Nvidia Obliterates Estimates, Sends Stock Soaring Past $200 as AI Frenzy Intensifies

Nvidia just delivered another quarter that makes “beat and raise” feel like an understatement, posting fiscal Q4 results that cleared both consensus and the more demanding whisper numbers while reminding investors that the AI buildout is still in the “customers racing” phase, not the “customers optimizing” phase. The company reported non-GAAP EPS of $1.62 versus the Street at $1.53, on revenue of $68.1 billion versus consensus around $66.0 billion. More importantly for positioning, the top line also beat the $68 billion whisper number you flagged, a meaningful point given how elevated expectations were headed into the print. In after-hours trading, shares popped into the psychologically important $200 area and have been holding there as the market waits for the conference call, which begins at 5:00 p.m. ET.

Guidance was the real mic drop. NvidiaNVDA-- guided fiscal Q1 revenue to $78.0 billion, plus or minus 2% (a range of roughly $76.44B to $79.56B), well above consensus estimates around the low-$73B area and above the $74B whisper number. Gross margin guidance also remained strong, with Nvidia expecting Q1 GAAP and non-GAAP gross margins of 74.9% and 75.0%, respectively, plus or minus 50 basis points. And crucially—because this will come up repeatedly as investors handicap the next few quarters—management again emphasized it is not assuming any data center compute revenue from China in the Q1 outlook. That “China excluded” caveat makes the guide feel less like a stretch and more like a statement about demand visibility elsewhere, even as the company noted it has not generated revenue to date under an H200 licensing program and does not yet know whether imports will be allowed into China.

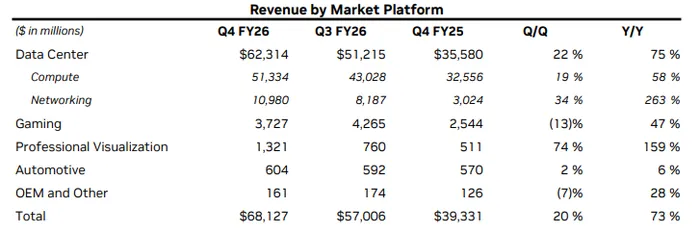

At the segment level, Q4 showed the core data center engine still accelerating and the platform approach (compute plus networking) tightening its grip on the AI infrastructure stack. Data Center revenue came in at $62.3 billion, beating estimates near $60.4 billion, and was up 22% sequentially from $51.2 billion in Q3 and up 75% year over year from $35.6 billion in the prior-year quarter. Within that, Compute revenue was $51.3 billion, up 19% quarter over quarter and up 58% year over year, while Networking revenue surged to $11.0 billion, up 34% sequentially and up a staggering 263% year over year. That networking line is becoming impossible to ignore: management attributed the strength to the ramp of NVLink compute fabric for GB200 and GB300 systems and growth in Ethernet and InfiniBand platforms, reinforcing the idea that the “GPU sale” is increasingly a “rack sale,” with Nvidia capturing more of the bill of materials and the performance-per-watt narrative in one bundle.

Outside data center, results were mixed but broadly supportive of the bull case that Blackwell is lifting multiple product families, even as gaming carries some near-term supply noise. Gaming revenue was $3.73 billion, down 13% sequentially from $4.27 billion but up 47% year over year from $2.54 billion. Management framed the sequential decline as normal channel inventory moderation after a strong holiday season, but also warned that supply constraints will be a headwind to Gaming in fiscal Q1 and beyond. Professional Visualization was a standout, with revenue of $1.32 billion, up 74% sequentially from $760 million and up 159% year over year from $511 million, again driven by strong Blackwell demand. Automotive was $604 million, up 2% sequentially and up 6% year over year, reflecting steady adoption of self-driving platforms rather than any step-change. OEM and Other was $161 million, down 7% sequentially but up 28% year over year, and remains immaterial in the context of the overall model.

From a P&L quality standpoint, margins and operating leverage were both better than feared, which matters because one of the recurring bear arguments has been that “the ramp gets harder” as the numbers scale. Gross margin improved meaningfully, with Q4 GAAP gross margin at 75.0% and non-GAAP at 75.2%, up 1.6 points sequentially and roughly 2 points year over year on the GAAP line. Nvidia said the year-over-year improvement was helped by lower inventory provisions, while the sequential lift reflected Blackwell ramping with an improved mix and cost structure. Operating expenses did grow quickly—GAAP opex rose 16% quarter over quarter and 45% year over year to $6.79 billion, while non-GAAP opex rose 21% sequentially and 51% year over year to $5.10 billion—but revenue grew faster, preserving the operating leverage story. On a GAAP basis, operating income was $44.30 billion (up 23% q/q, up 84% y/y) and net income was $42.96 billion (up 35% q/q, up 94% y/y). Non-GAAP net income was $39.55 billion (up 25% q/q, up 79% y/y), with non-GAAP EPS at $1.62 (up 25% q/q, up 82% y/y). Translation: expenses are rising with headcount and infrastructure investment, but the revenue engine is still outrunning them.

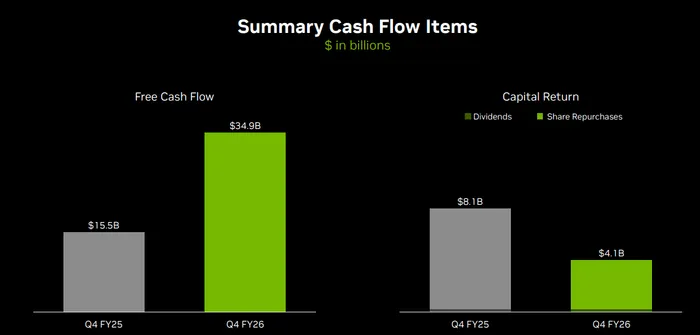

Management’s commentary continued to lean heavily into demand visibility and the idea that compute demand is expanding rather than saturating. Jensen Huang’s messaging was straightforward: customers are “racing” to invest in AI compute and overall computing demand is growing exponentially. That tone matters because the market is less interested in whether Nvidia beat Q4—most expected it would—and more focused on whether the CEO sounds like he’s managing scarcity and a multi-quarter backlog, or managing digestion and cancellations. On that front, Nvidia’s balance sheet and supply-chain commentary did more to calm nerves than raise them. The company ended the quarter with $62.6 billion in cash, cash equivalents, and marketable securities, up from $60.6 billion in Q3 and $43.2 billion a year ago, supported by stronger operating cash generation. Cash flow from operations was $36.2 billion, up sharply from $23.8 billion in Q3 and $16.6 billion a year ago, reflecting the scale of revenue and profitability.

At the same time, Nvidia is clearly spending to stay ahead of demand and to fund the ecosystem around its platform. Inventory rose to $21.4 billion from $19.8 billion sequentially, while total supply-related commitments increased to $95.2 billion, which management framed as intentionally securing inventory and capacity to meet demand beyond the next several quarters. The company also disclosed multi-year cloud service agreements of $27.0 billion, up slightly from $26.0 billion, to support growing research and development needs—an underappreciated “cost of doing business” in the AI era, where model training, simulation, and software development require massive compute resources even inside the company. Nvidia also returned $4.1 billion to shareholders in the quarter via $3.8 billion of repurchases and $243 million of dividends, and it returned $41.1 billion for the full fiscal year, signaling it can fund growth, secure supply, and still run an aggressive capital return program.

China remains the big optionality—and the big uncertainty—yet the near-term narrative was intentionally constructed to keep the base case clean. Nvidia reiterated it is not assuming any data center compute revenue from China in the Q1 outlook, noted it has not generated revenue under the H200 licensing program, and warned that any H200 shipped under a new licensing program would be subject to a 25% tariff upon importation into the U.S. The company also referenced a $4.5 billion charge tied to H20 excess inventory and purchase obligations as a factor that impacted FY26 gross margin. Investors will likely treat China as a swing factor rather than a requirement for the current guide, which is exactly the message management appears to be pushing: demand is strong enough elsewhere to carry the next few quarters, with China a potential “when/if” lever later.

Put it all together and the market reaction makes sense. Nvidia beat consensus and the tougher whispers, data center strength was broad with networking increasingly doing real work in the model, margins improved as Blackwell ramped, and Q1 guidance cleared the bar by a wide margin without leaning on China. With the stock tagging and holding the $200 level after hours, the conference call becomes about two things: how long supply can stay ahead of demand (or at least keep pace), and whether management can extend the visibility story into the back half of calendar 2026 and beyond without stumbling over geopolitics. If Huang stays on-message—demand accelerating, supply chain secured for several quarters, and the platform moat widening—then the $200 print will look less like a pop and more like a reset point for the next leg of the AI cycle.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet