Nvidia’s Solid Quarter Meets High Bar as Conservative China Outlook Tempers Excitement

Nvidia’s second-quarter fiscal 2026 results delivered strong growth across its key businesses, but the stock slipped around 2% in after-hours trading as Wall Street wrestled with expectations that may have simply been too lofty. The company topped consensus on revenue and EPS, reaffirmed its robust margin profile, and expanded its capital return program. Yet the modest beats and a cautious stance on China left investors wanting more, underscoring how elevated expectations have become for the company that sits at the heart of the AI revolution.

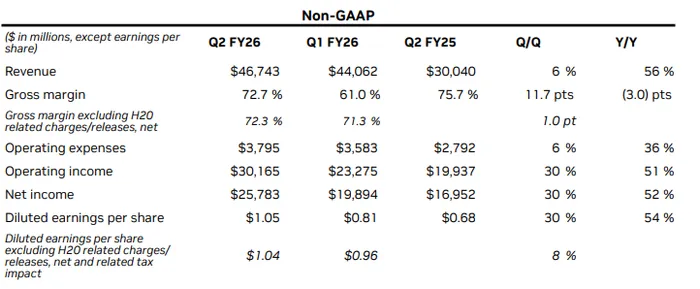

Numbers at a Glance NvidiaNVDA-- posted Q2 revenue of $46.7 billion, up 56% year-over-year and 6% sequentially, ahead of consensus at $46.2 billion. Adjusted EPS of $1.05 beat the Street’s $1.01 forecast. Gross margins were a highlight, climbing to 72.7% on a non-GAAP basis, up more than 11 points sequentially and comfortably ahead of guidance. Operating income rose 73% year-over-year to $28.4 billion, while net income jumped 59% to $26.4 billion.

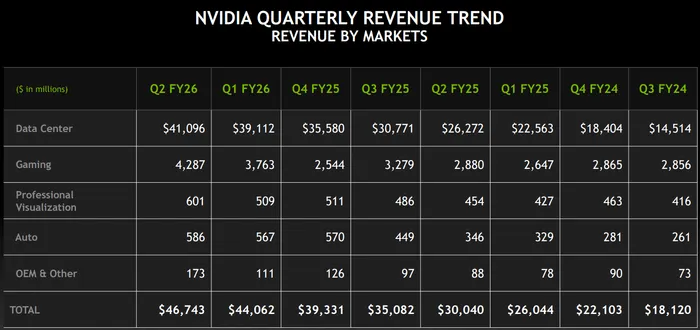

Segment performance was solid across the board. Data Center revenue surged 56% from a year earlier to $41.1 billion, though it narrowly missed estimates and showed only a 5% sequential gain, weighed by a 1% drop in compute revenue. Networking provided the offset, surging 46% sequentially and nearly doubling year-over-year to $7.3 billion. Gaming revenue rose 49% year-over-year and 14% sequentially to $4.3 billion, reflecting a rebound in GPU demand and broad RTX adoption. Professional Visualization climbed 32% year-over-year to $601 million, Automotive revenue advanced 69% to $586 million, and OEM & Other nearly doubled to $173 million, boosted by sales of previously reserved H20 inventory to non-China customers.

Guidance and China Uncertainty For Q3, Nvidia guided revenue to $54 billion, plus or minus 2%, above consensus at $53.5 billion but short of the blowout some investors hoped for. Crucially, management made clear that guidance does not include any assumption for sales of H20 products into China. CEO Jensen Huang and CFO Colette Kress acknowledged that demand exists and licensing approvals could allow shipments as soon as October, but said it would be premature to include that in the official outlook.

That caution underscores the geopolitical risks surrounding U.S.-China tech trade. Huang estimated China could represent a $50 billion market for Nvidia this year if fully accessible and could grow 50% annually. He described China as “the second largest computing market in the world” and home to about half of global AI researchers, stressing the importance of U.S. companies maintaining a foothold. Still, until Washington’s regulatory stance is clarified, Nvidia is deliberately keeping China contributions out of its near-term forecasts.

Wall Street read between the lines: Nvidia’s official $54 billion guide could effectively translate to $56–59 billion if $2–5 billion in China H20 shipments materialize in the quarter. On that adjusted basis, growth would accelerate beyond what was feared heading into earnings. Yet for now, management’s conservative posture kept excitement in check.

Addressing Market Share Concerns Analysts pressed Huang on whether Nvidia is losing market share to custom ASICs or rivals in hyperscale accounts. He pushed back firmly, arguing that Nvidia’s full-stack approach—from GPUs and CPUs to networking, software, and system integration—creates an unmatched platform. He noted that ASICs struggle to keep pace with evolving AI models and workloads, while Nvidia’s ecosystem accelerates every stage of the pipeline. “Our platform breadth and performance per watt give customers lifetime utility and margins that remain highest,” Huang said.

The company also emphasized continued dominance in hyperscaler demand. Major cloud service providers now account for about half of Data Center revenue, and demand for both Hopper and Blackwell architectures remains overwhelming. Huang described the market as “sold out” for H100s and H200s, with CSPs even renting capacity from one another. While hyperscaler CapEx has doubled to $600 billion annually, Nvidia is also seeing diversification, with sovereign AI initiatives, enterprise adoption, and AI-native startups scrambling for capacity.

Beyond Hyperscalers: Where Growth Can Come From One of the themes of the call was Nvidia’s effort to broaden its revenue base beyond hyperscalers. The company said it is on track to generate $20 billion in sovereign AI revenue this year, more than doubling from last year, with governments in Europe and elsewhere building AI “factories” powered by Nvidia. The EU alone plans €20 billion of investment to deploy 20 AI facilities, including five giga-scale projects.

Enterprise demand is also becoming more meaningful, with large corporations seeking to deploy agentic and reasoning AI models internally. Huang noted that reasoning workloads require 100x to 1000x more compute than training, pointing to an expanding long-term opportunity. Meanwhile, networking is emerging as a growth pillar, with Spectrum-X Ethernet and InfiniBand helping interconnect multi-GW AI factories.

This diversification matters, as investors are keen to see Nvidia maintain growth even if hyperscaler spending cycles normalize. The company’s push into sovereign and enterprise AI, coupled with innovations like NVLink-72 and the upcoming Rubin platform, suggests multiple levers to sustain momentum.

Capital Returns and Balance Sheet Nvidia paired its earnings with shareholder-friendly announcements. The board authorized an additional $60 billion for share repurchases, one of the largest buyback programs in history, and declared a $0.01 quarterly dividend. In Q2 alone, Nvidia returned $10 billion to investors, including $9.7 billion in buybacks. With $56.8 billion in cash and equivalents on hand, the company remains well-positioned to balance capital returns with aggressive investment in next-generation products.

Investor Sentiment and Market Impact Despite the solid quarter and constructive guidance, shares fell after-hours as investors digested the tempered outlook. At roughly 7.2% of the S&P 500’s weighting, Nvidia’s moves ripple across the broader market, and a pullback below $172 could bring the 50-day moving average near $169 into play. Still, analysts characterized the commentary as reassuring, with little evidence of weakening demand or structural red flags.

If anything, Nvidia’s conservatism on China provides a potential upside lever. Should licensing approvals allow H20 or Blackwell shipments into China, revenue could surge beyond current guidance. Huang’s comments reinforced that the demand backdrop remains extraordinary, with every major AI platform sold out and capacity scarce across the ecosystem.

The Bottom Line Nvidia’s Q2 FY26 results were strong by almost any measure—double-digit revenue growth, robust margins, and accelerating demand across Gaming, Visualization, and Automotive. But against the backdrop of AI-fueled euphoria, solid was not spectacular. By excluding potential China revenue from guidance, management set a lower bar that could ultimately prove beatable if geopolitical clouds clear.

For now, investors are likely to remain cautious, with shares digesting gains of more than 50% in the past six months. But the core story hasn’t changed: Nvidia is still at the center of what CEO Jensen Huang calls a new industrial revolution, with AI infrastructure demand projected at $3–4 trillion by decade’s end. The near-term volatility reflects expectations management, not cracks in the foundation.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet