November CPI Preview: Could Be a Positive Surprise, Reviving Expectations for Fed Easing Next Year

With the unemployment rate recently hitting a four-year high and fresh AI-related concerns emerging after reports that Oracle's data center expansion may be facing funding strains, the upcoming CPI release carries heightened risk for markets. The U.S. Department of Labor will publish the November CPI report—the first inflation reading since the end of the longest government shutdown in U.S. history—and it could deliver a surprise.

After the Fed signaled last week that its easing cycle may be nearing an endpoint, and with the labor market already showing signs of fatigue, only a renewed slowdown in inflation would justify further rate cuts. If inflation meets or exceeds expectations, it could deal another heavy blow to already volatile financial markets.

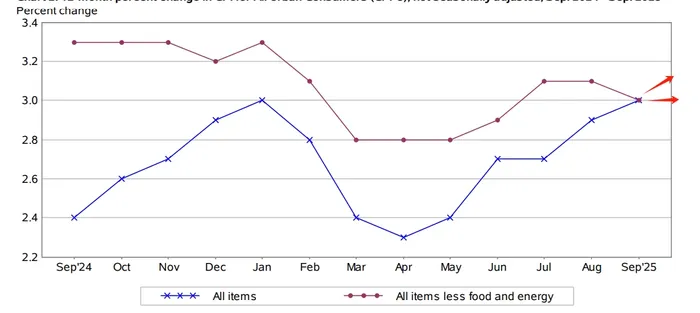

Consensus expects headline CPI to rise 3.1% year over year in November, the highest level since May 2024. Core CPI—the Fed's preferred gauge—is expected to increase 3.0% year over year, unchanged from September. Notably, because the October CPI report was missing, this release will not include month-over-month data.

"The psychological distinction between a two handle and a three handle is going to be paramount," José Torres, senior economist at Interactive Brokers, said in an interview with CNBC. He expects both headline and core CPI to come in at 2.9%, below consensus. Such an outcome could provide positive momentum for equities heading into 2026 and reshape expectations for next year's rate outlook, where the Fed currently projects just one cut.

However, even a slightly better-than-expected inflation reading may not be enough to turn the tide, as this report carries notable distortions. Victoria Fernandez, chief market strategist at Crossmark Global Investments, said, "This is not going to be a clean CPI report." She pointed to the absence of month-over-month data and uncertainty around when November data collection actually began as key issues.

President Trump signed the funding bill on November 12, but it took time for the government to fully reopen. "By the time the government actually opened and they started collecting data, we were almost halfway through the month of November, so you're only getting the last half of the month," Fernandez said. "You have to start wondering, 'Is there some kind of bias in terms of what prices do and how things work in the latter half of the month versus the beginning of a month?"

The broader theme remains that inflation is still elevated, while the effects of three consecutive rate cuts and the halt in balance-sheet runoff need more time to filter through the economy—factors that keep the Fed cautious. If inflation comes in above expectations, especially alongside a rising unemployment rate, the Fed could find itself in a policy dilemma, further clouding the monetary outlook.

With gaps in official data, third-party indicators have taken on greater importance.

President Trump has been notably effective at keeping energy prices in check. According to EIA data, U.S. retail gasoline prices across all grades fell 0.3% month over month in November to $3.179 per gallon, up just 0.1% year over year. However, highway diesel and jet fuel prices rose 8% and 9% year over year, respectively.

As time passes, the impact of tariffs appears to be gradually absorbed. Auto and apparel prices have stabilized, but without month-over-month data, year-over-year increases may appear more pronounced. J.D. Power and GlobalData estimate that the average new-vehicle retail transaction price in November rose 1.6% year over year to about $46,000 per vehicle. The Manheim Used Vehicle Value Index shows that wholesale used-vehicle prices over the first 15 days of November were down 0.2% year over year.

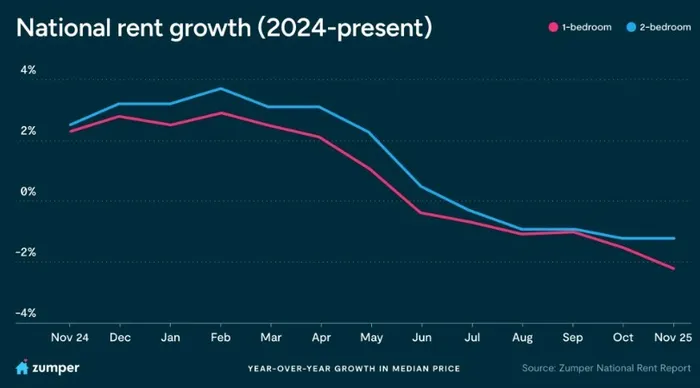

Housing remains the most critical component, accounting for more than one-third of the CPI basket and the largest share of core CPI. Data from rental platform Zumper show that the median monthly rent for a one-bedroom apartment fell 0.7% month over month to $1,501 in November, while two-bedroom rents declined 0.4% to $1,880. On a year-over-year basis, rents fell 1.2% and 2.2%, respectively.

"Our National Rent Index shows one-bedroom rent down more than 2% year over year, the steepest decline we've recorded since we started tracking national rent data," said Anthemos Georgiades, CEO of Zumper. "It's a clear signal that the cooling we're seeing isn't just seasonal. This pattern is playing out across most of the country, with only a few outliers, like San Francisco, moving in the opposite direction. It reflects a two-tiered economy and rental landscape: many markets are slowing under softer labor conditions, while a small number of high-wage hubs continue to accelerate."

Overall, despite the government shutdown, U.S. prices appear to have remained relatively stable in November. Softer consumer demand and fading tariff effects have helped offset upside risks. As a result, the odds of CPI coming in below expectations may be slightly higher, which could support markets—especially given tight year-end liquidity and a lack of recent positive catalysts. Still, with policy easing requiring time to transmit through the economy, the Fed is likely to maintain a cautious stance. That, in turn, could reshape next year's monetary policy path: more rate cuts would imply stronger risk appetite.

Crypto market researcher and content strategist with 3 years of experience in digital asset analysis and market commentary. Skilled at transforming complex blockchain data and trading signals into clear, actionable insights for investors. Experienced in covering Bitcoin, Ethereum, and emerging ecosystems including DeFi, Layer2, and AI-related projects. Passionate about bridging professional market research with accessible storytelling to empower readers and investors in the fast-evolving crypto landscape.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet