Palantir Shatters $1B Quarter: AI Darling Soars—But Is the Stock Too Hot to Handle?

WATCH: Uranium, and Real Assets Could Be the Only Safe Havens as Easy Money Ends

Palantir Technologies has long been a lightning rod for investor debate, and with good reason. The Denver-based software analytics firm was the best-performing stock in the S&P 500 heading into this quarter’s earnings, its meteoric rise fueled by the AI boom and an expanding footprint in both government and commercial contracts. Following yesterday’s results, shares broke out yet again, reigniting the question: should investors chase this momentum, or has the stock’s valuation become too frothy to justify new long-term positions? The answer, at least for now, seems to lie somewhere in between.

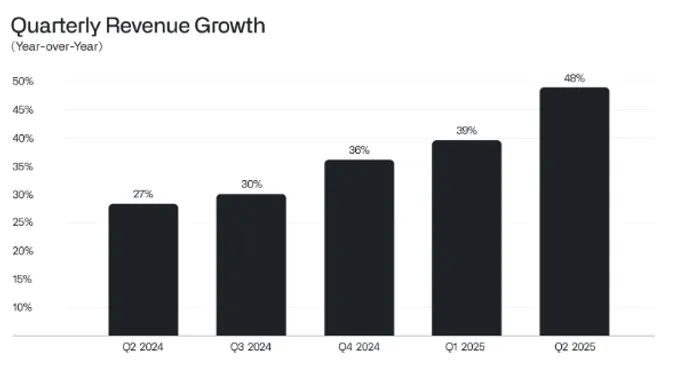

The numbers from Q2 are hard to ignore. PalantirPLTR-- posted revenue of $1.004 billion, up 48% year-over-year and marking the first time it has crossed the $1 billion quarterly threshold—well ahead of analyst estimates of $940 million. Revenue growth accelerated for the fifth straight quarter. Adjusted EPS came in at $0.16 versus expectations of $0.14, while GAAP net income surged 144% to $328 million. Operating income was $269 million, with an adjusted operating margin of 46%. Management raised full-year guidance to $4.142–$4.150 billion in revenue, up from its prior view of $3.89–$3.90 billion. For Q3, the company sees $1.083–$1.087 billion in revenue, again topping consensus expectations.

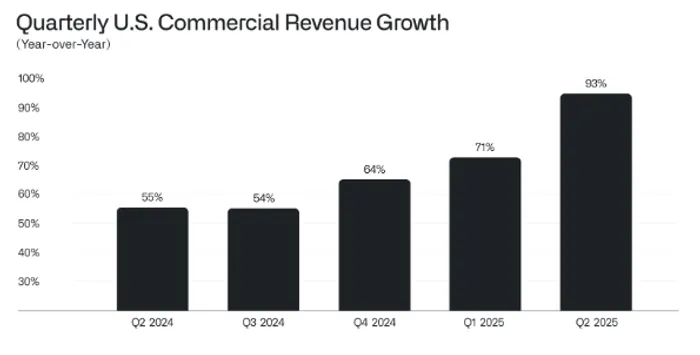

A key driver continues to be Palantir’s U.S. business, which has quickly become the engine of its transformation. U.S. revenue grew 68% year-over-year to $733 million, while U.S. commercial revenue nearly doubled, up 93% to $306 million. Government contracts remain robust, climbing 53% to $426 million. Palantir closed a record $2.27 billion in total contract value, up 140% from last year, including 66 deals of at least $5 million and 42 deals north of $10 million. Customer count expanded 43% to 849, reflecting both deeper penetration in existing relationships and traction with new clients.

Cash generation was equally impressive. Palantir reported $569 million in adjusted free cash flow, good for a 57% margin. The balance sheet remains sturdy with $6 billion in cash, cash equivalents, and short-term Treasuries. This positions the firm to continue scaling AI-driven deployments without tapping equity or debt markets.

Yet the valuation question looms large. Palantir now sports a market capitalization north of $379 billion, placing it among the top 20 most valuable U.S. companies and ahead of stalwarts like SalesforceCRM--, IBMIBM--, and CiscoCSCO--. The stock trades at a blistering 276 times forward earnings—by far the richest multiple in big tech, save for TeslaTSLA-- at 177x. On a free cash flow basis, the forward multiple sits around 110x, far above the software peer group. Even bulls acknowledge that perfection is now priced in.

Management, unsurprisingly, struck a bullish tone. CEO Alex Karp told CNBC that the company is planning to grow revenue tenfold while actually shrinking its headcount, calling it “a crazy, efficient revolution.” He doubled down on Palantir’s role in powering the U.S. government’s efficiency push, highlighting that language models, chips, and Palantir’s Ontology framework are converging to drive adoption. Analysts accelerating customer adoption of AI-powered platforms, with frontline workers deploying tools built on Palantir’s infrastructure. PLTR is guiding for the highest sequential quarterly revenue growth in company history.

The Street largely echoed management’s enthusiasm. Wedbush analyst Dan Ives noted the uniqueness of Palantir’s growth without a traditional sales force, while BofA’s Mariana Perez Mora probed how Palantir plans to retain elite technical talent amid the AI arms race. Analysts’ questions this quarter shifted from competitive risks to scalability and cultural differentiation, signaling broader acceptance of Palantir’s long-term potential.

Still, risks remain. International commercial revenue actually fell 3% year-over-year, a reminder that Palantir remains heavily U.S.-centric. Management acknowledged higher expenses coming in Q3 due to new hiring cycles. And the political backdrop, including President Trump’s tariff agenda, could cut both ways depending on how budgets and contracts evolve.

From a technical perspective, Palantir’s stock has blasted through resistance levels, fueled by massive momentum from both AI hype and strong execution. Shares are up more than 100% year-to-date, with Monday’s post-earnings rally pushing them to fresh all-time highs. That said, investors should tread carefully: historically, even high-quality momentum stocks experience sharp pullbacks when valuations disconnect too far from fundamentals.

In summary, Palantir’s Q2 results were stellar by almost any metric: revenue growth of nearly 50%, strong free cash flow, record contract wins, and raised guidance. The company has cemented itself as a central player in the AI software ecosystem, with both government and commercial demand accelerating. For traders, the setup remains favorable—momentum is strong, guidance is rising, and sentiment is exuberant.

For longer-term investors, however, caution is warranted. At nearly 300x forward earnings, Palantir’s valuation is beyond stretched, and the stock leaves little room for execution missteps or slowing growth. The froth is real, and those looking to initiate or add long-term positions would be better served waiting for a pullback.

Bottom line: Palantir remains one of the most compelling growth stories in the market, but at today’s levels, it’s more of a trade than a buy‑and‑hold. The fundamentals support further upside, yet prudent investors will want to keep valuation “out to the side” for now and watch for better entry points once the market inevitably cools.

WATCH: Crypto ETFs Are About to Explode — Canary Capital CEO Reveals What’s Coming Next!

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet