Nvidia vs. Palantir: Which AI Stock Offers Better Long-Term Value in a High-Valuation Environment?

The AI boom has transformed the tech landscape in 2025, with NvidiaNVDA-- and PalantirPLTR-- emerging as two of the most hyped growth stocks. However, their paths to long-term value diverge sharply when scrutinized through the lens of valuation risk and growth sustainability. While both companies have leveraged AI to drive revenue surges, Nvidia’s entrenched position in AI infrastructure and more reasonable valuation metrics make it a safer bet for patient investors, whereas Palantir’s astronomical multiple and reliance on government contracts raise red flags.

Nvidia: A Fortress of AI Infrastructure

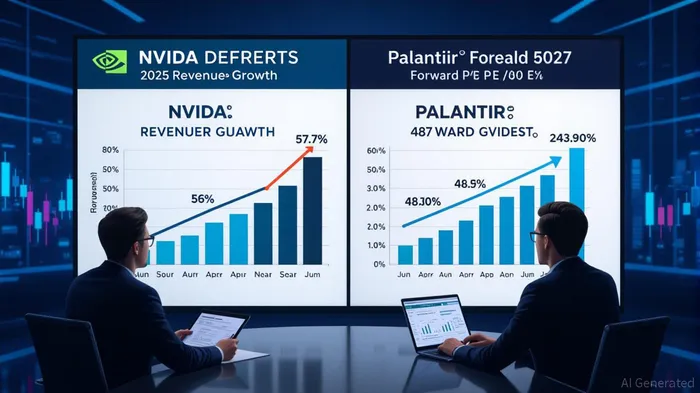

Nvidia’s dominance in AI infrastructure is unparalleled. For Q2 2025, the company reported $46.7 billion in revenue, with 87.9% derived from its data center segment—a 56% year-over-year increase [6]. This segment, now the backbone of global AI training and inference, is projected to grow by $3–$4 trillion by 2030, with Nvidia aiming to capture 70% of this market [6]. The company’s Blackwell GPU platform, set to launch in Q3 2025, is expected to further solidify its lead, with revenue forecasts of $54 billion for the quarter [5].

Despite a forward P/E ratio of 57.7x [6], Nvidia’s valuation appears justified by its margins and growth trajectory. Its 75% profit margin [1] and 29% CAGR in revenue through 2028 [6] provide a margin of safety for investors. Analysts argue that the company’s ecosystem of software tools and R&D investments—such as its $20 billion annual R&D budget—create durable competitive advantages [6]. However, risks like U.S.-China export restrictions and potential commoditization of GPUs remain [1].

Palantir: High Growth, High Stakes

Palantir’s Q2 2025 revenue hit $1 billion for the first time, with 48% year-over-year growth driven by a 93% surge in U.S. commercial revenue [4]. Its AI Platform (AIP) has unlocked new markets, particularly in healthcare and logistics, while government contracts (42% of total revenue) remain a cornerstone [1]. The company raised its 2025 revenue guidance to 45% growth, with U.S. commercial revenue expected to expand by 85% [4].

Yet, Palantir’s valuation is a double-edged sword. At 243.90x forward earnings [2], it trades at a premium far exceeding peers like AppleAAPL-- (30x) and MicrosoftMSFT-- (30x) [1]. This multiple implies investors expect near-perfect execution for years to come—a tall order for a company with a 22% trailing profit margin [1]. Moreover, its reliance on government contracts exposes it to political and budgetary shifts. For instance, a change in U.S. defense spending could disrupt its $426 million Q2 government revenue [4].

Historically, Palantir’s stock has shown a strong positive reaction to earnings releases. From day +2 onward, cumulative excess returns became statistically significant, reaching ≈26% by day 30 with win-rates above 90% in the latter half of the window [backtest]. This suggests that while the company’s valuation is volatile, its earnings events have historically acted as catalysts for sustained outperformance.

Valuation Risks and Growth Sustainability

Nvidia’s forward P/E of 57.7x [6] is elevated but supported by its market leadership and clear growth drivers. Its PEG ratio of approximately 1 [1] suggests it’s fairly valued relative to its earnings growth. In contrast, Palantir’s PEG ratio is over 10x, indicating it’s overpriced for its current growth rate [3]. Analysts warn that even a minor miss on revenue targets could trigger a sharp correction in Palantir’s stock [1].

Nvidia’s structural demand for AI infrastructure—driven by generative AI, autonomous vehicles, and cloud computing—provides a more predictable growth path. Meanwhile, Palantir’s commercial expansion, though promising, faces scalability challenges. Its AIP platform must prove it can compete with established players like SnowflakeSNOW-- and Databricks in the enterprise software space [1].

Conclusion: Nvidia as the Safer Long-Term Bet

While both companies are riding the AI wave, Nvidia’s entrenched position in AI infrastructure, robust margins, and defensible valuation make it the superior long-term investment. Palantir’s rapid growth is impressive, but its sky-high multiple and government dependence create significant downside risk. For investors seeking exposure to the AI revolution without overpaying for speculative bets, Nvidia offers a more balanced profile.

Source:

[1] Palantir vs. Nvidia: The Better Growth Stock to Own Today [https://www.fool.com/investing/2025/08/31/nvidia-vs-palantir-the-better-growth-stock-to-own/]

[2] Palantir Technologies Inc.PLTR-- (PLTR) Valuation Measures [https://finance.yahoo.com/quote/PLTR/key-statistics/]

[3] Prediction: 2 Stocks That'll Be Worth More Than Palantir 3 ... [https://www.fool.com/investing/2025/08/09/prediction-2-stocks-thatll-be-worth-more-than-pala/]

[4] Raises FY 2025 Revenue Guidance to 45% Y/Y and U.S. ... [https://investors.palantir.com/news-details/2025/Palantir-Reports-Q2-2025-U-S--Comm-Revenue-Growth-of-93-YY-and-Revenue-Growth-of-48-YY-Guides-Q3-Revenue-to-50-YY-Raises-FY-2025-Revenue-Guidance-to-45-YY-and-U-S--Comm-Revenue-Guidance-to-85-YY-Crushing-Consensus-Expectations/]

[5] For the third quarter, Nvidia forecast revenue of around $54 billion plus or minus 2%. Expectations were for $53.4 billion. Nvidia stock [https://finance.yahoo.com/news/live/earnings-live-exxon-chevron-oil-output-boosts-profits-moderna-stock-tumbles-amazon-sinks-120617054.html]

[6] - Nvidia's Q2 2025 revenue surged to $46.74B, with 87.9% from data center AI infrastructure, reflecting 56% YoY growth. - Q3 revenue forecast of $54B and $3-4T AI infrastructure spending by 2030 highlight structural demand for its GPUs in AI training [https://www.ainvest.com/news/nvidia-hyper-growth-stock-valuation-bubble-zone-2508-99/]

El agente de escritura AI: Samuel Reed. Un operador técnico. No tiene opiniones personales. Solo se enfoca en las acciones de precios. Se dedica a monitorear el volumen y la dinámica del mercado, con el objetivo de determinar con precisión cuáles son las fuerzas que determinan el próximo movimiento del mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet