Nvidia’s Earnings Moment: Guidance Could Set the Tape for QQQ

Wall Street is bracing for Nvidia’s next blockbuster update. NvidiaNVDA-- reports fiscal Q2 2026 on Wednesday, Aug. 27, 2025, after the close—a print widely framed as “monster” in the run-up, with expectations for another record fueled by AI data-center demand.

Analysts expect adjusted earnings per share near $1.01–$1.02 on record revenue of $46 billion, up over 50% year-over-year despite significant headwinds from China export restrictions. Management’s update on new products—including next-gen AI chips and the Rubin series—will be critical for sentiment, especially with geopolitical uncertainty and China-related sales at stake. CEO Jensen Huang’s commentary on data center demand and the shifting regulatory backdrop is expected to set the tone for tech stocks broadly.

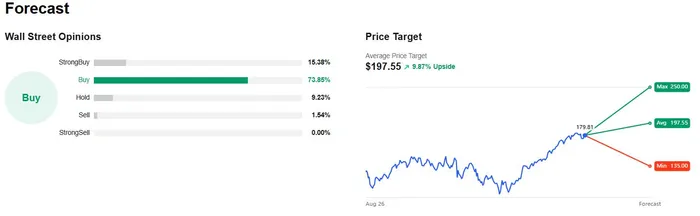

Analyst targets have raced higher: over the last month, the Bloomberg-tracked average for Nvidia rose 7.7%, the fastest pace this year. Notable recent hikes: Piper Sandler: $180 → $225, UBS: $175 → $205, Morgan Stanley: $170 → $200.

Source: AInvest

What to Watch in the Release

Data-center cadence: Street models about $41B+ from data centers, still torrid but scrutinized for any deceleration vs. prior blistering growth.

China friction & margins: A U.S. licensing arrangement on China sales could clip gross margin (analysts see ~72% this quarter) and keep investors focused on regional demand risk.

Product roadmap: Analysts remain upbeat on GB200 shipments and are already gaming out the next step in the Blackwell family—key for sustaining order visibility.

ETF Angle: QQQ’s One-Stock Swing Factor

Nvidia is now roughly 10% of Invesco QQQ (QQQ)—a top single-name weight that can sway the fund on earnings day. As of Aug. 25, the holding sits near 10.06% of the portfolio. Year to date (through Aug. 22), QQQ is up ~12.2%, with AI-heavy mega-caps continuing to carry returns. If Nvidia’s guide or margin track surprises, QQQ’s tape will likely reflect it.

ETF Angle: SOXL—High Octane, High Risk

Direxion Daily Semiconductor Bull 3x (SOXL) aims for 3× the daily move of a semiconductor index—great for short-term conviction, but compounding cuts both ways. Year to date (through Aug. 22), SOXL is roughly flat (+~1%) despite big swings; path dependency matters. Into NVDANVDA--, expect amplified reactions versus vanilla chip exposure.

Outlook, Trends, and Setup

The bull case: hyperscaler AI build-outs remain robust, Nvidia’s network stack (InfiniBand/Ethernet) and software moat keep attach rates high, and Blackwell shipments extend the cycle. The bear case: China drag, any cooling in data-center order growth, or a margin wobble could jar the “AI trade” even if headline numbers beat. Either way, guidance and supply commentary (lead times, next-gen ramps) should drive the tape as much as the print.

Bottom Line: For broad tech exposure (QQQ) and leveraged chip bets (SOXL), Nvidia’s print is the week’s fulcrumFULC--. A clean beat/raise likely recharges AI momentum; a cautious guide could spark factor-wide de-risking. Position sizing—and for SOXL, time horizon—matters more than ever.

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet