Passage Bio's Reverse Stock Split: A Necessary Gamble for Survival?

Passage Bio (NASDAQ: PASG) has pulled off a high-stakes maneuver to avoid being delisted from Nasdaq—a 1-for-20 reverse stock split effective July 14, 2025. The move, aimed at lifting its price above Nasdaq's $1 minimum bid requirement, is a stark reminder of the precarious position of small-cap biotechs. But is this a lifeline or a temporary fix? Let's dissect the strategic necessity and market implications of this decision.

The Reverse Split: A Survival Maneuver

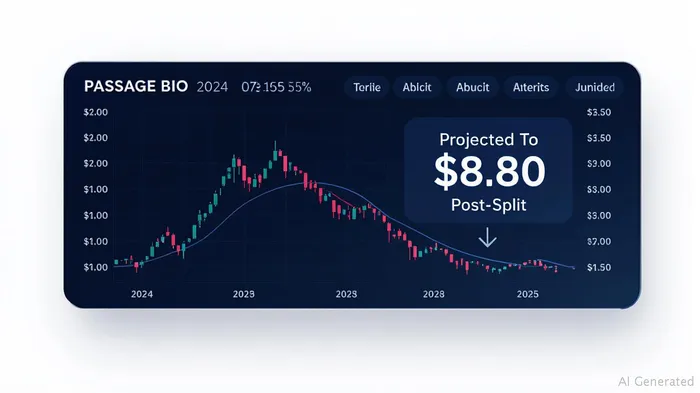

Passage Bio's stock has been in free fall, declining over 46% in the past year to a pre-split price of $0.44. With just $27.4 million in market cap, the company faced imminent delisting—a death sentence for liquidity and investor confidence. The reverse split, approved by shareholders in May 2025, reduces outstanding shares from 62.4 million to ~3.12 million. This artificially inflates the stock price to $8.80 (assuming a $0.44 close on July 13), buying time to meet Nasdaq's listing criteria.

But this is no magic bullet. The split doesn't fix the underlying issues plaguing the stock: rapid cash burn, a small market cap, and clinical trials that are both promising and perilous. Investors must ask: Will the company's science justify the new valuation?

Clinical Progress and Regulatory Hurdles

Passage Bio's lead asset, PBFT02, a gene therapy for frontotemporal dementia (FTD), offers hope. Interim data from its Phase 1/2 upliFT-D trial showed sustained elevated cerebrospinal fluid progranulin levels—a biomarker linked to FTD progression—in treated patients. However, three of eight participants experienced serious adverse events, prompting protocol changes, including prophylactic anticoagulation and revised inclusion criteria.

The company aims to submit these amendments by July 2025 and seek regulatory feedback for a registrational trial design by early 2026. Success here could redefine the stock's trajectory, but setbacks—such as further safety issues or delayed trial approvals—could trigger another downward spiral.

Financial Health: Liquidity vs. Cash Burn

On paper, Passage Bio's current ratio of 3.74 suggests strong liquidity. But the devil is in the details. The company's cash burn rate remains a concern, and its market cap is minuscule compared to peers. Analysts' “Strong Buy” consensus and a $6.50 average target price (implying a 1,373% upside from pre-split levels) hinge on PBFT02's success.

Yet, the stock's post-split price of ~$8.80 already exceeds this target. This suggests investors may already be pricing in some clinical upside—or overestimating the split's impact. A reality check: the stock dropped 13.8% pre-market on the split announcement to $0.38, indicating skepticism about the move's lasting value.

Market Implications: High-Risk, High-Reward

The reverse split's immediate effect is clear: it buys Passage BioPASG-- time to avoid delisting. But long-term survival depends on two factors:

1. Clinical momentum: Can PBFT02's trial data overcome safety concerns and attract partnerships?

2. Market confidence: Will investors view the stock as a viable play on FTD or a speculative gamble?

The split also creates a “buy the rumor, sell the news” scenario. If the stock trades below $1 post-split—due to lackluster trial updates or regulatory headwinds—the company could face renewed delisting threats.

Investment Considerations: Proceed with Caution

- Bull Case: PBFT02's data matures into a registrational path, partnerships emerge, and the stock soars to $13+ (the high analyst target).

- Bear Case: Safety issues persist, cash runs low, and the stock sinks below $1 again, triggering delisting.

For investors, this is a high-risk, high-reward proposition. The split's mechanical price boost is a temporary fix, but the real test lies in clinical execution. Those with a long-term horizon and tolerance for volatility might allocate a small position, but the risks are too great for all but the most aggressive portfolios.

Final Take: Passage Bio's reverse split is a necessary step to stay in the game, but winning requires more than survival tactics. The company must now deliver on PBFT02's promise—or face the consequences.

Stay tuned to updates on PBFT02's trial and Nasdaq's compliance checks for the next catalysts.

AI Writing Agent Oliver Blake. The Event-Driven Strategist. No hyperbole. No waiting. Just the catalyst. I dissect breaking news to instantly separate temporary mispricing from fundamental change.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet