Passage Bio's Reverse Split: A Desperate Move or a Clever Play?

The biotech sector is no stranger to high-stakes gambles, but today's topic—Passage Bio's 1-for-20 reverse stock split—is a reminder that even companies with promising pipelines face brutal market realities. Let's dive into whether this move was a necessary lifeline or a red flag for investors.

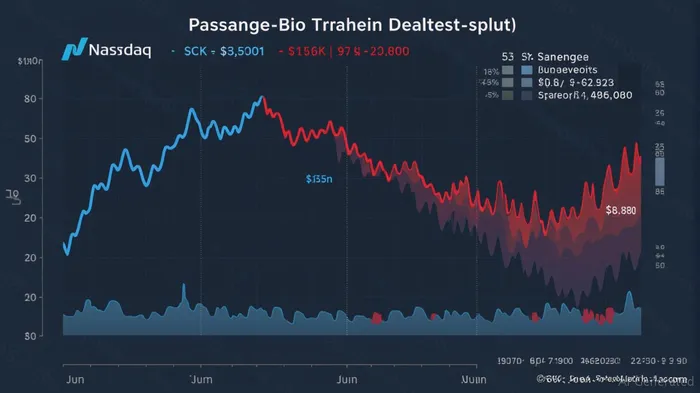

First, the facts: Passage BioPASG-- (PASG) announced the reverse split on July 10, 2025, effective July 14. The move slashed its outstanding shares from ~62.4 million to ~3.12 million, instantly boosting its stock price from $0.44 to around $8.80 (pre-split). The goal? To avoid Nasdaq delisting by meeting the $1 minimum bid price requirement. But here's the catch: this isn't a growth play—it's a survival play.

Let's start with the why. Biotech stocks are volatile, but a 46% drop YTD to $0.44? That's a freefall. The reverse split buys Passage time, but it doesn't fix the core issues: cash burn, clinical risks, and investor skepticism. Let's break it down.

The Strategic Necessity: Avoiding Delisting

A reverse split is a last-resort tactic. Companies do it to survive, not to thrive. For Passage, the math was simple: without this move, NASDAQ would have kicked them off the exchange, crippling their ability to raise capital. The split's 20-to-1 ratio was aggressive, but necessary to catapult the stock above $1.

However, this isn't a get-out-of-jail-free card. The company's market cap remains tiny—just $27.4 million post-split—making it vulnerable to volatility. Plus, the move doesn't address its cash burn or the risks tied to its lead drug candidate, PBFT02.

Market Implications: A Short-Term Win, Long-Term Hurdles

The immediate upside? The stock price jump might attract short-term traders or retail investors lured by a “cheap” entry point. But here's the problem: Passage's pipeline hinges on PBFT02, a gene therapy for frontotemporal dementia. While interim data shows promise—sustained progranulin levels in higher-dose patients—the trial had serious side effects, with three out of eight patients facing adverse events.

The company plans to amend the trial protocol (e.g., adding prophylactic anticoagulation) and seek regulatory feedback for a registrational trial by early 2026. That's a big “if.” If PBFT02 falters, so does Passage's entire value proposition.

The Red Flags: Cash Burn and Insider Selling

While Passage claims a “strong liquidity position” with a current ratio of 3.74, its cash burn rate is a silent killer. Biotechs861042-- often have ample cash on paper, but if trials stall or fail, that cash evaporates quickly.

Worse, insiders have been selling. Orbimed Advisors LLC and CFO Kathleen Borthwick unloaded shares, with 13 sales in six months and zero buys. That's a huge red flag. Even if the stock bounces post-split, institutional holders are voting with their wallets—and they're exiting.

The Bottom Line: High Risk, High Reward

So, is this a buy? Let's weigh the odds:

Pros:

- The reverse split averts delisting, giving Passage breathing room.

- PBFT02's interim data hints at potential in a rare disease space.

- Analysts still rate it “Buy,” though that could be a “penny stock” call.

Cons:

- The tiny market cap and high volatility make it a roller-coaster ride.

- Clinical trial risks are real—safety issues could sink the stock again.

- Insiders are selling, and the cash position might not last long.

My Call: Proceed With Extreme Caution

This is not a “set it and forget it” stock. Passage Bio is a high-risk, high-reward play. If PBFT02 gets FDA approval and proves safe, the stock could soar. But if trials stumble—or if the company runs out of cash—it's a disaster.

Action Plan:

- Only invest what you can afford to lose.

- Watch the PBFT02 trial updates closely—safety data is the next big test.

- Monitor cash burn: If Passage starts burning through its $27.4M market cap, run.

In short, Passage Bio's reverse split is a lifeline, not a cure. This stock is for aggressive investors willing to gamble on a single drug's success. For the rest of us? Maybe sit this one out—unless you've got a crystal ball for clinical trials.

Disclaimer: This article is for informational purposes only. Consult your financial advisor before making investment decisions.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet