NVIDIA's Gross Margin Hovers Near 75%: Can NVDA Maintain This Level?

NVIDIA Corporation NVDA is delivering unusually high profitability, with gross margins hovering around 75%. In the fourth quarter of fiscal 2026, NVDANVDA-- reported a GAAP gross margin of 75% and a non-GAAP margin of 75.2%.

Both metrics marked a significant improvement on a year-over-year basis as well as sequentially, driven by strong demand for its high-end artificial intelligence (AI) chips and favorable product mix. For the first quarter of fiscal 2027, it projects GAAP gross margin and non-GAAP gross margin of 74.9% and 75%, respectively, signaling NVIDIA’s confidence in generating high profitability.

The main driver behind these elevated margins is the pricing power of its AI chips. NVIDIA’s advanced platforms like Blackwell are in tight supply, while demand from hyperscalers, enterprises and AI model developers remains strong. Its ability to deliver superior performance per watt and lower cost per token allows customers to generate higher returns, justifying premium pricing for its AI chips.

Another key driver is its integrated ecosystem. NVIDIANVDA-- combines graphics processing units, networking and software like CUDA, making its solutions hard to replace. This reduces pricing pressure and supports margins.

Nonetheless, pricing power could weaken over time with the improvement in AI chip supply and an increase in competition. Large customers may also push for lower costs as their AI spending scales. New product ramps like Rubin could bring temporary cost pressures.

Overall, while margins may gradually normalize over time, NVIDIA’s technology leadership and ecosystem strength suggest it can still sustain high profitability, even if the 75% level moderates slightly.

How Competitors Fare Against NVIDIA

Advanced Micro Devices, Inc. AMD and Intel Corporation INTC are two major companies that are competing closely with NVIDIA in the AI and data center markets.

Advanced Micro Devices is gaining traction with its MI300 series accelerators, which are designed to handle training and inference for large AI models. AMD’s chips have attracted interest from major cloud providers seeking diversification beyond NVIDIA’s ecosystem. While Advanced Micro Devices’ non-GAAP gross margins are lower (57% in Q4 2025), its strategy focuses on offering competitive performance at a better price. This could gradually pressure industry pricing, especially if large cloud players diversify suppliers to reduce costs.

Intel is also reasserting its presence with the Gaudi series of AI accelerators. The company is positioning Gaudi3 as a cost-effective and scalable option for AI data centers, targeting enterprise clients looking for flexibility. Intel’s broad reach in CPUs and server infrastructure helps it integrate AI solutions more easily into existing systems. However, Intel’s non-GAAP gross margins (37.9% in Q4 2025) remain well below NVIDIA’s, limiting its ability to compete purely on profitability.

NVIDIA’s Price Performance, Valuation and Estimates

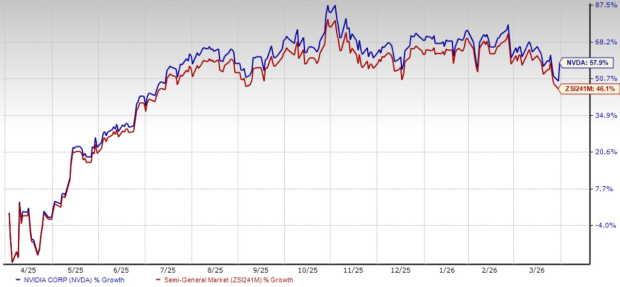

Shares of NVIDIA have risen around 57.9% over the past year compared with the Zacks Semiconductor – General industry’s gain of 46.1%.

NVIDIA One-Year Price Return Performance

Image Source: Zacks Investment Research

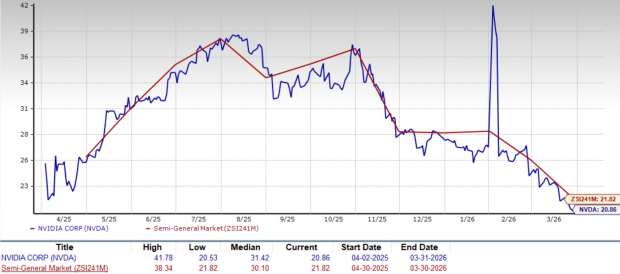

From a valuation standpoint, NVDA trades at a forward price-to-earnings ratio of 20.86, below the industry’s average of 21.82.

NVIDIA Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for NVIDIA’s fiscal 2027 and 2028 earnings implies a year-over-year increase of approximately 66.9% and 30.7%, respectively. Estimates for fiscal 2027 and 2028 have been revised upward in the past seven days.

Image Source: Zacks Investment Research

NVIDIA currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC): Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet