Nu (NU): Is Wall Street's Bullish Hype Justified in a High-Growth Fintech Landscape?

Nu Holdings Ltd. (NU) has emerged as a standout name in the fintech sector, with Wall Street analysts penciling in a "Moderate Buy" consensus rating, according to Finviz, and a 12.57% average price target upside per the MarketBeat forecast. But does the company's financial performance and strategic moat justify this optimism? Let's dissect the numbers and narrative.

Financial Firepower: Growth, Profitability, and Balance Sheet Strength

Nu's Q2 2025 results were nothing short of explosive. Revenue hit $3.7 billion, reflecting an 85% annualized growth rate since 2021, according to Nu's Q2 2025 results, while net income nearly tripled over two years to $637 million per the Investing.com transcript. Gross profit margin expanded to 42.2%, driven by disciplined cost management and a 55% YoY surge in interest-earning assets to $15.7 billion, according to the Yahoo Finance transcript. These metrics underscore Nu's ability to scale efficiently, a critical trait in capital-intensive fintech.

The balance sheet is equally robust. Deposits grew 41% YoY to $36.6 billion, per the Morningstar report, providing a stable funding base for its expanding credit portfolio. Active unsecured and secured loans rose 56% and 158% YoY, respectively, according to a Monexa update, signaling strong demand for Nu's financial products. Yet, the stock dipped 2.95% post-earnings in the transcript, hinting at market skepticism-perhaps over concerns about valuation or macro risks.

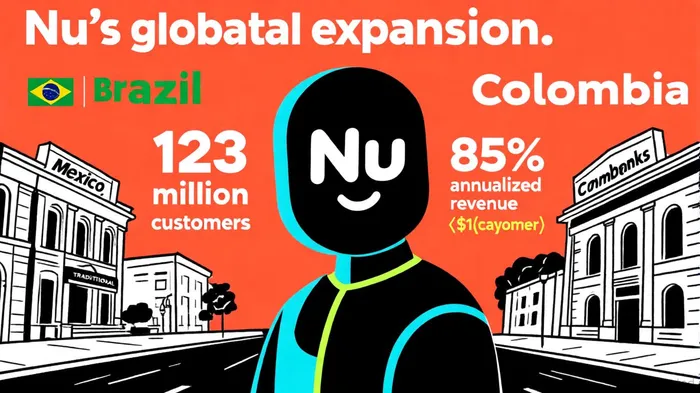

Strategic Moats: Tech-Driven Scalability and Global Ambitions

Nu's dominance in Latin America is unparalleled. With 114 million customers, it serves 30% of Brazil's adult population and 60% as their primary financial institution, per Statista data. Its AI-driven credit scoring and cloud-based infrastructure enable a cost-to-serve under $1 per customer, as noted in a LinkedIn post, while generating $10.7 in average revenue per active customer (ARPA) in the WhiteSight report. This "low-cost, high-margin" model is a textbook example of compounding growth.

Expansion into Mexico and Colombia has been equally impressive. Mexico's customer base grew 70% YoY in the PYMNTS article, and NuNU-- now serves 13% of Mexico's adult population, according to Monexa. The company is also pursuing a U.S. national bank charter (reported by PYMNTS), signaling ambitions to replicate its Latin American playbook in a $1.12 trillion global fintech market projected to grow through 2032, per the DigitalSilk forecast.

Analyst Rationale: Earnings Momentum and Conservative Leverage

Wall Street's bullishness is anchored in Nu's improving earnings trajectory. Earnings per share (EPS) estimates have seen upward revisions, with the Zacks consensus rising over recent months in a Nasdaq note. Analysts highlight a 27.91% return on equity (ROE) and a debt-to-equity ratio of 0.24, metrics that suggest strong capital efficiency and prudent leverage (per MarketBeat).

Goldman Sachs and Susquehanna recently raised price targets to $17.00 and $16.00, respectively, in a Nasdaq evaluations piece, citing Nu's cross-selling potential (4.1 products per user per the WhiteSight report) and AI-driven risk mitigation. The average 12-month price target of $17.06 implies a 12.57% upside from current levels, a premium that reflects confidence in Nu's ability to monetize its massive user base.

Risks: NPLs, Macroeconomic Volatility, and Regulatory Hurdles

No bull case is without caveats. Non-performing loans (NPLs) rose to 4.7% in Q1 2025, according to Monexa, a red flag as Nu expands into riskier underbanked demographics. While the company has refined its risk management processes, Monexa notes that rising inflation and currency fluctuations in emerging markets could strain margins.

Regulatory complexity is another headwind. Tightening data privacy laws in Brazil and Mexico could increase compliance costs, per Monexa, while competition from traditional banks and AI-powered fintech rivals threatens Nu's pricing power. The pursuit of a U.S. banking license, reported by PYMNTS, is a strategic move but could delay expansion timelines.

Verdict: A Buy for the Long-Term, But Not Without Caution

Nu's financials and strategic positioning are undeniably compelling. Its ability to scale a low-cost digital platform, coupled with a 58% YoY revenue surge in 2024 (per Monexa), validates Wall Street's optimism. However, investors must weigh the risks of macroeconomic volatility and rising NPLs.

For those with a 3–5 year horizon, Nu represents a high-conviction play in the digital banking revolution. But for shorter-term traders, the stock's 2.95% post-earnings dip noted in the transcript may reflect lingering doubts about near-term execution. As always, diversification and a close eye on NPL trends will be key.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet