Oracle's AI Backlog Strengthens: Is Sustained Growth Ahead?

Oracle’s ORCL AI-driven backlog expansion is strengthening its growth outlook and improving forward revenue visibility. In the second quarter of fiscal 2026, Remaining Performance Obligations (RPO) climbed sharply year over year, reflecting robust AI-related demand from large enterprise customers. RPO, expected to convert within the next 12 months, increased 40%, highlighting strong near-term revenue realization and reinforcing confidence in sustained top-line momentum.

Cloud remains the main growth driver. Quarterly cloud revenues jumped 34% year over year to $8 billion, making up about half of the total revenues. This shift shows Oracle’s successful move toward recurring, AI-based revenue streams. Cloud Infrastructure led the way, boosted by higher GPU demand and quick growth in multi-cloud database use. These trends suggest that AI investments are now turning into real revenue growth instead of just long-term potential.

Management expects $4 billion in incremental revenues in fiscal 2027 tied directly to the recently signed AI contracts, alongside an unchanged fiscal 2026 revenue forecast of $67 billion, reinforcing forward visibility and contractual demand strength.

Oracle is aligning capital expenditure closely with contracted demand, prioritizing revenue-generating infrastructure and defined return thresholds. This disciplined allocation strategy helps mitigate overbuild risks while supporting scalable AI expansion.

With AI embedded across its infrastructure, database and applications stack, OracleORCL-- appears well-positioned to convert rising enterprise AI demand into durable, multi-year growth. The Zacks Consensus Estimate projects year-over-year total revenue growth of 16.6% in fiscal 2026 and 27.6% in fiscal 2027, supporting the case for sustained growth.

How Oracle’s AI Backlog Stacks Up Against Rivals

Despite Oracle’s ambitious push into AI infrastructure, hyperscalers like Amazon AMZN and Salesforce CRM present formidable competitive headwinds.

Amazon creates strong competition for Oracle in AI infrastructure. AMZN’s AWS has grown to a $142-billion annual revenue run rate, supported by a solid AI-driven backlog and rising enterprise demand. AMZN’s custom chips, such as Trainium and Graviton, improve cost efficiency and AI performance. While Oracle benefits from loyal database customers and growing RPO, AMZN’s larger scale and heavy AI investments highlight competitive pressure.

Salesforce competes with Oracle mainly in AI-driven applications, not infrastructure. CRM reported $72 billion in RPO, showing strong backlog visibility. CRM’s Agentforce platform is growing fast, with rising enterprise adoption and large government deals. While Oracle focuses more on AI infrastructure, CRM embeds AI into its core apps to drive workflow automation. CRM’s expanding AI backlog highlights how Oracle’s AI backlog stacks up against major software rivals.

ORCL’s Price Performance, Valuation & Estimates

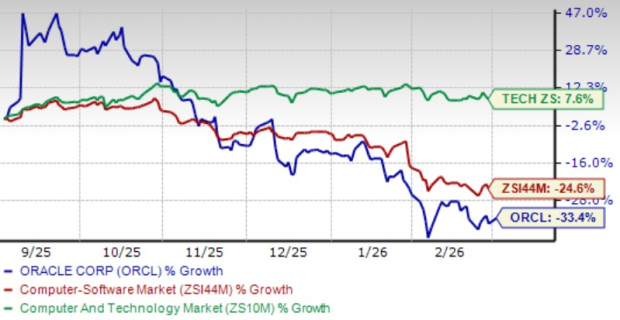

Shares of Oracle have declined 33.4% in the past six months, underperforming the Zacks Computer and Technology sector’s growth of 7.6% and the Zacks Computer - Software industry’s fall of 24.6%.

ORCL’s 6-Month Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, the ORCLORCL-- stock is currently trading at a forward 12-month P/E ratio of 18.81X, which is lower than the industry average of 21.79X. Oracle has a Value Score of D.

ORCL’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ORCL’s fiscal 2026 earnings is pegged at $7.45 per share, down 1 cent over the past 30 days. The earnings estimate suggests 23.55% growth over the figure reported in fiscal 2025.

Image Source: Zacks Investment Research

ORCL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet