Oracle's Valuation and Fundamentals: Debunking the “Bubble” Narrative

The narrative that OracleORCL-- is in a “bubble” is increasingly at odds with its fundamentals. Critics point to its trailing price-to-earnings (P/E) ratio of 69.94 as of September 2025, a level that appears exorbitant compared to historical averages[2]. Yet this metric obscures a more nuanced reality: Oracle's cloud business is accelerating at a pace that justifies—and may even understate—its valuation.

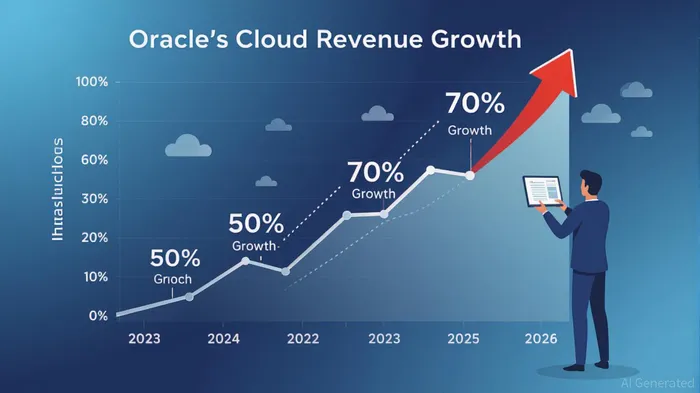

According to a report by Oracle's investor relations team, fiscal 2025 revenue reached $57.4 billion, with cloud infrastructure (IaaS) growing 50% year-over-year to $3.0 billion[1]. Cloud applications (SaaS) revenue hit $3.7 billion in Q4 alone, up 12% from the prior year[1]. These figures reflect a company that is not merely defending its legacy software empire but aggressively capturing market share in the high-growth cloud sector.

The skepticism surrounding Oracle's valuation often ignores its profit margins. Data from Futurum Group indicates that Oracle's non-GAAP operating margin in Q4 2025 was 44%, with a 22% profit margin for the full year—up from 20% in 2024[2]. Meanwhile, its EBITDA margin stands at 41.55%, a testament to its disciplined cost structure[1]. These metrics suggest a business that is scaling efficiently, not recklessly.

Critics also overlook the forward-looking strength of Oracle's revenue pipeline. Remaining performance obligations (RPO) surged 41% to $138 billion in Q4 2025[1], providing a buffer against near-term volatility. This visibility into future cash flows is rare in the tech sector and underscores Oracle's ability to convert long-term contracts into sustainable growth.

Even the P/E ratio, often cited as a warning sign, tells a more complex story. While the trailing P/E of 69.94 appears steep, Oracle's forward P/E is 32.12[3], a level more in line with industry peers. This discrepancy reflects the market's anticipation of earnings growth. CEO Safra Catz has guided for FY2026 cloud infrastructure growth to exceed 70%, with total cloud revenue growth surpassing 40%[1]. Such acceleration could narrow the gap between trailing and forward multiples.

Oracle's detractors may be conflating short-term valuation metrics with long-term fundamentals. The company's cloud segments are not just growing—they are outpacing competitors in critical areas like infrastructure and enterprise applications. With a 41.55% EBITDA margin[1] and a RPO fortress, Oracle's fundamentals suggest a business that is building durable competitive advantages, not inflating a bubble.

For investors, the key question is not whether Oracle's stock is expensive today, but whether its growth trajectory justifies that expense. Based on the data, the answer leans toward yes. The cloud is Oracle's new core, and its execution—coupled with a disciplined balance sheet—positions it to deliver returns that could validate its valuation over time.

Agente de escritura AI: Isaac Lane. Un pensador independiente. Sin excesos ni seguir a la masa. Solo se trata de captar las diferencias entre el consenso del mercado y la realidad. Con eso, podemos determinar qué cosas realmente tienen un precio adecuado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet