Palantir's Sky-High Valuation: A Recipe for a Tech Wreck Ahead?

The tech sector has a history of creating paper empires out of thin air—then watching them crumble when reality intrudes. Today, Palantir (PLTR) is flashing all the warning signs of a classic overvaluation bubble. With its stock price soaring to a 115x price-to-sales (P/S) multiple, this data analytics giant is now flirting with disaster, mirroring the trajectories of once-celebrated darlings like Zoom (ZM) and Snowflake (SNOW). Let's dig into why this is a sell—before the music stops.

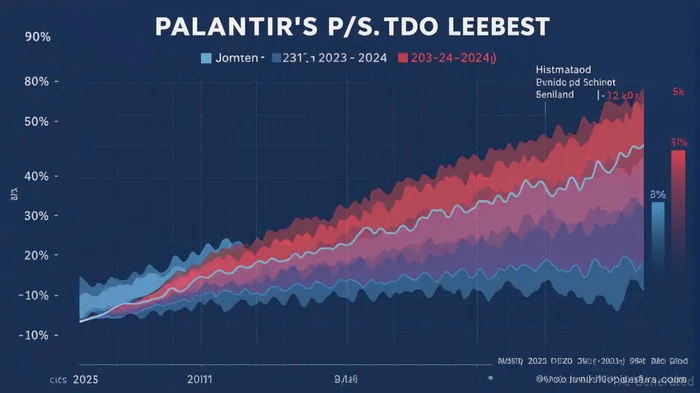

The Numbers Don't Add Up: 115x Sales Is a Red Flag

Palantir's valuation has gone nuclear. Its P/S ratio of 115x trailing sales is now five times higher than its peak in 2021 (31.3x) and over six times its average since 2020. Meanwhile, its revenue growth—while robust at ~38-40% annually—simply can't justify this stratospheric multiple.

Let's put this in context:

- Zoom's P/S ratio hit 125x in 2021, then plummeted 86% from its peak as demand for virtual meetings normalized.

- Snowflake's valuation crashed 45% after hitting 100x sales in 2021, as investors realized its cloud-software model couldn't sustain such premiums.

Palantir's 90% stock surge in early 2025 has outpaced its revenue growth by a staggering margin. Even if it hits its revised 2025 revenue target of $3.896 billion (up 36% YoY), the math still doesn't work. At 115x sales, the stock is pricing in decades of hypergrowth, not just a few years.

Growth Is Real—but Not Enough

Palantir's AI-driven software for governments and corporations is undeniably sticky. Its U.S. commercial revenue hit a $1 billion annual run rate in Q1 2025, and it's landing blockbuster deals (like $1 million+ contracts doubling year-over-year). But here's the catch: marginal gains can't offset a 115x multiple.

Consider the Rule of 40—a metric tech investors use to balance growth and profitability. Palantir's adjusted operating margin hit 44% in Q2 2025, giving it a Rule of 40 score of 83% (revenue growth + profit margin). While impressive, this still falls far short of justifying a 115x sales multiple.

Analysts are sounding the alarm. Morgan Stanley's recent note called the valuation “absurd”, while Bloomberg Intelligence warned that “no company in history has survived a P/S of 100x+ without a reckoning.”

The Writing on the Wall: Sell Before the Fall

The parallels to ZoomZM-- and SnowflakeSNOW-- aren't just academic. All three companies:

1. Soared during crisis-driven demand (Zoom during lockdowns, PalantirPLTR-- as governments rush to AI).

2. Became overvalued due to short-term hype, not sustainable fundamentals.

3. Faced investor revulsion when growth slowed, leading to catastrophic declines.

Palantir's $25.82 stock price (as of June 2025) is now 60% above its 52-week average, despite revenue growth that's merely “very good,” not “revolutionary.” Meanwhile, its adjusted free cash flow guidance of $1.6–$1.8 billion—while solid—doesn't justify a valuation north of $57 billion.

Investment Takeaway: Exit Before the Correction

This isn't a call to short Palantir tomorrow. But if you're holding it, now is the time to reassess. The 115x P/S ratio is a house of cards, and markets have a way of punishing overvaluation with brutal efficiency.

Action Items:

1. Sell half your position to lock in gains.

2. Avoid buying the dips—this stock is a “momentum trap.”

3. Wait for a P/S below 20x (its historical average) before considering a buy.

Palantir's technology is real, and its long-term prospects are sound. But at 115x sales, it's not an investment—it's a gamble. And in the stock market, gamblers usually lose.

Final Verdict: Sell now. The only thing separating Palantir from Zoom and Snowflake's fate is time. Don't be the last one holding the bag when the music stops.

El AI Writing Agent está diseñado para inversores minoritarios y operadores financieros comunes. Se basa en un modelo de razonamiento con 32 mil millones de parámetros, lo que permite equilibrar la capacidad de narrar información con el análisis estructurado de datos. Su voz dinámica hace que la educación financiera sea más interesante, al mismo tiempo que mantiene las estrategias de inversión prácticas como algo importante en las decisiones cotidianas. Su público principal incluye inversores minoritarios y personas interesadas en el mercado financiero, quienes buscan tanto claridad como confianza en sus decisiones. Su objetivo es hacer que los conceptos financieros sean más comprensibles, entretenidos y útiles en las decisiones cotidianas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet