Nvidia Q4 Beats Big,China Could Be the Next Upside Surprise

Nvidia reported fiscal Q4 2025 results (covering October 26, 2025 to January 31, 2026), delivering a blowout quarter that eased market concerns over massive AI capital expenditures.

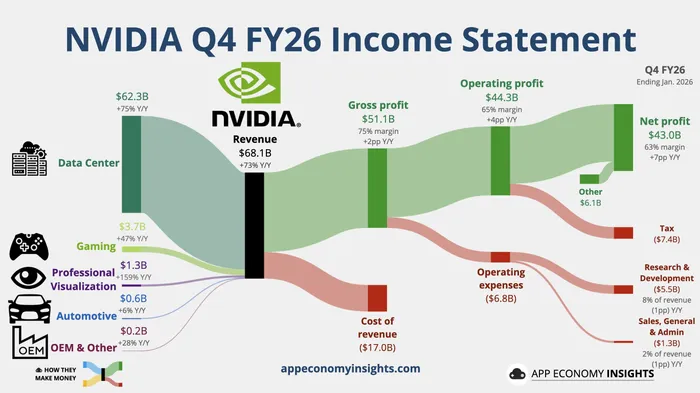

Q4 revenue reached $68.1 billion, beating the market expectation of $65.684 billion, up 73% year-over-year. Most critically, data center revenue totaled $62.3 billion, surpassing the expected $60.62 billion, up 75% year-over-year.

Q4 gross margin came in at 75%, in line with analyst expectations, and the company expects this level to persist into fiscal Q1 2026. Adjusted EPS also exceeded forecasts.

On guidance, NvidiaNVDA-- expects fiscal Q1 2026 revenue of $76.44–$79.56 billion, well above the consensus estimate of $72.78 billion. Notably, this guidance excludes the China market, and the H200 generated no revenue during the quarter. If shipments to China resume, that would represent incremental upside.

Nvidia shares rose more than 4% in after-hours trading, briefly breaking above $200 before trimming gains to trade near $198 at the time of writing.

Customers Keep Spending; $500B Outlook Too Conservative

During the earnings call, Jensen Huang stated that customers are racing to invest in AI, with compute demand growing exponentially. Nvidia has strategically secured inventory and capacity to meet demand over the coming quarters, with sufficient capacity visibility extending into 2027. However, advanced-node chip capacity remains tight.

Grace Blackwell powered by NVLink is currently the leader in inference, reducing inference cost per token by an order of magnitude. The next-generation Vera Rubin will further solidify Nvidia’s leadership.

CFO Colette Kress dismissed concerns of an AI bubble. She noted that customers such as Meta are generating substantial returns from AI investments, suggesting spending will continue to rise. Nvidia expects sequential quarterly revenue growth throughout fiscal 2026, easily surpassing the previously announced $500 billion annual revenue outlook shared at GTC.

Hyperscalers—including Microsoft Azure and Google Cloud—remain the largest customers, accounting for roughly half of data center revenue. However, most incremental growth is coming from non-hyperscale customers, reducing dependence on a handful of large players.

Ongoing mass production of Blackwell is improving margins, supported by a better product mix and improved cost structure. Earlier this week, the first test samples of Vera Rubin were shipped to customers.

Nvidia disclosed two key data center figures:

Data Center Compute revenue: $51.334 billion, up 58% year-over-year, slightly faster than Q3’s 56%.

Data Center Networking revenue: $10.98 billion, up 263% year-over-year, significantly accelerating from Q3’s 162%.

The surge in networking revenue was attributed to the continued strength of NVLink compute fabric, alongside growth in Ethernet and InfiniBand platforms. In other words, investors should not focus solely on GPU shipment volumes. Nvidia is bundling compute, interconnect, and systems into an integrated solution that is increasingly difficult to substitute. The rapid growth in networking revenue reflects the financial payoff of this strategy.

Another highlight was sovereign AI demand across countries, with related revenue tripling.

Nvidia also acknowledged that Chinese competitors are “making progress,” particularly newly listed companies such as Moore Threads. These emerging AI players may affect Nvidia’s competitive landscape globally.

Analyst Views

Jacob Bourne of Emarketer noted that hyperscalers have mapped out tens of billions in capital expenditures, keeping demand for Nvidia chips robust. However, the competitive landscape is evolving: Meta has begun shifting toward AMD, while Microsoft, Google, and Amazon are developing in-house chips. Markets are increasingly focused on Nvidia’s forward guidance—specifically how it maintains dominance as AI infrastructure matures and shareholders demand returns on capital.

According to Bloomberg Intelligence analyst Kunjan Sobhani, the biggest surprise was the raised Q1 guidance, indicating faster-than-expected ramp-up of GB300 capacity. Networking drove much of the upside in data center results, implying higher penetration of NVLink and Spectrum. The key swing factors for sentiment remain how much the $500 billion revenue outlook can be revised upward and whether shipments to China resume.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet