Nvidia Has More Trouble Now: Fundamental Shift, Rich Valuation, and Technical Warnings

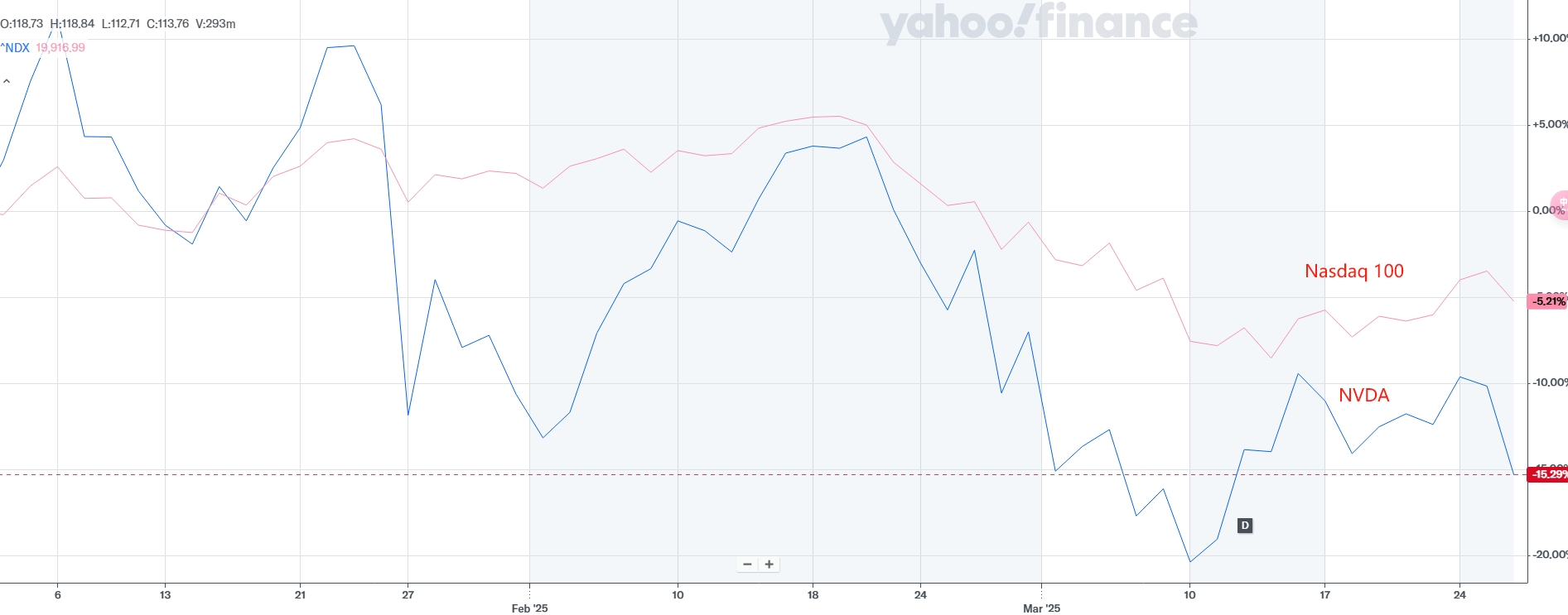

Nvidia has significantly lagged the Nasdaq 100's performance over the past two weeks, as macro headwinds loom. More importantly, concerns over a potential computing surplus are shaking its fundamentals, something investors once believed was unshakable. Although AI is still the future and NvidiaNVDA-- remains a key player, the GPU giant has failed to justify its evolving role as AI enters a more mature stage. Meanwhile, China's DeepSeek has demonstrated that clusters of super-advanced AI chips may not be a necessity but rather a luxury, raising concerns about Nvidia's long-term growth potential. From a fundamental, valuation, and technical standpoint, Nvidia now faces severe challenges in the foreseeable future.

A Failed GTC 2025 and Concerns Over Computing Oversupply

Nvidia's stock is currently 24% off its late January peak and down 15% year-to-date. While this may seem reasonable given that the Nasdaq 100 has fallen over 5% this year—and Nvidia naturally exhibits a higher beta—the real concern is its recent underperformance even as the benchmark rebounds. The stock has dropped 6% over the past two weeks, while the Nasdaq 100 has gained 1%, signaling a potential fundamental shift.

A disappointing GTC 2025 may have been the catalyst. Historically, Nvidia's AI conference has been a stock-moving event, but this time, it failed to deliver the usual hype. Jensen Huang unveiled the Blackwell Ultra, which promises faster model processing and is set to launch in the second half of this year. He also laid out a three-year roadmap, including the Robin architecture, Robin Ultra chip, and Feynman, all of which promise exponentially greater computing power. But here's the catch: it's all about computing power.

Despite Huang's insistence that more advanced models require 1,000 times the computing power of earlier ones, investors aren't buying it. They expect Nvidia, with its $2.78 trillion market cap, to innovate beyond just raw computing capacity. Meanwhile, China's DeepSeek has managed to build a competitive model at a fraction of OpenAI's cost, gaining widespread adoption among China's tech giants. Even more troubling, DeepSeek and other Chinese firms achieved this using Nvidia's older H800 and H20 chips, which are vastly inferior to the H100 and the current Blackwell. This raises a critical question: is the U.S. tech sector heading toward a computing power surplus?

U.S. tech giants have spent aggressively on AI infrastructure over the past two years, and they may soon realize they have overbuilt. If Nvidia's next-generation AI chips are still just about computing power, this could become a major problem.

There are already signs of a slowdown in AI spending. According to TD Cowen, Microsoft has withdrawn over 2GW of scheduled data center leases in the U.S. and Europe over the past six months, canceling or deferring existing agreements due to concerns about an oversupply of computing clusters. Some may blame this on OpenAI's shift to Oracle, but it could also reflect a broader realization that tech giants already have enough AI chips—at least in the short term. With Q1 earnings on the horizon, we may see even stronger signals of an AI spending pullback, which could pose a significant threat to Nvidia's growth.

Financial Prospects: Slowing Growth and Shrinking Surprises

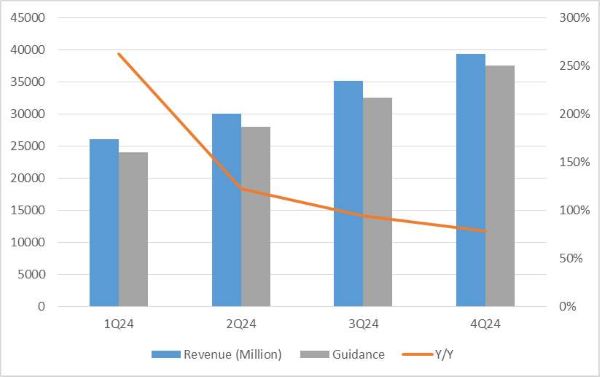

Nvidia's revenue growth has been decelerating for four consecutive quarters, from 262% year-over-year in Q1 to 78% in Q4. The slowdown is expected to continue in Q1 2025, with projected growth of 65% (based on guidance). These numbers do not yet account for the impact of DeepSeek R1, which emerged in late January—meaning the next few quarters could reveal even greater downside risk.

While some of this deceleration is due to tougher year-over-year comparisons, the real concern is the shrinking revenue surprise factor. Nvidia's quarterly revenue has exceeded guidance by 9%, 7%, 8%, and 5% in the last four quarters, respectively. A hyper-growth company should consistently deliver big surprises, but Nvidia's trend suggests it is transitioning to a normal growth phase—hardly exciting news for investors, especially retail traders who thrive on hype.

From a valuation standpoint, Nvidia remains the most expensive among the Magnificent Seven when measured by P/S and PSG ratios. Nvidia's P/S ratio currently stands at 17.7, far higher than Microsoft's 10, the second highest. The PSG ratio, which adjusts for growth rate, places Nvidia at 9.94, close to Microsoft at 9.26 and Tesla at 8.35. While Nvidia's high growth rate has justified its premium valuation so far, as growth slows, the PSG ratio will inflate, making the stock appear even more expensive. If Nvidia's core GPU business weakens, investors may push for a valuation reset—potentially triggering a brutal sell-off.

Technical Warnings

Nvidia's technical setup is flashing multiple warning signs. Despite a bounce from the March 11 low, the stock remains in a downtrend with a lower-high pattern. The $120 resistance level has proven difficult to break. Wednesday's drop turned the 3-day moving average downward again, threatening to break below the 7-day and 10-day moving averages—a classic sell signal. If Nvidia breaks below $105, the next leg down could be steep.

From fundamental, financial, and technical perspectives, Nvidia faces increasing challenges. Despite its still-rich valuation, its core business lacks fresh innovation, which could push investors to rethink their allocations. Nvidia's meteoric rise has made it the third-largest company in the stock market, but investors should remain cautious—the entire AI infrastructure boom has been supporting its valuation, and if that support weakens, the risk of a deeper downturn grows.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.