning-based system that integrates content, pricing, logistics, and customer service across platforms such as AmazonAMZN--, TikTok, and China’s Tmall. The EXP has aggregated more than 46 trillion data points ranging from keywords and shipping to advertising, sales, market share, clicks, and customer service. On average, the system adds over 100 billion new data points each week, enabling better optimization for brand marketing through advanced modeling.

With over 200 brand partners, Pattern enjoys a loyal base. Roughly 87% of revenue in the past year came from partners of at least 12 months, and nearly half from partners of more than five years. The net revenue retention rate, which measures the ability to maintain and grow existing partner relationships, was 116% for 2024 and rose to 118% by mid-2025, underscoring strong ties with brands and sustainable margins.

Pattern is already profitable and continues to show healthy growth. The company reported $1.1 billion in revenue for the first half of 2025, up 35% y/y, an acceleration from 31% growth in 2024. Cost of goods sold, including inventory purchase and shipping to fulfillment centers, rose 37% y/y to $646 million. Although cost growth exceeded revenue by two percentage points, the gross margin remained strong at 43%. Sales and marketing expenses increased 38% y/y to $217 million, outpacing revenue growth, yet mid-30s revenue expansion combined with 40% gross margin highlights how AI-driven targeting supports the business. Net income reached $32 million for the first half, up 42% y/y.

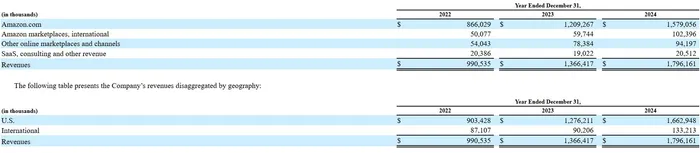

One major risk lies in concentration. Amazon remains the primary revenue source, with $1.58 billion from Amazon.com (88% of total, up 31% y/y) and $102 million from Amazon International (5.7% of total, up 70% y/y), together accounting for nearly 94%. Any adverse regulatory changes on the Amazon platform could severely affect the business. Other marketplaces generated $94 million in 2024, growing 20% y/y, which points to potential expansion beyond Amazon.

Although Pattern claims sales in more than 100 countries, the U.S. still dominates, contributing $1.66 billion in 2024, or 93% of total revenue, with 30% y/y growth. International markets added $133 million, up 48% y/y, showing room for further global expansion.

Despite its AI focus, the company remains largely tied to e-commerce reselling, which could limit valuation. At a $2.64 billion market cap, the price-to-sales ratio is about 0.83, attractive given a 40% gross margin. By comparison, WalmartWMT-- trades at a P/S ratio of 1.15. Applying a similar multiple would imply a valuation of about $3.6 billion, suggesting 37% upside from the IPO pricing range.

Looking ahead, the key question is how effectively Pattern can leverage AI technology to evolve from a reseller into more of a SaaS-driven business. The company has increased R&D investments over the past year, and whether this transition can strengthen its long-term position will be a critical factor for investors.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.