NTT DC REIT's Flat Debut: A Warning for Data Center REITs in a Tightening Market?

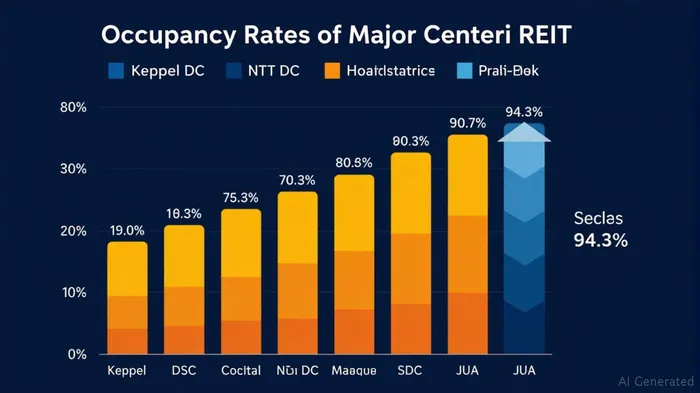

The underwhelming listing of NTT DC REIT on July 14, 2025—opening at $1.00 and rising just 3% in its first hour—sparked questions about investor sentiment toward data center REITs amid rising interest rates and shifting supply-demand dynamics. While the REIT's 94.3% occupancy rate and 7.5% yield initially seemed compelling, its tepid trading debut highlights broader concerns about valuation sustainability in a sector increasingly scrutinized for its reliance on hyperscale tenants and debt-fueled growth. Here's why this matters for investors, and where opportunities might lie.

The Numbers That Matter: Occupancy, Leases, and Debt

NTT DC REIT's portfolio boasts a staggered lease profile, with no more than 20% of leases expiring annually over the next five years. Its weighted average lease expiry (WALE) of 4.8 years is solid, but the reliance on a single tenant—reportedly TeslaTSLA--, which accounts for 31.5% of rental income—introduces critical concentration risk. This contrasts with Keppel DC REIT, which has a more diversified tenant base and a WALE of 5.2 years. While NTT's occupancy is strong, the Tesla dependency creates a vulnerability: a single tenant's financial or strategic shift could destabilize cash flows.

Debt metrics, meanwhile, appear manageable at 35% leverage post-IPO, well below the 50% regulatory cap. Yet the looming specter of rising interest rates complicates this picture. . While NTT's current fixed-rate debt structure (70% hedged) buffers against near-term rate hikes, its ability to refinance or acquire new assets without dilution hinges on maintaining low leverage. The lack of a capex reserve adds another layer of risk, as future maintenance or expansion costs could eat into distributions.

Why the Market Yawned—and What It Says About Data Center REITs

Investors' muted response to NTT's listing suggests skepticism about the sector's ability to sustain high yields amid macroeconomic headwinds. The REIT's 7.5% projected yield for 2026—surpassing peers—is appealing, but it comes with strings attached. Unlike Digital Core REIT, which has a proven track record of steady growth, NTT's reliance on sponsor-backed acquisitions (e.g., 130 MW of near-term pipeline assets) may not yet justify its premium. The absence of a capex reserve and the decision to pay management fees in units rather than cash further weigh on confidence.

Moreover, the broader data center sector faces a supply-demand balancing act. While AI-driven cloud adoption continues to fuel demand, oversupply risks loom in markets like Singapore, where NTT's Serangoon North data center competes with peers. . The sector's growth is undeniable, but REITs with poor tenant diversity or high leverage could struggle to command premiums in a slowing economy.

Actionable Insights: Where to Look for Value

The NTT DC REIT debut underscores the need for selective investing in data center REITs. Here's how to navigate the space:

Prioritize Tenant Diversification: Avoid REITs overly reliant on a single tenant. Keppel DC REIT's 4.3% yield may seem low, but its geographic diversity (U.S., Europe, Asia) and tenant mix reduce idiosyncratic risk.

Focus on Lease Stability: REITs with longer WALE and staggered expiries—like Keppel's 5.2 years—offer more predictable cash flows. NTT's 4.8 years are decent, but the Tesla exposure offsets this advantage.

Debt Discipline Over Yield: NTT's 7.5% yield may entice income seekers, but investors should demand REITs with debt below 40% and clear capex buffers. Digital Core's 6.9% yield, paired with a 34% leverage ratio, strikes a better balance.

Wait for Sector Pullbacks: NTT's post-IPO flatness could create an entry point if its yield expands due to price declines. However, investors should wait for clearer signs of hyperscale tenant demand or sponsor asset sales before committing.

Conclusion: Caution Amid Growth

NTT DC REIT's underwhelming listing isn't just a company-specific issue—it's a sector-wide wake-up call. While data center demand remains robust, investors must scrutinize tenant concentration, debt flexibility, and yield sustainability. For now, REITs like Keppel DC and Digital Core, with their diversified profiles and prudent capital structures, offer safer havens. NTT may yet find its footing, but its debut reminds us that even in booming sectors, fundamentals—and not just hype—rule the day.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet