Palantir Q4 Earnings Blowout! Revenue +70%, 2026 Outlook Stuns the Street

U.S. AI leader PalantirPLTR-- reported its 2025 Q4 earnings, significantly beating market expectations across the board.

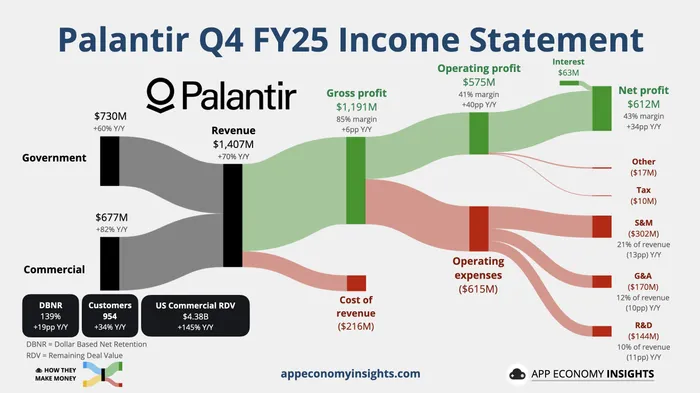

Quarterly revenue reached $1.41 billion, up 70% year over year, well above the consensus estimate of $1.34 billion. Adjusted earnings per share came in at $0.25, exceeding expectations of $0.23.

Palantir also delivered an exceptionally strong outlook for 2026. The company guided Q1 2026 revenue to a range of $1.532–1.536 billion, with the low end far above market expectations of $1.32 billion.

For full-year 2026, revenue is projected at $7.182–7.198 billion, significantly higher than the consensus estimate of $6.22 billion.

Following the earnings release, Palantir shares jumped more than 6% in after-hours trading.

CEO Alex Karp described the results as “the single best performance in the technology sector over the past decade,” calling it a “cosmic-level return” for shareholders.

Driven by President Trump’s emphasis on ICE and defense technology, Palantir’s U.S. government revenue surged 66%, with the majority coming from the Department of Defense.

In the summer of 2025, Palantir signed a 10-year contract worth up to $10 billion with the U.S. Army to support its software and data needs. In December, the company also secured a $448 million contract with the U.S. Navy to develop “ShipOS,” an operating system designed to support modern warship development. Demand from U.S. government contracts has been so strong that the company has struggled to allocate resources to U.S. allies.

Another key government customer is ICE. According to an analysis of government filings by the *Financial Times*, Palantir has received $81 million in ICE contracts since January 2025. This includes a $30 million agreement signed last April to build a system aimed at streamlining the “identification and apprehension of undocumented immigrants.”

Palantir’s cooperation with ICE dates back more than a decade, beginning during the Obama administration. While recent ICE enforcement actions have sparked controversy, Karp defended the partnership, arguing it helps secure U.S. borders. He stated that Palantir’s technology prevents terrorist attacks while also protecting citizens from unlawful government surveillance.

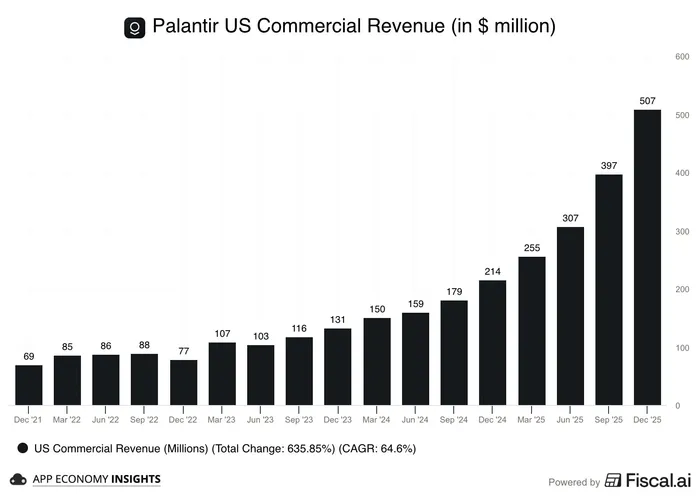

Beyond government contracts, Palantir’s commercial business also delivered standout performance. Commercial revenue reached $507 million, up 137% year over year. Karp noted that the company’s results are being driven by “an increasing number of discerning American enterprises and institutions that truly understand the value of artificial intelligence.”

However, geopolitical tensions are reshaping demand. Under Trump’s “America First” strategy, relations between Europe and the U.S. have deteriorated. Karp acknowledged that European clients are more inclined to use domestic vendors and have shown hesitation toward Palantir’s services. As a result, revenue from customers outside the U.S. fell to 23%, down from 33% in 2024.

Dispelling Valuation Concerns

Palantir has long faced criticism from analysts over its elevated valuation. This earnings report, however, reinforced that its high-growth trajectory justifies premium multiples. Karp emphasized that Palantir’s commercial segment benefits from surging demand for software that provides structural support for large language models. Companies that lack the ability to “actually catch mice,” he said, will inevitably fade into irrelevance.

On Monday, William Blair analyst Louis DiPalma upgraded Palantir from “Market Perform” to “Outperform,” noting that the prior pullback had made the company’s valuation “far more reasonable.”

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet