Nvidia GTC 2026 Preview: 3 Hardware Breakthroughs Fueling the Next AI Bull Run

As the artificial intelligence sector approaches critical physical limitations, all eyes are on San Jose. On March 16, 2026, NvidiaNVDA-- will host its annual GPU Technology Conference (GTC), an event widely recognized as the global benchmark for the computing power sector. Nvidia CEO Jensen Huang has previously noted that while technologies are approaching physical limits, the company is preparing to unveil components that will fundamentally restructure data center engineering. This transition from a pure computing power race to a complex system engineering and energy competition is highly bullish for specialized infrastructure providers, though it poses margin risks for legacy hardware manufacturers unable to adapt. As markets anticipate these technological leaps, Nvidia (NVDA) shares have recently surged, reflecting strong institutional confidence.

Architecture Leap: Rubin Ultra and the Feynman Showdown

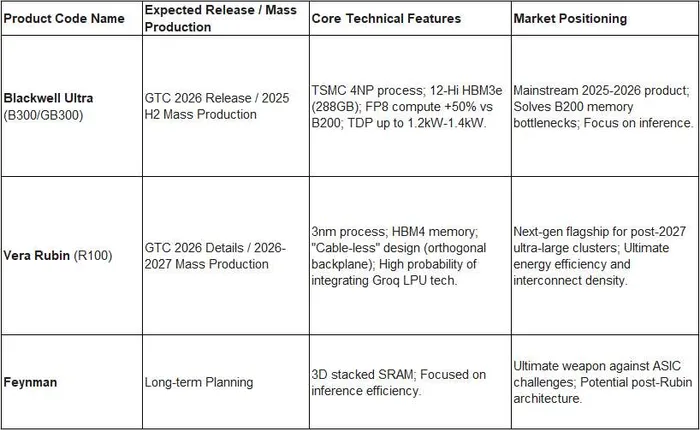

The 2026 GTC event will heavily focus on the technical specifications of the Rubin Ultra and outline the preliminary blueprint for the next-generation Feynman architecture. The industry expects the Rubin Ultra to establish a new standard for scale-up networks, utilizing a 1.5PB/s architecture that connects 144 GPUs. However, the most disruptive catalyst lies in the strategic direction of the Feynman generation. Rumored to utilize a 1.6-nanometer process, Feynman is expected to introduce advanced backside power delivery technologies.

Furthermore, as cloud service providers increasingly deploy custom Application-Specific Integrated Circuits (ASICs) to lower inference costs, Nvidia is exploring extensive SRAM-centric integration. Following its acquisition of Groq, Nvidia is expected to integrate Language Processing Unit (LPU) technology directly into its ecosystem. Analysts at Morgan Stanley note that integrating SRAM-based LPU architectures provides ultra-low latency and rapid token generation, effectively neutralizing the cost advantages currently held by competing ASIC manufacturers in the inference market. Enhanced LPX racks are projected to house 256 LPUs, distributed across multiple M9 glass-based printed circuit boards, cementing Nvidia's dominance in the highly competitive Agentic AI era.

Energy and Cooling Reconstruction

The pursuit of higher computing density has made power delivery and heat dissipation the primary bottlenecks for the semiconductor industry. The power consumption of a single Rubin chip is projected to exceed 2000W, while the subsequent Feynman chips are targeting thresholds above 5000W. Assuming stable voltage levels, doubling the power consumption implies a corresponding doubling of current, pushing three-stage power systems in the Rubin era toward the 3000A range. Traditional discrete power supply solutions have reached their limits regarding component count, routing losses, and printed circuit board (PCB) real estate.

Consequently, primary power supplies are making a definitive shift toward 800V high-voltage direct current (HDVC) architectures to reduce current and alleviate line losses. Furthermore, the implementation of modular and vertical power supply units—integrating inductors, capacitors, and control chips into three-dimensional modules—will significantly reduce PCB layout space.

This massive increase in power density means traditional air cooling can no longer support ultra-high-power chips. Liquid cooling is transitioning from an optional configuration to a mandatory industry standard. The year 2026 represents the inflection point for the liquid cooling market, with the proportion of liquid-cooled cabinets expected to rise from 85% to 100%. The focus of thermal management is also shifting toward advanced Thermal Interface Materials (TIM), with diamond heat sinks and liquid metals emerging as the dominant solutions to maintain optimal operating temperatures.

Interconnect Innovations and PCB Material Shifts

To support the massive data requirements of AI clusters, interconnect technology is undergoing a forced evolution. The year 2026 is officially designated as the commercialization year for silicon photonics, marking the large-scale deployment of Co-Packaged Optics (CPO) and Near-Packaged Optics (NPO). In the scale-out domain, Nvidia is anticipated to showcase critical CPO switches, including the Quantum 3400, Ethernet 6800, and 6810 models. By bringing optical engines closer to the switching ASICs, the industry aims to bypass the severe power consumption penalties associated with traditional digital signal processors (DSPs) in pluggable modules.

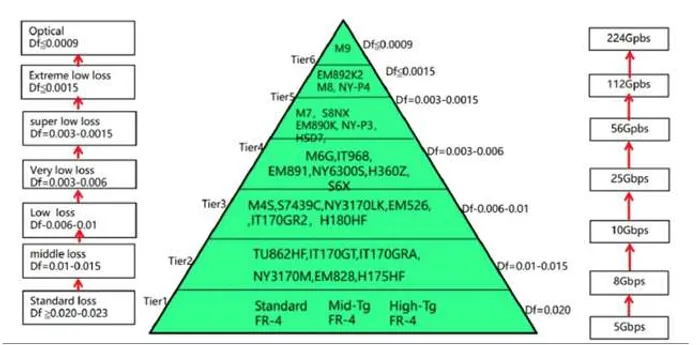

Simultaneously, the interconnect bandwidth enhancements require SerDes speeds to leap to 448G PAM4 and beyond. At these frequencies, traditional FR-4 and M7/M8 grade copper-clad laminates experience exponential signal attenuation. This physical limitation is forcing a mandatory supply chain transition to M9-grade PCB materials. M9 materials utilize ultra-low dielectric (Low Dk) fiberglass or fused quartz cloth, representing a significant technical barrier to entry for manufacturers.

The projected expenditure on M9-grade copper-clad laminates, featuring advanced PTFE substrates and multi-layer configurations, will constitute a significantly larger portion of the total server bill of materials moving forward. The complexity of manufacturing 78-layer mid-plane boards is expected to increase the value of these components by 20% to 25% per unit.

Spotlight on Key Supply Chain Players

The structural changes unveiled at GTC will serve as immediate catalysts for specific supply chain participants. Within the power architecture segment, Magmeet has secured a leading position in Nvidia's supply chain. The company is actively participating in the pre-research and development of 800V AC-to-DC and 800V-to-12V conversion systems for the Rubin generation, positioning it for substantial growth. In the optical communication sector, Taiwan Semiconductor Manufacturing Company (TSMC) remains a pivotal player, with yields for CPO-related components already reaching 90%, allowing the broader supply chain to accelerate inventory preparation.Meanwhile, Ainvest will also be present at the GTC exhibition, providing data terminal updates and ecosystem mapping.

Conclusion

The upcoming GTC 2026 conference confirms that the AI hardware market is no longer solely about graphical processing unit capabilities; it is a holistic competition encompassing energy efficiency, advanced packaging, and optical interconnects. As the industry transitions to 800V architectures, M9 PCB materials, and full liquid cooling, capital allocation must pivot toward the infrastructure providers enabling these physical realities.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet