Nvidia Q3 Preview: Will Strong Guidance Revive the Fading AI Story?

After the U.S. market close, Nvidia—the world’s largest company by market value—will release its fiscal 2026 third-quarter earnings (natural year July 28 to October 26, 2025), drawing global attention.

This comes at a time when the AI narrative is facing growing skepticism. Funds such as SoftBank and Bridgewater have aggressively cut their Nvidia positions, while Oracle’s massive debt-fuelled AI gamble triggered a dual sell-off in its stocks and bonds. Investors are now looking to Nvidia’s earnings to restore confidence in AI.

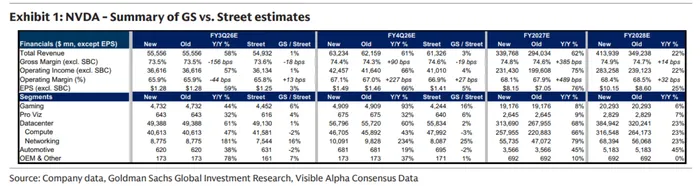

The market expects Nvidia to report Q3 revenue of $55.5 billion, up 58% year-on-year, and EPS of $1.26, up 59% year-on-year. With the global AI capex boom underway, an earnings beat is almost guaranteed. The real question is: how high will the guidance go?

Blackwell capacity ramp-up is the biggest driver of Nvidia’s earnings

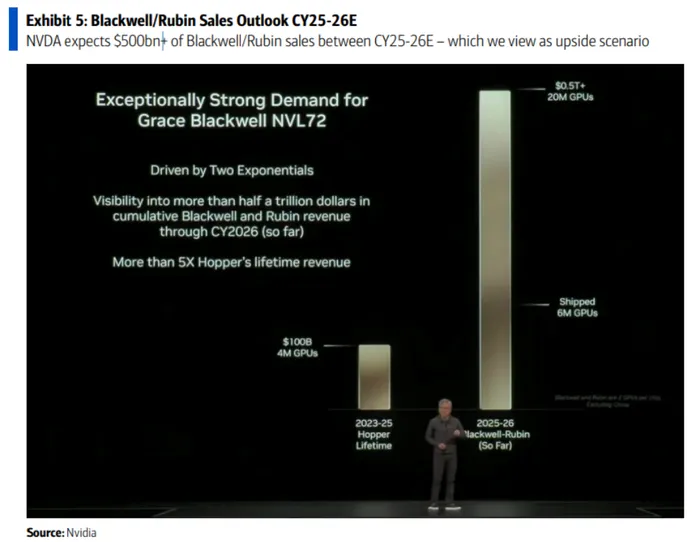

J.P. Morgan noted in its latest report that Blackwell rack shipments are entering a rapid acceleration phase. Supply remains far below demand, and the only constraint on Nvidia is capacity. Blackwell output is expected to rise to 10,000 units in Q3, up 50% quarter-on-quarter, with similar growth expected in Q4. Q4 revenue guidance is projected to reach USD 63–64 billion.

Nvidia’s supply chain is capable of doubling Blackwell shipments in fiscal 2027 (natural year 2026) to 60,000–70,000 units. According to data disclosed at the October GTC event, Nvidia already has more than 70,000 backlog orders for 2026—exceeding its maximum annual capacity—providing extremely high visibility for future growth.

GPU refresh cycles and massive AI capex secure Nvidia’s future growth

“Data-center GPUs have a lifespan of one to three years, and major cloud service providers may begin refreshing first-generation AI infrastructure as early as next year. Microsoft has hinted that aging equipment will need replacement. This gives Nvidia exceptionally strong growth visibility,” said Seeking Alpha buy-side analyst Michael Del Monte.

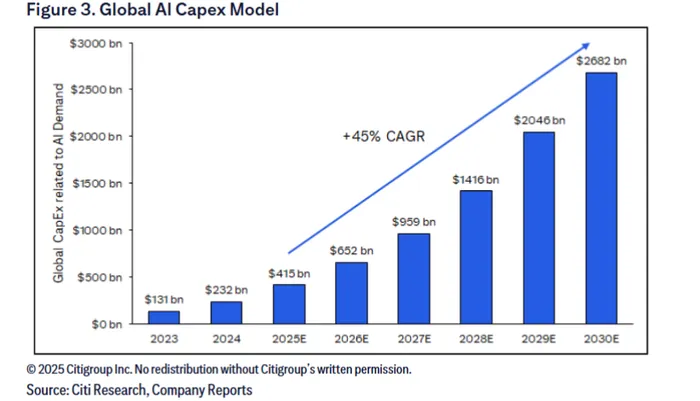

Citi forecasts global AI capital expenditure to reach USD 415 billion in 2025 and USD 2.682 trillion by 2030—a five-year CAGR of 45%.

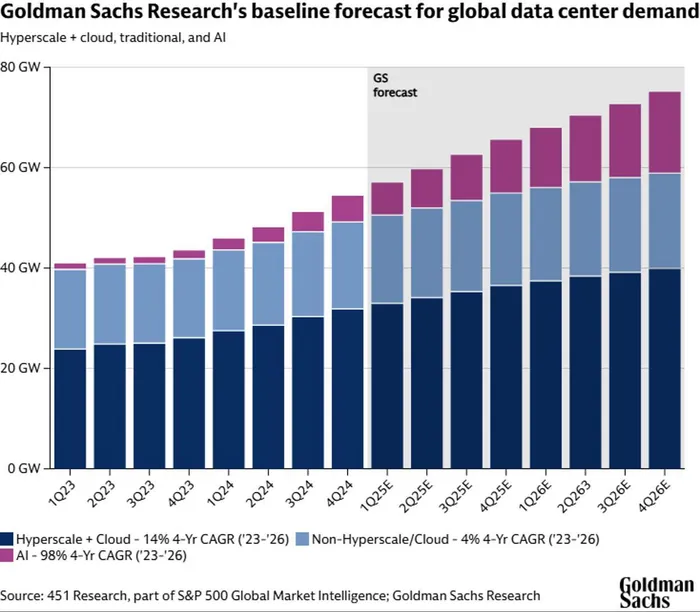

Goldman Sachs expects global data-center demand to surge from 40 GW in early 2023 to 80 GW by the end of 2026, with Nvidia capturing the largest share of the build-out.

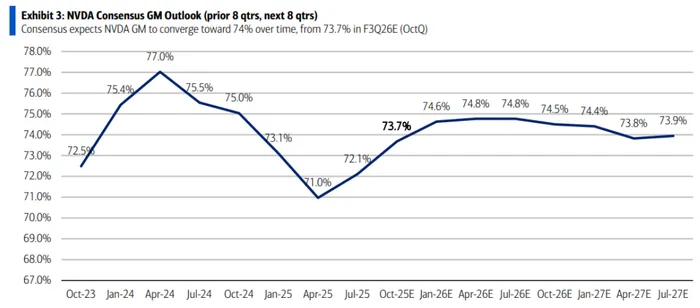

On profitability, Nvidia’s average net margin over the next five years is expected to reach 57%. The drivers are clear: continued mix shift toward high-margin Data Center products, and Nvidia’s increasingly powerful CUDA software ecosystem—a moat comparable to Microsoft Windows or Apple iOS, binding millions of developers and enabling strong pricing power.

With rising costs for memory, optical modules, and advanced packaging, Nvidia may even raise prices, showcasing its bargaining strength.

China market and networking business could be upside surprises

Last quarter, Nvidia booked zero revenue from China. With U.S.–China trade tensions easing, Nvidia’s related products may re-enter China’s vast market. Jensen Huang previously said China could represent a USD 50 billion opportunity.

Beyond Blackwell, Nvidia’s networking business could become another major growth engine. Spectrum-X has already exceeded USD 10 billion in annualized revenue. Combined with capacity expansion in NVL72 and NVL72/144 driving NVLink Fabric growth, Nvidia’s networking revenue could grow nearly 90% year-on-year in fiscal 2027.

What risks does Nvidia face?

First, customer in-house chips. OpenAI, Google, Meta, Microsoft, and Amazon are all accelerating development of proprietary AI chips, while AMD’s MI300 series is gaining broader adoption. Although these are unlikely to challenge Nvidia’s dominance in the short term, they may influence procurement patterns in coming years.

Second, customers’ strained cash flow. OpenAI, Oracle, and others have AI infrastructure ambitions far exceeding their internal cash flow, forcing them into heavy borrowing. Even Meta is struggling with capex demands, increasing market skepticism.

Third, Nvidia sits upstream in the data-center supply chain, and its order trends lead cloud-service budgets by roughly two quarters. If Jensen Huang signals continued acceleration in AI investment, tech valuations may hold; but if Nvidia hints at slowing customer orders, the sector could face valuation pressure.

Finally, power-supply bottlenecks and community resistance may delay data-center construction, indirectly affecting GPU demand.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet